EchoStar ($SATS): Is This The Cheapest Way to Buy SpaceX Before the IPO?

The back-of-envelope math looks compelling. But are you actually buying at a discount?

A year ago, EchoStar was on the verge of bankruptcy

Today it owns ~2% of SpaceX.

That is not a typo. In the span of 12 months, a leveraged spectrum holding company with a wall of near-term debt maturities and a half-built 5G network bleeding cash has transformed into one of the most interesting equity stories in the market. The inflection point was the SpaceX deal: $8.5 billion in cash and $8.5 billion in SpaceX equity in exchange for spectrum licences that EchoStar had been forced to sell anyway.

The question investors are now asking is simple.

SpaceX is reportedly targeting a $2 trillion-plus valuation in an IPO that could happen in weeks. At those levels, EchoStar’s stake is worth over $40 billion. The stock trades at a ~$37 billion market cap. So are you buying SpaceX at a discount through EchoStar, or has the market already figured that out?

That back-of-the-envelope math is exactly what most people are doing. The problem is that EchoStar is genuinely complicated. Most of what is being posted online is missing those details.

There was a Restructuring Support Agreement signed last month that changes the DISH DBS capital structure in ways that are not obvious from the headlines. There are intercompany loans and a waterfall of pre-committed AT&T proceeds that reduce what actually flows to holdco equity. There are tax considerations that most analyses ignore entirely. And there are operating businesses in various states of distress, including one with a debt maturity four months away that the bond market is pricing at 75 cents on the dollar.

Maybe none of it matters. Maybe the SpaceX narrative is powerful enough to override everything else. But I think you should know what you are buying before you decide that.

This piece is not an attempt to debate whether $2 trillion is the right number for SpaceX. That deserves its own analysis. The goal here is narrower: to work through the full sum-of-the-parts and figure out whether you are buying EchoStar at a meaningful enough discount to make it worth owning indirectly, vs. simply waiting and buying SpaceX when it goes public.

That is the question worth answering.

How We Got Here

You can find the full history elsewhere, so I will keep this brief.

EchoStar started life as a pay-TV company. DISH Network was for decades one of the two major satellite television providers in the United States, competing directly with DirecTV for the roughly 20 million American households that subscribed to satellite TV. It was a good business for a long time.

As that business began its secular decline, Charlie Ergen (co-founder/chairman) made a bet that spectrum would become the most valuable resource in wireless. Through a series of FCC auctions starting in the 2000s, DISH accumulated one of the largest spectrum portfolios in the country, spanning AWS-3, AWS-4, 600MHz, 3.45GHz, and several other bands. The thesis was that eventually the major carriers would need that spectrum badly enough to pay up for it.

The problem was the FCC had other ideas. It attached aggressive buildout requirements to the licences, forcing EchoStar to actually construct a 5G network rather than simply sit on the spectrum. The company spent years and billions of dollars building that network, acquired Boost Mobile from T-Mobile in 2020 to have a retail wireless presence. By 2025, it was burning cash at an alarming rate with a going concern disclosure and over $20 billion of debt.

Then the FCC came calling again, this time threatening to reclaim licences that EchoStar had not fully built out. Rather than fight a prolonged regulatory battle, Ergen did what he has always done: turned a problem into a transaction.

The spectrum sale to AT&T in August 2025 and the deal with SpaceX in September 2025 resolved the FCC dispute, retired the most pressing debt maturities, and in the process handed EchoStar a stake in the most valuable private company in the world.

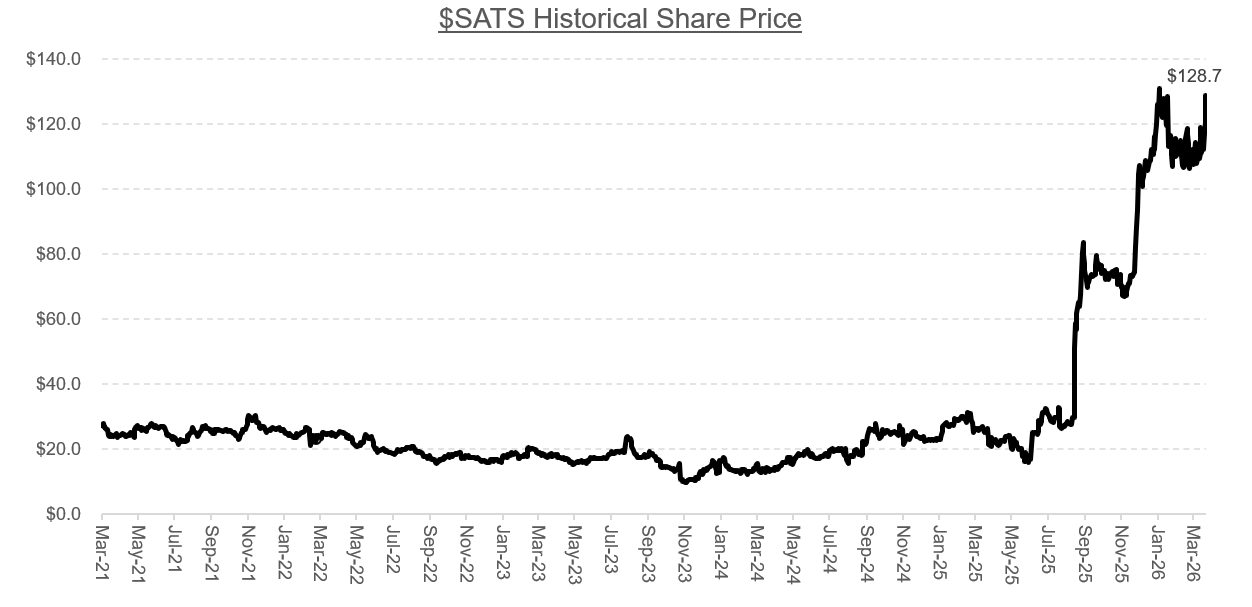

In the process, the stock has more than 5x’d, rallying from the teens to nearly $130 as the narrative shifted from near-bankruptcy to SpaceX proxy.

Sum of the Parts

The stock has re-rated dramatically to reflect the new reality, but whether it has re-rated enough, or too much, requires actually working through the numbers. So let us do that.

The way I think about EchoStar is in five buckets. The first is contracted cash: signed, binding deals where the amounts are fixed. The second is the three operating businesses. The third is the remaining spectrum. The fourth is the holdco deductions, which reduce what ultimately flows to equity holders. The last and most important is the SpaceX equity stake.

Starting with the easiest.

Bucket 1: Contracted Cash ($33.2 billion)

EchoStar has signed two deals that together guarantee $33.2 billion of cash inflows regardless of what happens to the operating businesses or the SpaceX stake.

The first is the AT&T spectrum sale: $22.65 billion for the 600MHz and 3.45GHz licences. Signed in August 2025, pending FCC approval, expected to close mid-2026. The largest spectrum transaction in US history.

The second is the SpaceX deal, signed in September 2025: $8.5 billion in cash for the AWS-4 and H-Block spectrum plus international S-band rights. On top of that, SpaceX contractually committed to fund $2 billion of interest payments on EchoStar’s outstanding debt through November 2027, effectively meaning SpaceX is servicing part of EchoStar’s balance sheet for the next 18 months. That brings the SpaceX cash package to $10.5 billion.

Combined: $33.2 billion of contracted, signed, committed cash. Not contingent on any valuation, not dependent on finding a buyer, not subject to negotiation. The only remaining step on the AT&T deal is FCC sign-off, which is widely expected given the current regulatory environment.