Private Credit Unfiltered: What’s Behind the Gate

The Adverse Selection Nobody Is Talking About

You didn’t panic.

The quarterly report looked fine. The NAV hadn’t moved. Redemptions were being honored and the people rushing for the exit seemed like they were overreacting to headlines.

So you stayed.

Rational, patient, exactly the kind of investor the pitch deck described when they sold you this thing.

And while you were being patient, every liquid asset in your portfolio walked out the door with the people who panicked.

That’s the part nobody is writing about.

I’m starting a new weekly series on private credit. There’s a lot of noise out there right now, some of it alarmist, some of it too rosy. I’ll try to cut through it.

Everyone Is Writing About the Wrong Story

The coverage so far has focused on the managers. Who honored redemptions. Who gated. Who wrote the check to buy goodwill.

The headlines treat this as a story about institutional character. That is not your story. Your story is what happened to the portfolio while all of that was playing out.

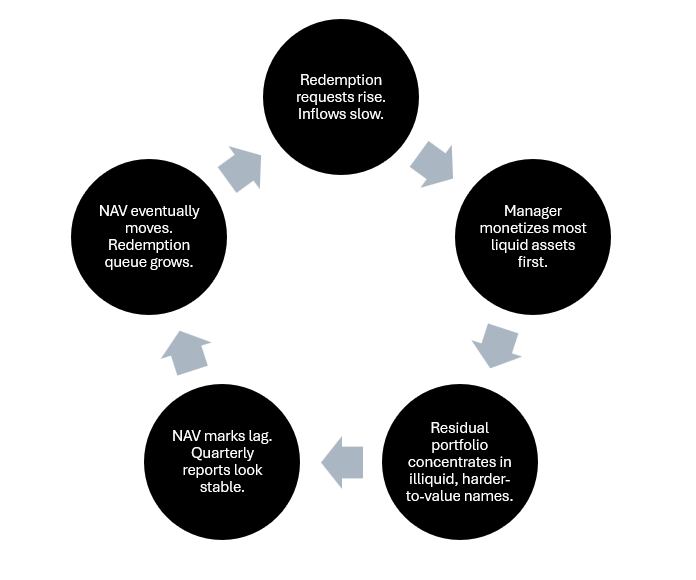

Redemptions at non-traded BDCs are rising sharply and gross inflows are slowing. At a few funds, outflows have already exceeded inflows. If that becomes widespread, the manager effectively has three levers.

Draw on credit facilities and issue debt. Some are doing exactly that. But re-leveraging a deteriorating collateral pool has limits, and the banks providing that leverage are paying close attention. JPMorgan has started independently revaluing private credit collateral used as loan security.

Find new equity inflows to replace what is leaving. That window is closing. Gross inflows slowed materially in the back half of 2025, and net flows across the private BDC cohort dropped sharply quarter over quarter.

Which makes asset sales the key pressure point if leverage and replacement inflows are insufficient.

Goldman Sachs estimates the retail private credit sector could shed between $45 and $70 billion in assets over the next two years, reversing growth that took the sector from $34 billion in 2021 to $222 billion by end of last year. The question that determines what happens to your capital is not which manager honored redemptions. It is which assets they sold to do it.

