Private Credit Unfiltered: Can a Sponsor Fix a Stranded BDC?

KKR is testing with FSK. The structure of the trade tells you what they think the marks are worth

A public BDC trading at 0.57x NAV is stranded. It can’t issue equity. Its cost of capital is broken. The sponsor can’t grow the vehicle, can’t deploy through it, can’t show the market that the discount is irrational without putting capital on the line.

KKR is trying to do something about that with FSK 0.00%↑.

The four-part package they announced this week is an attempt at confidence repair in a stranded public BDC.

Tender, preferred, buyback, fee waiver, all in one press release.

Whether it becomes a template for other discounted BDCs depends entirely on whether it has any impact. If FSK can improve the discount, expect imitators. If the discount holds or widens, expect sponsors to follow Apollo’s MFIC approach instead and exit through a sale or portfolio wind-down rather than try to repair the wrapper.

The structural nuances in how this one was built are worth attention either way, because they tell you what a sponsor will and won’t do when faced with a stranded vehicle, and they reveal which parts of the package are genuine and which are optics.

I wrote about FSK's bonds at the end of April, when the credit was already telling a different story than the equity narrative. This week the equity side got an answer.

What KKR just announced

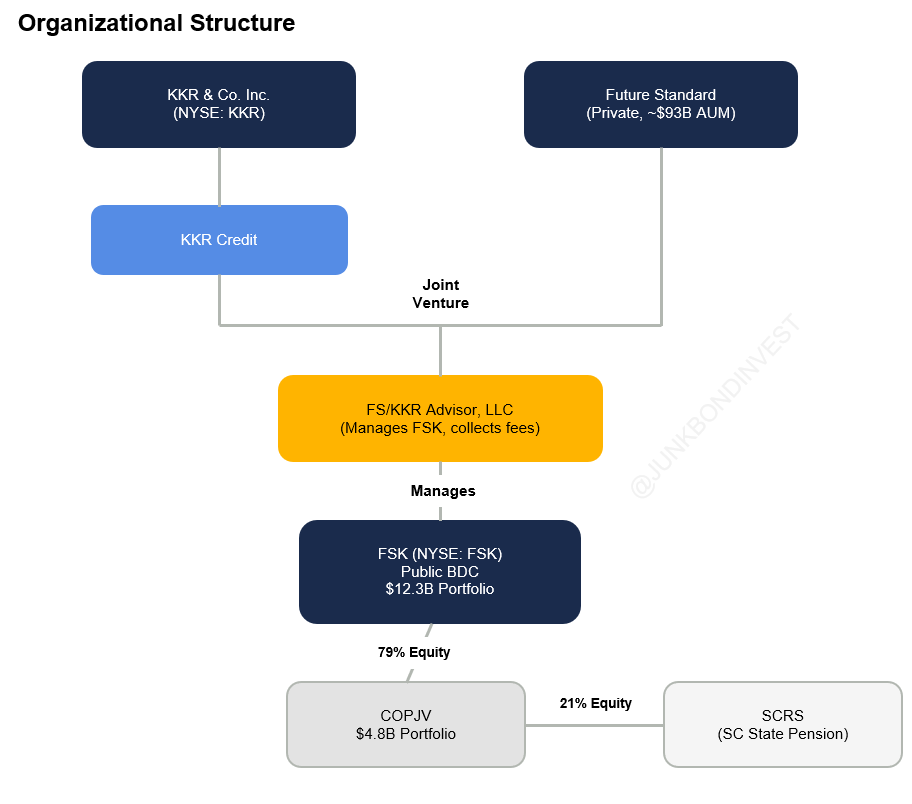

For background, FSK is managed by FS/KKR Advisor, a joint venture between KKR Credit and Future Standard (formerly FS Investments), with both parties sharing management and incentive fees. Here’s the simplified org chart:

