Private Credit Unfiltered: Everyone Is Talking Their Book

A field guide to who's selling what in the private credit stress cycle

Everybody’s telling a version of the truth and everybody’s selling you something.

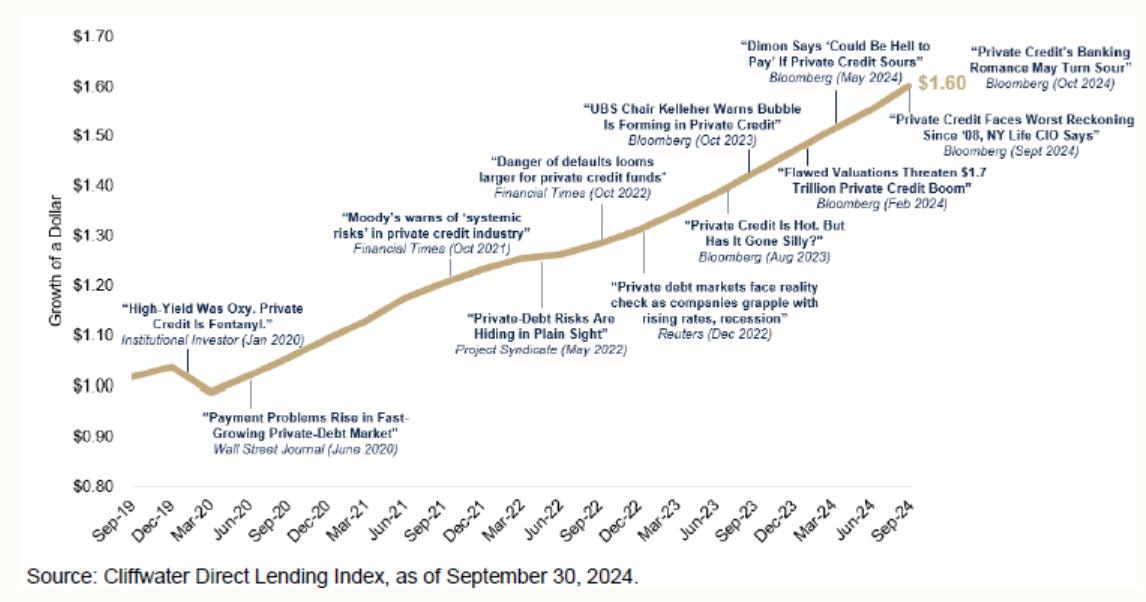

Howard Marks wrote 6,000 words about how private credit lost its mind. Goldman mailed a shareholder letter that read like a recruitment brochure. Blackstone closed a $10 billion opportunistic fund the same week Moody’s downgraded the sector. Cliffwater published a defense. Bain went on Barron’s to say there’s no bubble.

All in the same week. Not one of them disinterested.

None of them are lying, either. That’s the trick.

Every piece of public commentary was a fundraising document dressed up as market analysis. And the 5% redemption gate, the mechanism trapping billions inside non-traded BDCs right now, is what lets these narratives run at the same time without anyone having to be wrong.

The Gate Creates a Narrative Market

A large subset of private credit managers are now processing redemption queues that will take 2-4 years to clear. Blue Owl’s technology fund saw 40.7% of investors request their capital back in Q1. The larger credit fund saw 21.9%. Barings saw 11.3%. All fulfilled at the 5% cap.

These gated managers aren’t frozen. They have revolvers, CLO warehouse lines, and portfolio cash flow from loan maturities and interest payments. OTIC told investors it has $1.3 billion in liquidity across cash, undrawn debt, and other liquid assets against a $6 billion portfolio.

But the constraint is real even if the capital is technically available. When your debt costs are rising, your hurdle rate on new originations goes up, which means you need wider spreads to hit the same return targets, which means you’re less competitive on deals where an ungated fund can bid tighter.

