Private Credit Unfiltered: Match-Funded

Everyone says the gates are working. Nobody is talking about what happens when the loans come due.

Everyone loves to say these products are working exactly as designed.

The gates go up, redemptions get managed, the 5% quarterly cap does its job. Apollo’s Jim Zelter went on Bloomberg last week and said as much. Properly structured. Properly disclosed. The rules were clear.

He said this right before Blue Owl announced 40.7% redemption requests.

The whole structure rests on one assumption: that the loans mature when they’re supposed to.

The people saying everything is fine are correct about today. The gates are holding. But the match-funding argument gets tested in 2028, when the software maturities arrive and the borrowers who can’t refinance need more time. If the redemption queue is still running when that happens, the liquidity mismatch isn’t a sentiment story anymore.

And just to be clear about what we’re actually talking about. This is about one specific product, the non-traded BDC, sold through wealth channels to retail and HNW investors who were told they were getting private credit returns with semi-liquid access. Institutional direct lending is a different business. Publicly traded BDCs are a different conversation.

Why the Timing of These Loans Matters More Than People Think

When people say a BDC is match-funded, they mean the timing works.

Loans mature, cash comes in, investors who want out get paid, the vehicle continues. The liabilities are gated because the assets aren’t liquid on demand. You accept quarterly liquidity with a 5% cap because the yield compensates you, and the whole structure balances because the loans actually mature on schedule and produce the cash flows the model assumed.

But if the loans don’t mature on schedule, cash doesn’t arrive on schedule. The vehicle has to fund redemptions from somewhere else: new investor capital, bank lines, CLO proceeds, secondary loan sales. Each of those sources has a cost and a limit. I talked about hierarchy of redemption pressures last week.

Right now, each of those limits is being tested simultaneously.

New investor capital, the cleanest source, is slowing. Inflows turned negative in Q1 for the first time. Bank lines are tightening. JPMorgan is restricting lending to some private credit funds after marking down loan values in their portfolios. Meanwhile, CLO issuance is running near record pace partly to fill that gap.

$9.5 billion in CLOs issued so far this year. Near the 1Q’24 record. People in the industry call it capital stack diversification. It’s also a funding gap getting papered over with securitization.

Notably, BDCs are retaining the junior tranches of these CLOs. The equity and mezz pieces that absorb first loss. Citigroup estimated total BDC exposure at roughly $12 billion, about a third of all junior capital in the private credit CLO market. The leverage inside the BDC gets extended one level further inside the securitization, in a way that doesn’t surface cleanly in the headline debt-to-equity ratio.

The secondary market is now asking those same assets to clear at those same marks (they won’t).

More private credit loans for sale right now than at any point in this market’s short history. Goldman, Morgan Stanley, JPMorgan, Jefferies, all running processes. Asking prices near par. Bids not meeting them. One direct lender put it simply: buyers aren’t there in a systematic way at par, and the bid-ask spread remains very wide in reality.

That’s the only independent price signal available on loans otherwise valued by the people who own them. Right now that signal and the quarterly NAV are not saying the same thing.

All of that matters, but only because it tells you the same thing: the market is already rejecting the marks. The core problem is what happens when the maturities arrive and the borrowers can’t refinance.

The BREIT Comparison and Why It Breaks Down Here

The industry’s response to all of this has been consistent: the gate is working as designed, the structure is sound, BREIT proved the model.

It’s worth taking that argument seriously because it’s not stupid.

BREIT gated in 2022. Blackstone held firm. Investors asked to withdraw roughly 20% of shares at the peak. The fund fulfilled 100% of requests over a fourteen-month period. The assets recovered, sentiment normalized, and the vehicle survived. The industry has been banking on that outcome ever since. It became the template. It became the answer to every skeptic.

The argument being made right now, explicitly in industry whitepapers and implicitly in every shareholder letter, is that non-traded BDC redemptions are market-driven rather than performance-driven. Sentiment is the problem, not credit quality. The underlying loans are healthy. The gates buy time for sentiment to normalize, just like they did for BREIT.

That argument works if the underlying assets are actually fine.