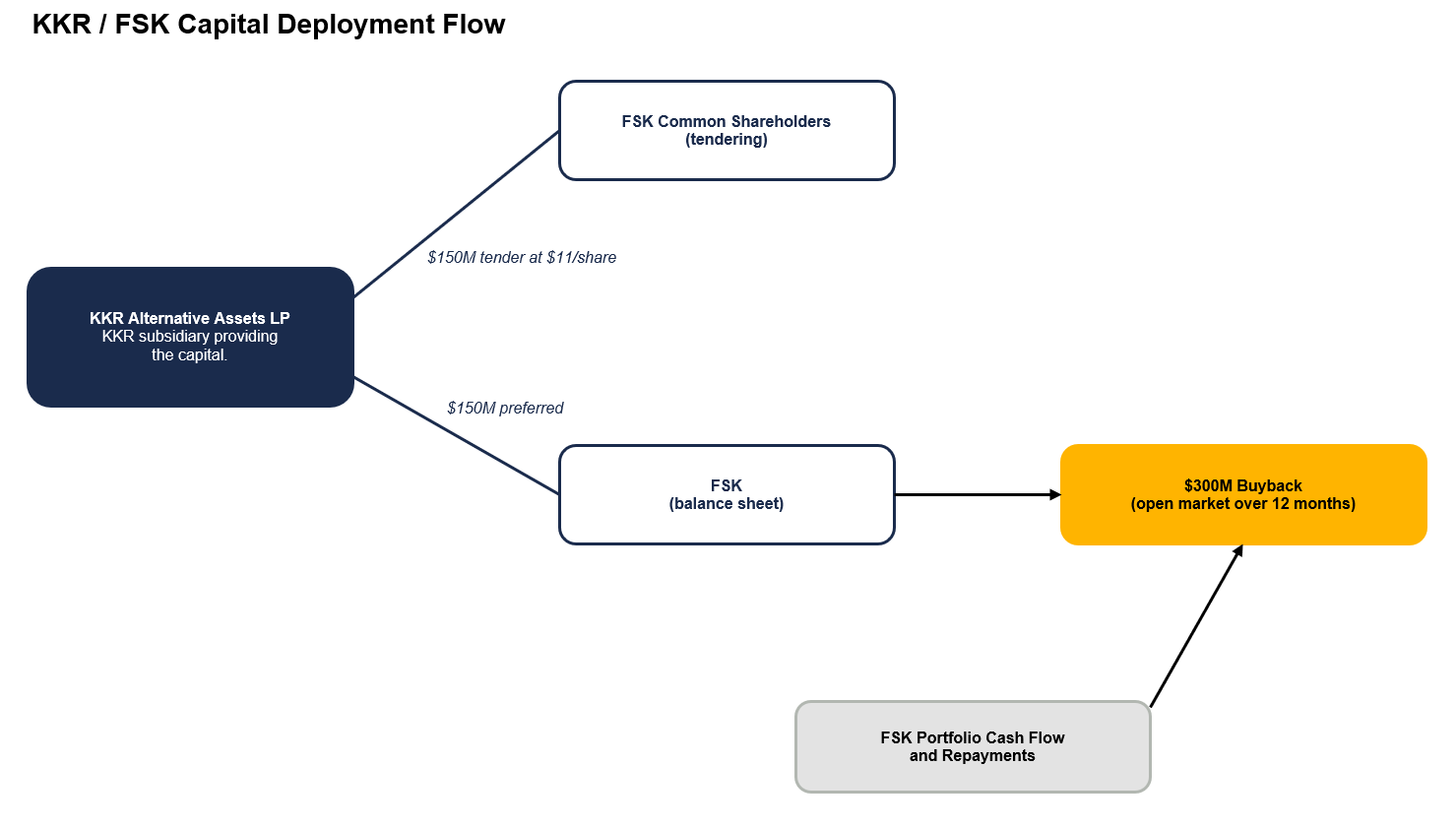

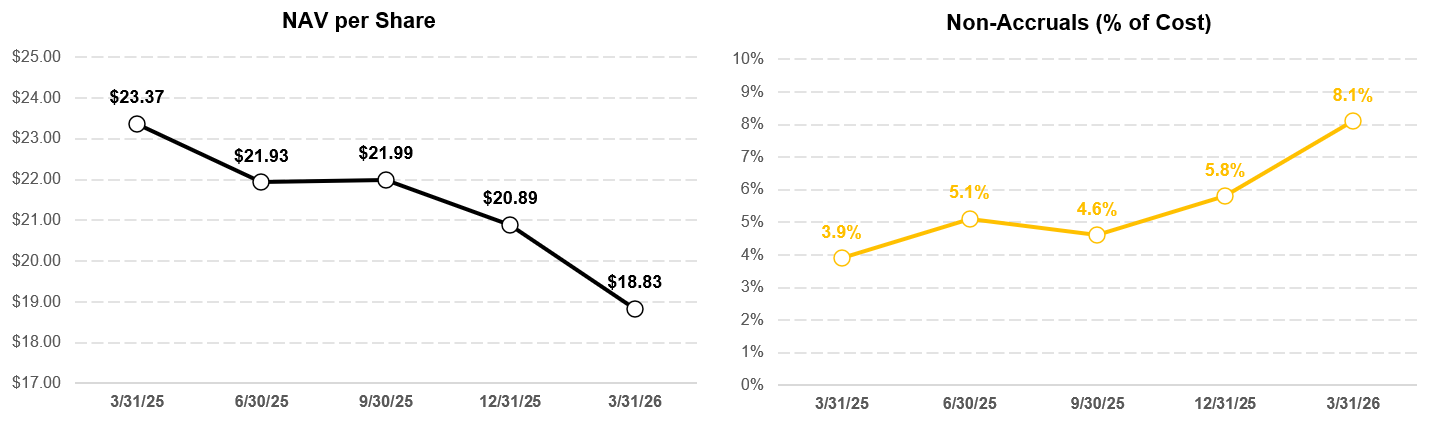

KKR Alternative Assets LP, a KKR subsidiary will tender for up to $150 million of FSK common at $11. The tender opens May 12 and runs 20 business days. Once it closes, KKR buys $150 million of cumulative convertible perpetual preferred from FSK at a 5% cash coupon (or 7% PIK), convertible to common at $18.83, which is the current NAV.

FSK’s board separately authorized a $300 million stock repurchase program through June 2027, funded from FSK’s own balance sheet including the preferred proceeds. KKR also waived its share of the subordinated income incentive fee for four quarters.