How You Fund a Redemption

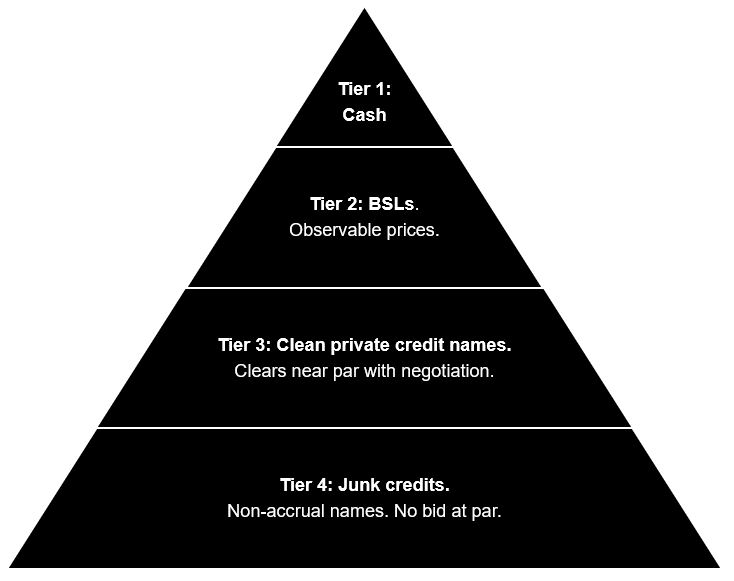

You don’t get to sell whatever you want when you’re under redemption pressure. You sell what has a bid.

Cash goes first. Then the liquid stuff (broadly syndicated loans if any), the ones with observable prices and real secondary market depth. Then the cleaner names, the credits a sophisticated buyer will underwrite quickly, close to par, without demanding a steep discount.

What’s left after that process is not random.

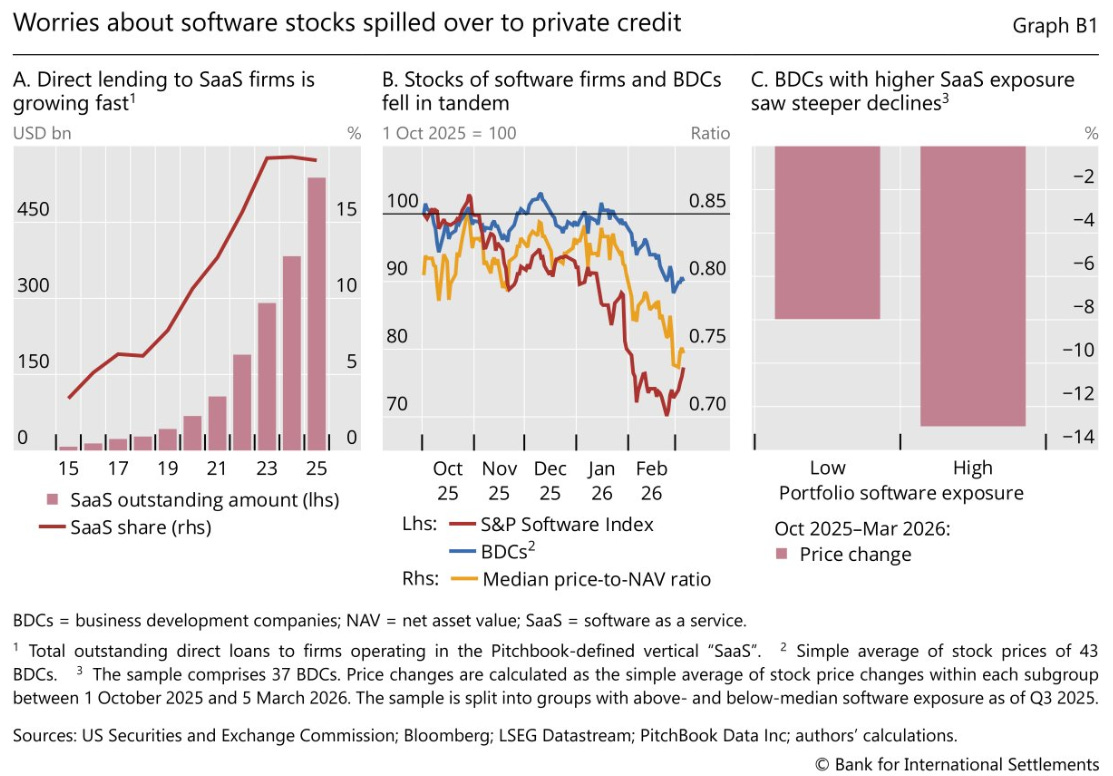

Heavily leveraged paper from 2021 and 2022, underwritten at 7-9x when rates were zero. PIK toggles. Names that are one bad quarter away from non-accrual. Software loans (which are under-represented) with AI disruption hanging over them.