BREIT’s assets were buildings. Stabilized real estate. Class A industrial, multifamily, things that exist independent of the capital structure sitting on top of them. When Blackstone said trust us, the assets are fine, they were making a claim that could eventually be tested against observable transactions in the same markets. The gate bought time for sentiment to catch up to fundamentals, and the fundamentals turned out to be intact.

Non-traded BDC assets are middle market loans. Many of them to software companies. These are businesses that went to private credit because the syndicated market passed. The spread you earned was the market’s way of quantifying the risk you were absorbing. When a non-traded BDC says the portfolio is resilient, they’re making a claim that’s much harder to verify, on assets valued by the same manager that originated them, held them, and has every incentive to keep them at par.

The BREIT playbook assumed the problem was sentiment and sentiment heals. The assumption in that entire framework is that redemptions are market-driven, not performance-driven.

The BDC question is whether the software maturity wall is the scenario where that assumption breaks down. If the 2027 to 2029 maturities don’t refinance cleanly, redemptions stop being a sentiment problem and start being a cash flow problem. Those are different situations with different endings, and running them together in shareholder letters is doing investors a disservice.

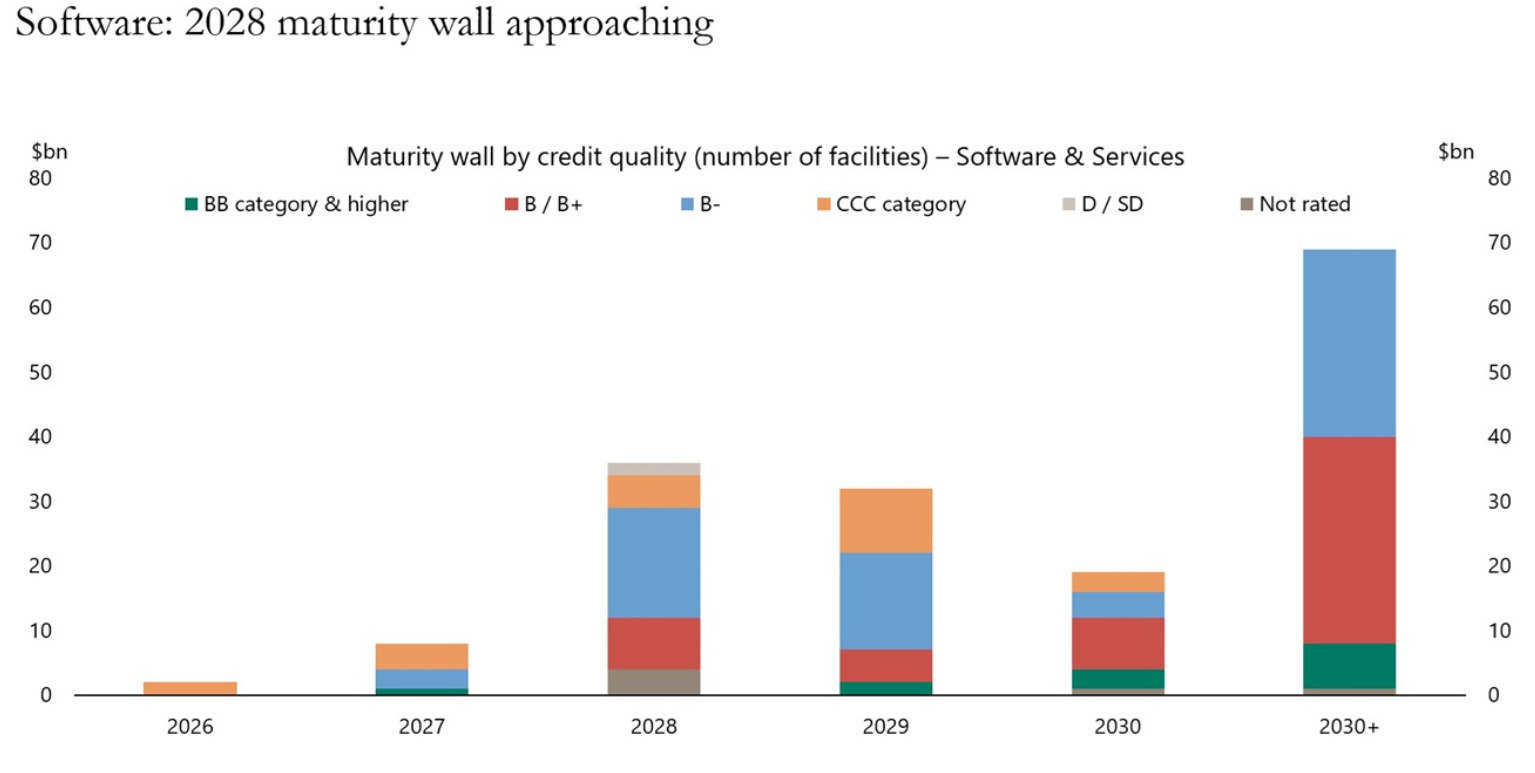

The Software Maturity Wall Is Coming

We’ve covered this multiple times now. The private credit boom in software lending peaked roughly 2021 to 2023 by most estimates. Sponsor-owned software businesses, many taken private at elevated multiples, borrowed heavily from direct lenders at spreads that reflected both the illiquidity premium and the credit risk the syndicated market didn’t want to absorb.

Those maturities start coming due in 2028 in a major way

And the default backdrop they’re maturing into is not benign. Morgan Stanley estimates the private credit default rate reaches 20% in the current cycle, approaching the sector’s historical stressed peak in 2009.

Some of those businesses will be fine. Revenue held up, the model worked, they refinance cleanly. That happens. Probably more often than the bears want to admit, and it’s worth saying that a performing software business with stable cash flows and a credible growth story gets refinanced. The match-funding argument works. The gate was never really tested.

Some will be genuinely impaired. The business deteriorated, the sponsor is deeply underwater, there’s no equity value left to protect. In those cases lenders take the keys. They stop waiting for a refinancing that was never coming and run the business for cash instead. Lenders in that position often do reasonably well. First lien, recurring revenue, a software business that still functions even if the growth story is gone. Operating it for distributions beats waiting for a par recovery that isn’t there.