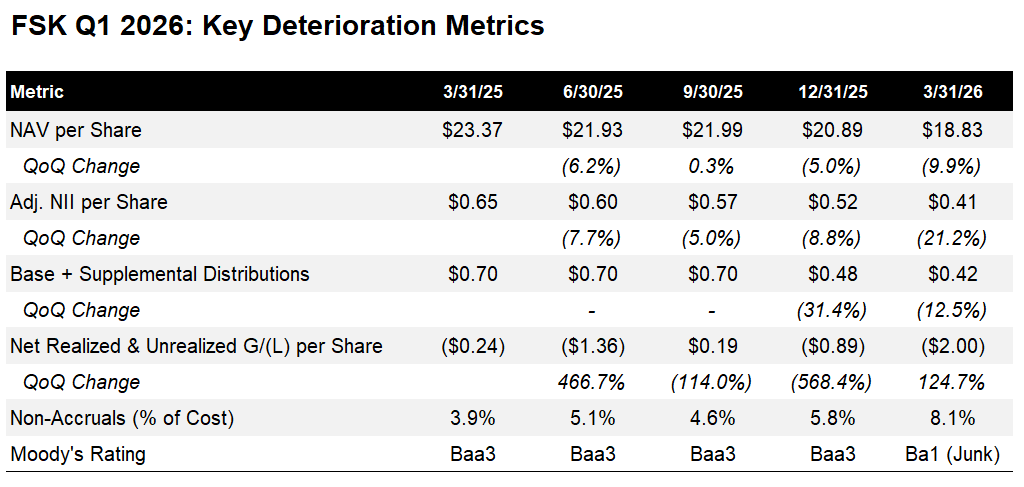

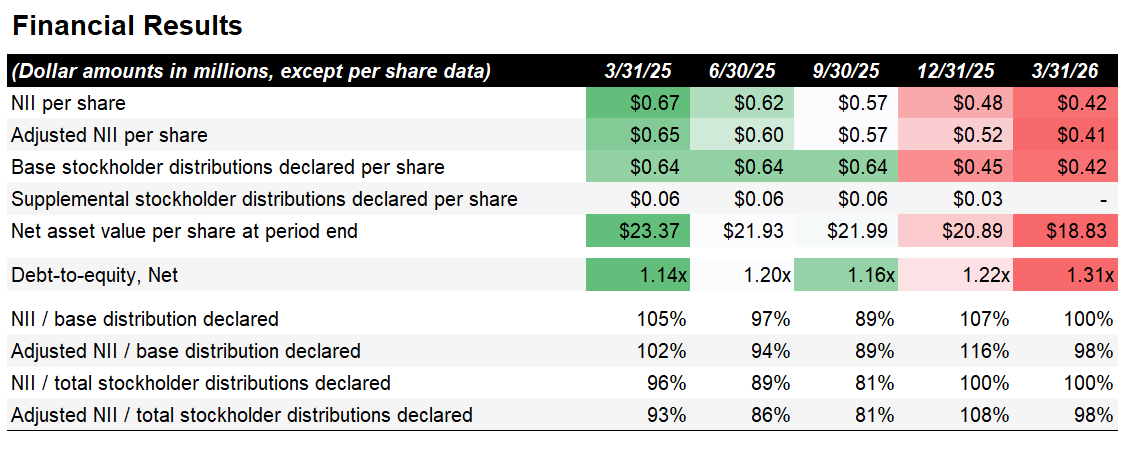

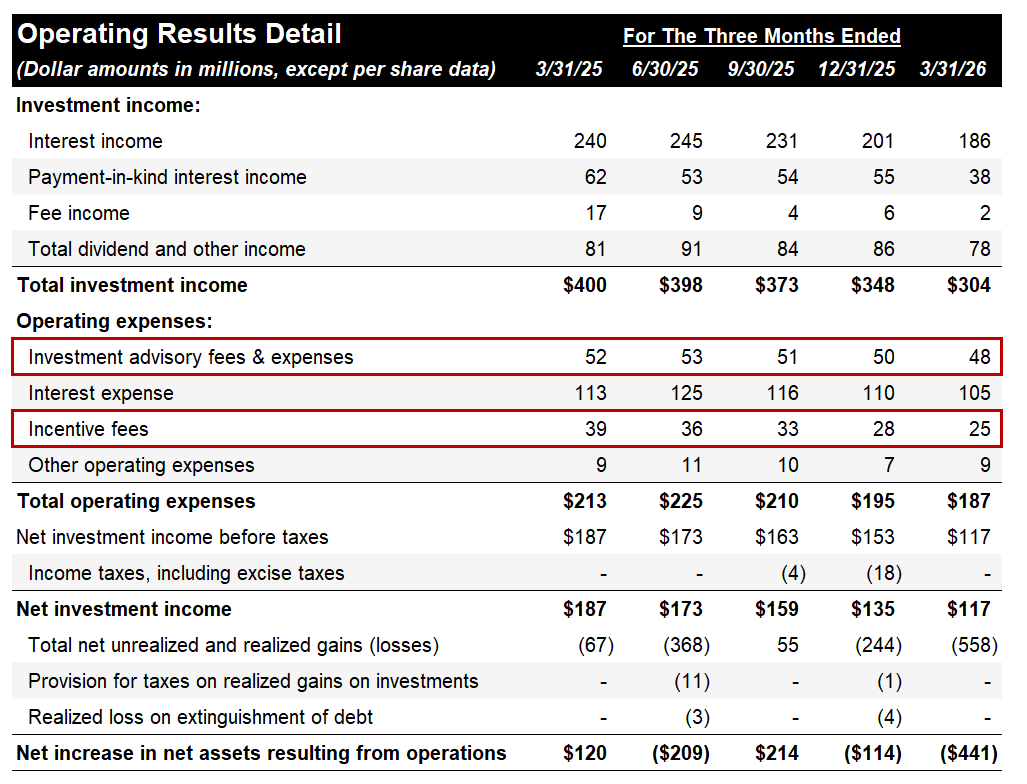

The backdrop to this explains the move. A 9.9% NAV decline, Adj. NII at $0.41 vs. $0.52 the prior quarter, $2.00 per share of realized/unrealized losses, non-accruals at 8.1% of cost, and a Q2 dividend reset from $0.48 to $0.42. Moody’s cut FSK to junk in March. The senior secured revolver was amended May 8 to shrink commitments and reset the minimum equity covenant lower.