Boards and risk committees in defensive mode tend to slow deployment even when the liquidity is there. The result isn’t that gated funds stop lending. It’s that they lend more cautiously, at higher internal hurdle rates, with less leverage flexibility, while ungated funds and closed-end vehicles are deploying aggressively into the same pipeline with a structural cost-of-capital advantage.

The queues aren’t shrinking either. Moody’s spelled out the feedback loop in its sector downgrade: investors who were prorated in Q1 will resubmit in Q2 for their remaining balance. Investors who weren’t planning to redeem see the gates go up and submit preemptive requests to get in line. The queue grows even as it’s being processed. At 5% per quarter against a 40% backlog, the math alone takes 8 quarters to clear, and that assumes zero new requests.

That vacuum is what everyone else is positioning around. The public commentary sounds like market analysis when it really functions as a sales pitch.

Goldman Telling You Exactly What’s Happening

Goldman Sachs Private Credit Corp. (GSCRED) was the only major non-traded BDC to come in under the 5% quarterly redemption cap (4.999% to be exact). The shareholder letter didn’t just report this. It built an investment thesis around it.

The fund said the retreat of retail capital will produce a more lender-friendly environment, reversing the supply-demand imbalance that benefited borrowers in recent years. Wider spreads. Stronger documentation.

Why did Goldman avoid the gate? Institutional LPs accounted for more than 80% of their platform’s capital. Long-duration commitments from pensions and sovereign wealth funds that aren’t subject to the same redemption dynamics as retail vehicles. The fund didn’t outperform on credit quality. It outperformed on LP composition.

The bond market is reading the same signals. GSCRED sold $750 million of notes on Tuesday, a day after OBDC sold $400 million of bonds, the first BDC offerings since February. The GS deal priced at 255bps over, about 30 bps tighter than initial price talk. The Blue Owl notes priced at 270bps with a 6.5% yield, rated Baa2/BBB-.

The interesting detail on the Blue Owl deal: PIMCO bought the entire $400 million offering. This is the same PIMCO whose president said last month that the firm was staying away from “pretty bad loans” being sold by funds meeting redemption requests.1 Public caution about private credit loan quality in one breath, $400 million deployed into BDC unsecured debt in the next.

Either way, the deal only exists at these terms because of the stress PIMCO was publicly warning about. Another actor whose public commentary and capital deployment tell slightly different stories.

The Marks Memo Is a Fundraising Document

Howard Marks’ “What’s Going on in Private Credit?” was widely circulated last week. The diagnosis was historically grounded and broadly accurate: direct lending grew too fast, attracted too many inexperienced managers, and produced a goldrush where standards collapsed. Software concentration became the sector’s biggest risk because of how the capital stack evolved, not by accident.

The part worth reading more carefully is the pivot.

After 4,000 words building the case for why the market is broken, Marks shifts to explaining why Oaktree isn’t. Private credit is well under half of their performing credit assets. Direct lending is less than half of their private credit book. Software exposure is “extremely small on an absolute basis and relative to peers.” 80% of their private credit capital is institutional. The memo builds the case for an industry in trouble, then presents Oaktree as the exception.

Oaktree/Brookfield runs opportunistic credit funds that deploy into exactly the kind of stress the memo describes. The memo creates the fear. The fund deploys into the fear. That mechanism is as old as alternative asset management, and it doesn’t make the analysis wrong. But keep it in mind when the memo gets passed around the desk as though it were written by a neutral party.

There’s a detail the memo doesn’t mention. Oaktree Specialty Lending (OCSL) has a negative individual outlook from Moody’s. Marks wrote 6,000 words about the fragility of everyone else’s direct lending book while his own publicly traded BDC is on negative watch by Moody’s.

The Opportunistic Funds Tell the Same Story From the Other Direction

Moody's downgraded the BDC sector last week. The same week, the largest opportunistic credit fundraises in a decade closed.