Medallia is probably heading there. Thoma Bravo called the $6.4 billion take-private a “mistake.” The paper is being shopped in the secondary market right now. Nobody is offering par. The lenders who end up owning it may not have a disaster on their hands. They have a software business. They’ll run it for cash.

The clearly impaired credits get resolved. That’s not where the structural problem lives.

The Middle Is Where It Gets Complicated

The problem cases are the ones that aren’t clearly fine and aren’t clearly impaired.

Not good enough to refinance cleanly into the 2027 market. Not bad enough that the sponsor hands over the keys. A business that’s technically performing, still generating revenue, sponsor still holding out hope for an exit, but rates are higher than the original underwriting assumed, growth has slowed, and the syndicated market isn’t going to touch it at a price that works for the capital structure.

That borrower and that lender sit down and have a conversation. The lender can mark the loan down and take the loss. Or extend the maturity, collect an amendment fee, and give the business another eighteen months.

Think about what marking down actually means in this context. It’s not an accounting entry. If NAV goes down, more investors head for the exit, the fund sells assets into a market that won’t pay par. Nobody in that seat marks down if they can avoid it.

So you extend. The fee gets collected. The loan stays at par. The quarterly letter reports a resilient portfolio.

Some of those extensions will work out. The business stabilizes, a refinancing happens in 2028 or 2029, the lender gets paid. The extend decision was correct. This is the base case the managers are implicitly assuming when they say the portfolio is resilient.

Some won’t. The extension buys time the business uses to get worse rather than better. Now the lender is holding a more impaired credit at the same par value, two years later, in a vehicle that has been funding redemptions from bank lines and CLO proceeds the whole time.

Non-accruals stay low throughout all of this. An extended loan is technically performing. A loan restructured to pay interest in kind rather than cash is not in default. The statistic is accurate and misleading at the same time, which is a recurring feature of how private credit health gets reported.

The match-funding argument doesn’t require every borderline credit to go bad. It just requires enough of them to extend rather than mature that the cash flow timing stops working the way the model assumed.

What the Redemption Queue Is Actually Telling You

Last quarter investors asked to pull 40.7% of Blue Owl’s tech-focused BDC, OCIC. Nearly 22% from the flagship. Both funds enforced the 5% cap. More than $4 billion is now sitting in the queue.