The quarter forced the action. The structure is the more interesting part.

The stranded BDC problem

The modern public BDC model depends on growth. Trade at or above NAV. Issue equity at a premium. Deploy proceeds into senior secured loans. Earn the spread. Distribute the income. Repeat. Read this if you’re new to BDCs:

When the stock trades at ~60% of NAV, that loop breaks. Equity issuance would be massively dilutive. The vehicle can no longer grow. The sponsor still earns management fees on a fixed asset base but loses the ability to compound the platform. The market is essentially telling the sponsor that the franchise is worth less alive than the underlying portfolio is worth on paper.

The sponsor has three plausible responses. Sell the vehicle and exit. Run the vehicle in slow-motion runoff and harvest fees. Or try to fix the discount and reopen the equity issuance window.

Apollo picked option one with MFIC. KKR is testing option three with FSK. Whether other sponsors with discounted BDCs follow KKR or Apollo depends on whether the FSK trade actually moves the stock. Right now, neither option has been validated, and most BDCs trading at meaningful discounts are running variations of option two by default.

The $300 million headline obscures whose downside is whose

The package puts $300 million of KKR capital into FSK across two pieces. $150 million tenders for common at $11. Another $150 million buys preferred convertible to common at NAV.

The number that matters most is $11.

KKR is publicly defending an $18.83 NAV. The stock trades at $10.84. A sponsor that believed the NAV was real and the discount was irrational would tender at a meaningful premium to market, somewhere between $14 and $16, capturing upside to NAV for itself while delivering a real bid to exiting shareholders. That tender would be a credible signal of conviction.

KKR didn’t do that. The $11 tender is 2% above the market clearing price and 42% below the NAV the company is defending. The premium to market is so thin that it barely counts as a bid. KKR is offering to buy common at almost exactly the price the market is already clearing at, then accumulating the maximum possible discount on every share tendered.

The preferred reinforces the same posture. KKR is putting $150 million into a senior security with a coupon, conversion optionality, and redemption rights, rather than putting that capital directly into common. The preferred sits ahead of common in every scenario. A sponsor confident in the NAV would put at least some of the capital into common at or near market. KKR put none.

Together the structure says: KKR wants to support the vehicle, but on terms that protect KKR from the common-equity outcome the company is publicly defending. The tender accumulates common at the market price. The preferred sits senior. The buyback gets funded partly by FSK’s own balance sheet. KKR captures the discount in the tender, the seniority in the preferred, and the conversion upside if the NAV thesis works. Existing common shareholders are stuck at their original cost basis with none of those protections.

This isn’t bad. It’s a rational way to deploy sponsor capital into a stranded vehicle while limiting the sponsor’s downside. But it isn’t the structure a sponsor builds when it genuinely believes the marks. A sponsor that believed $18.83 was the real number would have tendered at $14 and put more of the support into common. KKR did neither.

For any future template, the tender price is the cleanest test. A tender at a meaningful premium to market signals genuine conviction in the NAV. A tender at or near the market clearing price tells you the sponsor wants to accumulate common cheaply while talking about alignment. The press release will frame either version as confidence. The number tells you which one it is.

The conversion strike also means nothing

The preferred converts at $18.83, exactly reported Q1 NAV.

Nobody at KKR thinks FSK’s NAV is worth $18.83. The stock trades at ~$11 because the market is pricing further deterioration, not par recovery. The strike isn’t a forecast.

It’s the symbolic anchor of the package. Setting the strike at reported NAV lets KKR and FSK tell shareholders that sponsor capital is locked in at the same valuation the company defends publicly. The strike signals alignment with reported NAV without requiring KKR to express any actual view on intrinsic value.

There’s also a sneaky part. The strike also ratchets down for special dividends. With Q4 spillover income near $1.66 per share, FSK may need to declare special distributions in late 2026 to maintain RIC status. Each one mechanically lowers the effective conversion price. The headline strike sits at NAV. The effective strike drifts lower through distributions and likely settles closer to the prevailing market range.