Blackstone Capital Opportunities Fund V closed at over $10 billion. Ares Special Opportunities Fund III at $9.8 billion. Guggenheim Private Debt Fund IV at $8.4 billion. Adams Street raised $7.5 billion for its 3rd private credit vehicle, more than double its prior vintage. Record numbers, raised in the worst sentiment environment for private credit in a decade.

The Adams Street raise is particularly telling. The fundraise took roughly a year, meaning it stretched across Liberation Day tariffs, the SaaSpocalypse, the Iran war, and the entire BDC redemption wave. Bill Sacher, Adams Street’s head of private credit, said institutional investors are “a little less prone to headlines and a little bit more informed about what’s going on with the underlying investments.” That’s someone who just raised $7.5 billion telling you the BDC crisis didn’t matter to his LP base. About 40% of the commitments came from outside the US.

The pitch for every one of these vehicles is built on the same foundation: direct lending funds are gated, software loans are repricing, spreads are 100 bps wider than they were 18 months ago, and this is the best deployment vintage since 2009. The pitch is probably right. New-issue direct lending spreads have moved from SOFR + 450-475 to SOFR + 550-575. Covenant-heavy volume is up. The data supports the thesis.

What makes it interesting is the circularity. Blackstone runs BCRED, which is under gate pressure. Blackstone also just closed a $10 billion opportunistic credit fund to deploy into the opportunity BCRED’s stress is helping create. Ares runs non-traded BDCs with elevated redemptions. Ares also just closed a $9.8 billion special opportunities fund. These firms aren’t picking a side. The gated fund generates the stress narrative. The opportunistic fund monetizes it. Both vehicles sit on the same platform, managed by teams that share research and deal flow, marketed to different LP bases with different stories about the same market.

The Defense Is Equally Positioned

Cliffwater’s “Ten Misconceptions About Private Debt” published a detailed rebuttal to the negative private credit narrative last week.

They argue credit health metrics remain below historical stress averages: non-accruals at 1.3% versus a 2.1% long-term average, credit losses at 0.64% against a 1.0% average. Portfolio cash flow has historically averaged 8.4% per quarter, well above the 5% redemption cap. Private debt valuations aren’t smoothed, and Cliffwater’s research shows private loan price drops actually exceed subsequent realized losses, meaning marks are conservative.

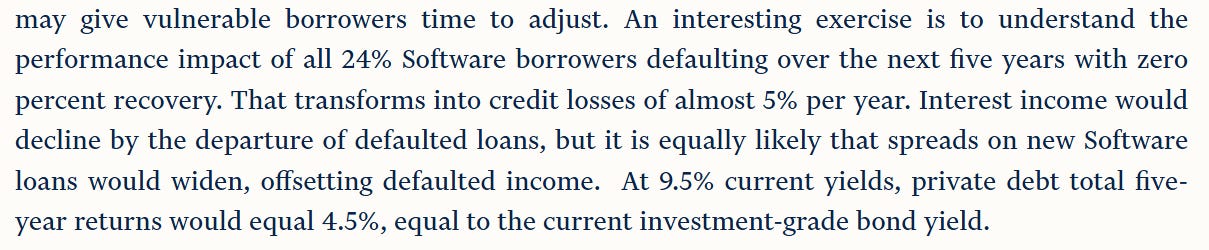

Their most provocative number: if every single software borrower in the private debt universe defaulted over five years with zero recovery, portfolio-level total returns would still come in around 4.5% annualized. That matches the current investment grade bond yield. The carry eats the losses even in a doomsday scenario.

Cliffwater also created the Cliffwater Direct Lending Index, the main benchmark for the asset class, and manages interval funds invested in private debt. The defense of the asset class is also a defense of the franchise.

Bain went a similar direction, telling Barron’s that private credit isn’t a bubble and software isn’t the real issue, disclosed 10-15% software exposure, and noted that Bain doesn’t have a retail problem because it prioritizes institutional and ultra-high-net-worth clients. The interview reads as reassurance directed at existing and prospective LPs wondering whether Bain has the same vulnerabilities as Blue Owl.