OCIC has $11.3 billion in liquidity. OTIC has $1.3 billion. The funds can meet the 5% cap for now, and probably for a while. It’s worth highlighting that the near-term liquidity is real, the gates are holding, and the managers saying they’re well-positioned to meet upcoming tenders are not wrong about today.

The real problem is that this gets ugly on a timeline longer than one quarter, which is exactly why people keep hand-waving it away.

A 5% quarterly cap on a fund facing 40% redemption requests means the queue takes two years to clear under static assumptions, with no additional requests. Two years during which investors at the back of the line are holding a vehicle that’s paying out the more motivated investors first, while the 2027 and 2028 software maturities are arriving and being evaluated one by one.

Corbin Capital’s John Cocke put it plainly: if outflows hold at 5% per quarter for a year, it becomes “an existential question of the vehicle.” Not a prediction. A description of the math.

Moody’s cut the sector outlook to negative this week. $14 billion in Q1 redemption requests. The proration psychology is now in motion: investors watching peers get gated and deciding to queue before the window closes further. Once that dynamic sets in it’s genuinely hard to reverse.

The industry’s own scenario analysis, modeled on BREIT, assumes requests peak around 20% for a couple of quarters and then normalize over three to five quarters. That’s the optimistic path. It assumes the underlying credits are healthy, sentiment is the driver, and time solves the problem.

The Question Nobody Is Asking

Last week the Department of Labor proposed rules that would move private credit into 401(k) retirement portfolios. Scott Bessent called it the beginning of a Golden Age.

The week after Moody’s cut the sector to negative. After $14 billion in Q1 redemption requests. After Blue Owl disclosed nearly half of one fund’s investors trying to leave.

Nobody in Washington reads the filings.

Doug Ostrover said two weeks ago, about the mismatch between what investors expected and what the structure actually provides: “Between us, and the advisers who sell our products, I don’t think we made it clear enough.”

Here’s the question the industry’s BREIT framework doesn’t answer. BREIT worked because the assets were fine and time solved the problem. The entire non-traded BDC defense right now rests on the same assumption: redemptions are sentiment-driven, credit quality is intact, give it a few quarters.

But what if the redemption cycle and the maturity wall arrive at the same time?

The queue is running now. The 2027 maturities start in roughly eighteen months. If a meaningful portion of the borderline credits can’t refinance at that point, the lenders extend. The NAV holds. The queue keeps running. New capital stays away because nobody wants to invest in a vehicle that’s prorating redemptions. The vehicle is now funding a persistent queue from a shrinking pool of maturing assets, bank lines that are tightening, and CLO proceeds that are getting more expensive.

This is going to be a slow grind. The kind that doesn’t make headlines until it’s already well advanced. The type where the quarterly letters keep saying resilient right up until they don’t.

Centerbridge’s co-founder said yesterday the current moment is a genuine entry point for experienced investors with real liquidity and long time horizons. He’s right. The distressed opportunity in private credit over the next three years is going to be significant, precisely because the A&E cycle creates the conditions for it.

But that opportunity accrues to the people on the outside looking in.

The people on the inside, in the queue, waiting on cash flows from loans that may or may not mature on the schedule the model assumed, are in a different position entirely. They’re in something that doesn’t have a clean historical precedent, because the last time a product like this was stress-tested, the assets were buildings and not software businesses facing an AI disruption cycle with a maturity wall coming due.

The gate held for BREIT because the problem was sentiment.

The question worth asking right now is whether the problem is something else entirely. And whether by the time we know the answer, the queue has been running long enough that the match-funding argument has already quietly failed.

Thanks for this clearly written piece.

There’s something eerie about a structure that works perfectly in the present while quietly depending on a future that hasn’t been tested yet. Everything clears, everything reconciles, everything looks orderly. Until timing itself becomes the variable that no one priced correctly.

The gate gives the illusion of control, but it’s really buying time from a future that may not cooperate. Cash flows that are supposed to arrive on schedule start drifting, then stalling, and suddenly what looked like discipline reveals itself as delay. The uncomfortable part is that nothing needs to break all at once. It just needs to arrive later than promised, long enough for confidence to erode before the numbers do.