If this template gets copied, the conversion strike will sit at reported NAV every time. It’s the only number that lets the sponsor sell alignment. Read it as cosmetic, not predictive.

The fee waiver exposes the JV problem

The fee waiver is the most revealing part of the package.

FS/KKR Advisor, LLC is a joint venture between KKR Credit and Future Standard. Both entities earn management and incentive fees from FSK. The “alignment” announcement waives KKR’s portion of the subordinated income incentive fee for four quarters, covering 50% of the total.

Future Standard waived nothing.

The other half of the manager, the same entity earning fees on the same vehicle through the same JV, is taking the same economics it took last quarter. After a 10% NAV decline, higher non-accruals, weaker earnings, and a dividend cut, Future Standard is collecting full freight.

This matters for any future template. A single-manager BDC doing a similar package would have the sponsor waiving the full incentive fee, not half. FSK’s JV structure means KKR cannot deliver the cleaner version of alignment without Future Standard cooperating, and Future Standard didn’t. The result is a fee waiver that gets reported as alignment but functions as a partial concession from one of two parties responsible. The press release doesn’t acknowledge the asymmetry. The footnotes do.

The lesson for reading the next package: check who controls the manager. Single-sponsor BDCs can deliver real fee alignment. JV-managed BDCs deliver partial alignment dressed up as the real thing.

The buyback is the part that actually has to work

If NAV is credible, repurchasing stock at 60 cents on the dollar is one of the most accretive uses of capital available to FSK. The math is straightforward. Every share retired at $11 against $18.83 of NAV adds NAV per share for the holders that stay.

That’s also the if.

If the marks keep moving down, FSK is spending capital retiring stock at $11 while the underlying portfolio is worth less than that price implies. The buyback then becomes a transfer of value from the company’s balance sheet to the shareholders who tendered or sold during the program, at the expense of remaining shareholders bearing continued markdowns.

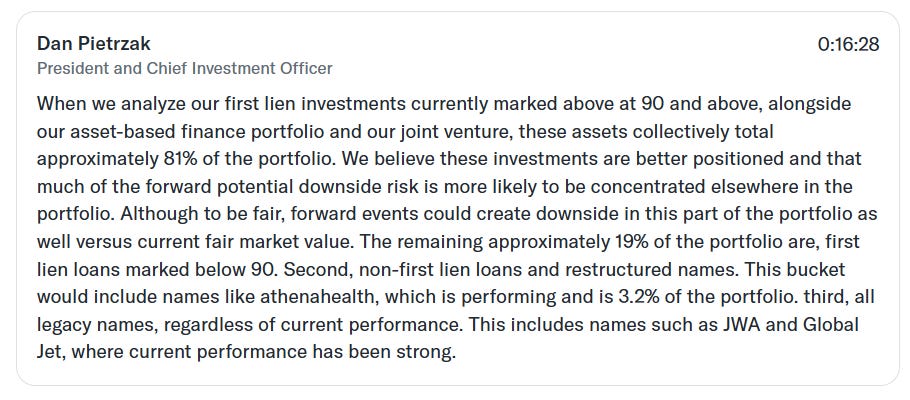

The package is making a bet that the marks are roughly correct and the discount is irrational. Management itself disclosed that 19% of the portfolio sits in a higher-risk bucket including all legacy investments and first-lien loans marked below 90. The buyback is being funded against a book where management has already publicly identified roughly one-fifth as problem paper.

If the bet works, the buyback is genuinely accretive, the stock re-rates closer to NAV, and the equity issuance window reopens. If the bet doesn’t work, the buyback is sponsor-financed share retirement at prices the underlying portfolio doesn’t support.

The market will vote on this over the next several quarters. But the marks problem isn’t separable from the confidence problem. The market trading FSK at $11 isn’t doing so because it’s irrational. It’s discounting the reported NAV because it doesn’t trust the portfolio is worth $18.83. Sponsor capital signaling confidence in the NAV doesn’t change whether the NAV is actually right.