The Banks Want You to Notice They’re Fine

Jamie Dimon’s annual letter gave private credit the backhanded compliment treatment. He said the market “probably does not present a systemic risk,” pointing to its $1.8 trillion size relative to much larger asset classes. Then he spent several paragraphs cataloguing everything that could go wrong: weakening standards, generous add-backs, weak covenants, growing PIK usage, aggressive private ratings, poor transparency, and the likelihood that retail investors will seek legal remedy if things deteriorate.

The framing sounds like concern. Read the context.

JPMorgan disclosed $50 billion in private credit exposure this week. Wells Fargo reported $36 billion. Citigroup reported $22 billion. Dimon said on the analyst call he’s “not particularly concerned” because banks sit behind substantial loss cushions. Wells Fargo showed a 40% loss buffer with the ability to adjust margins dynamically if collateral performance deteriorates.

Compare that to the BDC liability side. Moody’s flagged that BCRED’s five-year notes widened from ~180 bps to the upper 200s. Unsecured debt issuance is still possible for the largest BDCs but increasingly uneconomical, pushing them toward secured borrowing and all the structural subordination that entails. The banks are funding at tighter spreads with more flexible terms. The BDCs are watching their cost of capital rise in real time.

The banks aren’t worried about contagion. They’re establishing themselves as the safer, better-capitalized alternative. If retail money is leaving private credit, the banks want to be where it lands next. If private credit lenders are pulling back from software and middle market lending, the banks want to fill the gap. Matt Levine made the point cleanly in his Bloomberg column yesterday: you could imagine banks gloating, and some of them basically are.

What Nobody Is Incentivized to Say

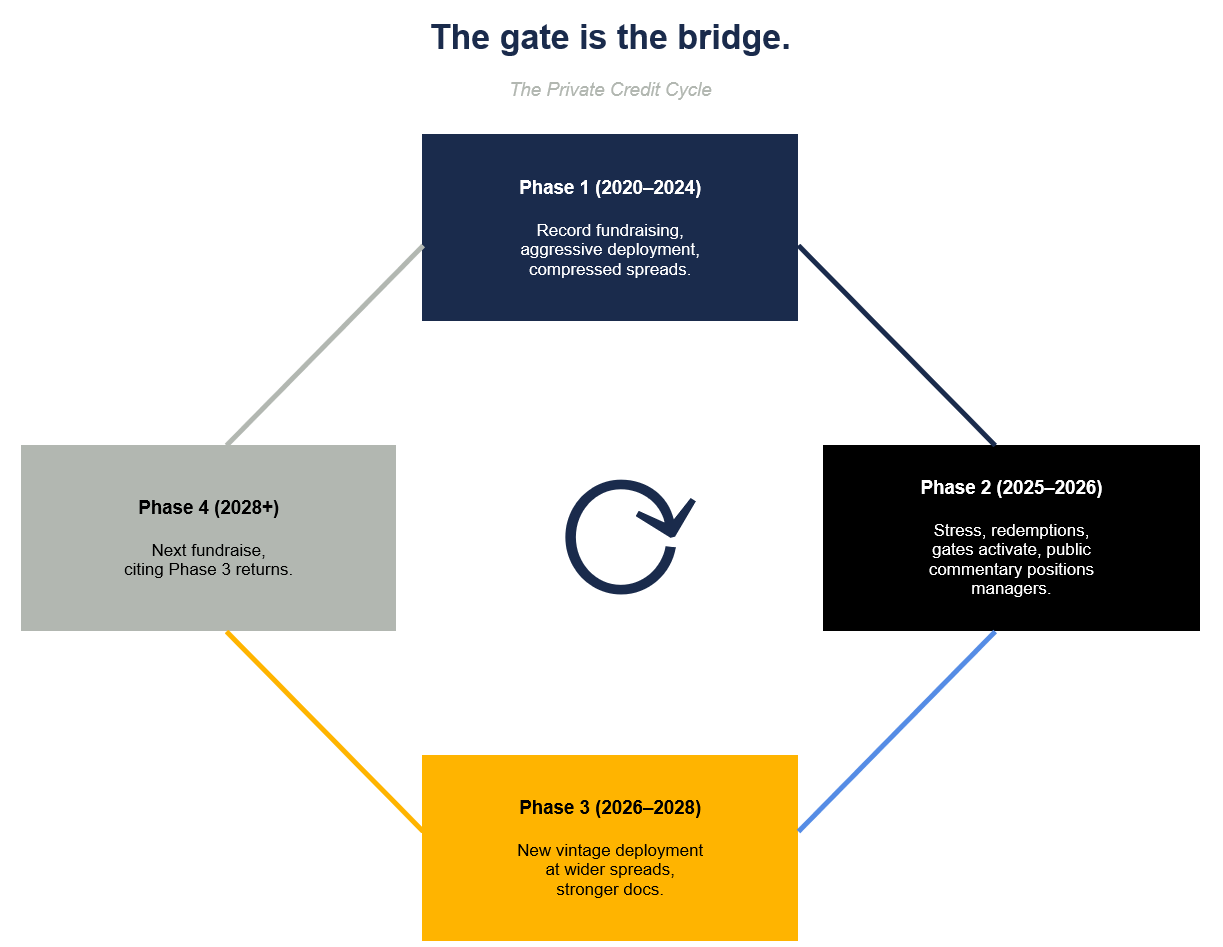

The private credit market may be going through exactly the mid-cycle repricing the asset class needs. Spreads are wider. Documentation is tighter. Leverage is lower on new deals. The capital that compressed terms and enabled sloppy underwriting is trapped behind gates or heading for the exits. By the standards credit investors actually care about, the lending environment is better than it was 18 months ago.

The biggest beneficiaries of that improvement will be the same firms whose retail fundraising excesses created the problem.

The managers who raised too much retail capital and deployed it into software loans at S+450 are gated now. Bad for their current funds. But the gate is creating the wider spreads and stronger docs that will make the next vintage significantly better. The worse this cycle gets for 2021-2024 vintages, the better it gets for 2026-2028 deployment. The same platforms will raise those funds. They’ll point to the improved environment as evidence they’ve learned their lesson and they’re now deploying into the best opportunity set in a decade.

Every piece of public commentary in the past week is laying the groundwork for that pitch.

Marks is positioning Oaktree as the disciplined manager who saw it coming. Goldman is positioning as the institutional-quality platform that avoided the retail mess. The opportunistic funds are positioning their deployment vintage as the post-correction opportunity. The banks are positioning for market share recapture. Cliffwater is positioning the asset class itself as resilient and misunderstood.

The gate is what makes all of these positions coexist. It prevents the stress from becoming a liquidation event. That’s the function everyone talks about. The function nobody mentions is that the gate bridges vintage cycles. It holds the current portfolio together long enough for the next fund to launch. It lets the stress generate the track record dispersion that makes “manager selection matters” a credible pitch. Boom, correction, recovery, new fund.

Next time you read a shareholder letter or an investor memo about private credit, ask one question. What is this person raising, and how does this story help them raise it?

If you liked this, you might also like:

Disclosure: The information provided is based on publicly available information and is for informational purposes only. While every effort has been made to ensure the accuracy of the information, the author cannot guarantee its completeness or reliability. This content should not be considered investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release the author from any liability. Always seek professional advice tailored to your financial situation and objectives.

OBDC is a publicly traded BDC and doesn’t face the same redemption pressure as the non-traded vehicles. But Stracke’s comments were about private credit loan quality broadly, not just the semi-liquid wrapper.

a very smart article

Your series on private credit comes at a crucial time. We provided highly structured data on debt capital, sourced from 8-K filings the moment they hit the EDGAR database. Sharing in case this type of data complements your research https://terrainlabs.substack.com/p/credit-roundup-april-13-17-2026.