Medallia is one of the cleaner near-term data points

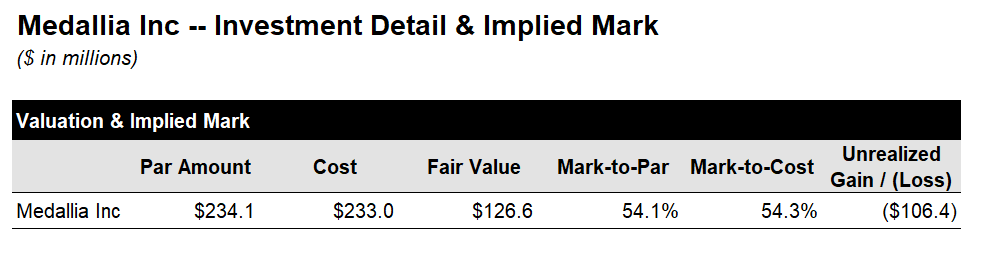

Medallia stopped paying interest to FSK in Q1. Marked at 54 cents, on non-accrual. Thoma Bravo signaling it will hand the keys to lenders. A group including Blackstone is putting in $100 million to fund the workout.

Eight other BDCs hold the same first-lien paper. Each will have to defend its own mark against the 54-cent comp in Q2.

The relevance for the FSK trade is direct. KKR is committing $300 million of headline capital to a fund whose biggest single-name NAV driver this quarter is marked at 54 cents, with the workout being run by a different sponsor. If Medallia recovers materially above 54 cents, the FSK trade looks smart. If it settles at or below 54 cents, the FSK trade is spending capital validating marks that are still moving.

The Medallia outcome also contributes to a broader test. Direct lenders argued for most of the post-2020 cycle that first-lien paper in a software business with recurring revenue recovers at or near par because the lender controls the asset. The 54-cent mark is one of the cleaner near-term challenges to that thesis. It isn’t the whole referendum, but it’s an actionable data point for institutional readers trying to calibrate where recovery values actually settle in this cycle.

What to watch in the next package, if there is one

FSK may end up being the only public BDC that tries this version of the trade. If the stock doesn’t move toward NAV by the end of 2026, other sponsors will look at the result and conclude that sponsor capital can’t fix a marks problem, and they’ll head toward Apollo’s MFIC exit route or simply run their vehicles in quiet runoff.

If FSK does work and the template gets copied, three dimensions are worth watching.

How much new common-equity risk does the sponsor actually take? FSK’s package put $150 million of new capital into the stack through senior preferred, not common. A more aggressive package would put sponsor money directly into common at or near market. The form of the capital tells you how much confidence the sponsor has in the marks.

Does the sponsor control the manager? FSK’s JV structure produced a half-aligned fee waiver. A single-sponsor BDC can deliver cleaner concessions. Watch whether manager economics actually move or whether the optics get reported as alignment without the substance.

Is the buyback funded by new proceeds or by retiring the balance sheet? FSK’s $300 million authorization is partly funded by KKR’s preferred proceeds and partly by the fund’s own runoff. A buyback funded by current portfolio cash flow is a different statement than one funded by drawing down the balance sheet.

The honest version

The press release calls it strategic value enhancement. The structure is a stranded vehicle trying to repair its own equity story with sponsor capital, while the sponsor protects itself against the possibility that the marks are still moving.

The trade works if FSK’s portfolio is worth roughly what management says it’s worth. If that’s true, the buyback is accretive, the stock re-rates, and the playbook becomes available to other discounted BDCs. If the marks are wrong, the playbook reduces to sponsor-financed share retirement at prices the underlying portfolio doesn’t support, and other sponsors will draw the obvious conclusion.

Judging by the market’s reaction, the verdict is clear. Confidence repair can’t solve a marks problem, and the marks problem is what’s actually driving the discount. But the next few quarters of FSK trading and the eventual Medallia recovery will tell us more than I can.

For now, the structural nuances are what travel. The headline number isn’t the headline. The conversion strike is theater. The fee waiver only goes halfway because the JV partner didn’t cooperate. The buyback math depends entirely on whether the marks hold.

That’s what a stranded BDC trade looks like when a sponsor decides to fight rather than exit. Whether other sponsors choose the fight is the open question.

Excellent piece.