The assets that remain are more likely to be the ones that didn’t find a bid. That is why they are still in your fund.

A handful of the largest managers have additional options. Blackstone injected $400 million of firm and employee capital to satisfy BCRED requests without touching the portfolio. Exceptional moves, available only to managers with institutional capital structures and balance sheets large enough to absorb the cost.

Most managers running non-traded BDCs are not Blackstone. Honored redemptions need to be funded somehow. The mix of how they get funded determines what you are left holding.

The Self-Selection Mechanism

The portfolio may deteriorate for two reasons at once: original underwriting quality, and a redemption process that selectively strips out the easier-to-sell assets first.

Every redemption cycle removes the assets with the most liquidity and buyer interest, leaving behind the ones with neither. Nothing in the disclosed data tells you the composition has shifted. But it has.

Here is what makes this particularly insidious. The headline credit metrics look fine.

Non-accruals across publicly traded BDCs have actually been falling. Loans are still “performing.” Borrowers are still paying, or PIK-ing with lender consent, but nothing has formally tripped.

That’s how private credit works. A loan doesn’t go non-accrual until there’s an actual payment default or a formal determination that collection is doubtful. Until then, it accrues. Sponsors and lenders have every incentive to amend, extend, and restructure their way around that moment. The reported metrics reflect what has already broken. They don’t reflect what is quietly deteriorating underneath.

The PIK data is where that deterioration becomes visible before it has to.

Lincoln International, which values more than 7,000 private credit companies each quarter, found that bad PIK, meaning PIK interest that was NOT part of the original loan structure but is now being utilized, sat at 6.4% of private loans in Q4 2025. Up from 6.1% the prior quarter. Up from 2.5% in late 2021 when Lincoln began tracking it. More than half of all PIK loans now feature this dynamic.

PIK loans are unlikely to leave in a curated portfolio sale. They stay, compounding deferred interest, increasing the face value of the obligation while the enterprise value underneath may be going the other direction. The gap between carrying value and recoverable value grows quietly. It doesn’t show up in NAV until it has to.

The Secondary Market Won’t Save You

Some managers are trying to solve this by selling loan portfolios in bulk. Package the assets, find a sophisticated buyer, sidestep the liquidation hierarchy.

The problem is who the buyer is.

HarbourVest, Coller, Pantheon, the secondary arms of the big private equity shops. These institutions do this for a living. They know what a portfolio assembled under redemption pressure looks like. They know the clean assets cleared first. They price what’s left accordingly.

A manager trying to raise liquidity under a redemption deadline is not negotiating from strength.

Blue Owl’s $1.4 billion sale at 99.7 cents was celebrated as proof the system worked. Look more carefully at who bought it. CalPERS. OMERS. BCI. Blue Owl’s own Kuvare insurance affiliate. Four institutions evaluating a pre-selected slice in a negotiated process. That is the best possible execution on the most sellable assets in the book. For anything beyond that kind of curated pool, buyers will probably not pay par.

The next portfolio sale is likely harder. The one after that harder still.

When a secondary transaction clears at a meaningful discount, it becomes the first real observable market price for assets that previously existed only at manager-determined marks. Once that price is observable, every manager running a similar book has a problem. Which means the NAV you are looking at today may not be the one you are looking at next quarter.

The NAV Illusion

On the surface, nothing looks wrong. Stable marks. Assets sold at or near par. The manager’s letter references portfolio resilience.

But the composition of what remains has quietly worsened, and the NAV may reflect that only slowly, unevenly, or after a forcing event.

We already have real examples of how fast marks can move when a stressed book gets forced into the open. At BlackRock TCP Capital Corp, writedowns in Q4 2025 reduced NAV by 19% in a single quarter. Moody’s downgraded FS KKR Capital Corp to Ba1, one level into junk, citing non-accruals rising to 5.5% of total investments. This doesn’t mean every fund is next. It proves the speed of adjustment, when it comes, can be severe.

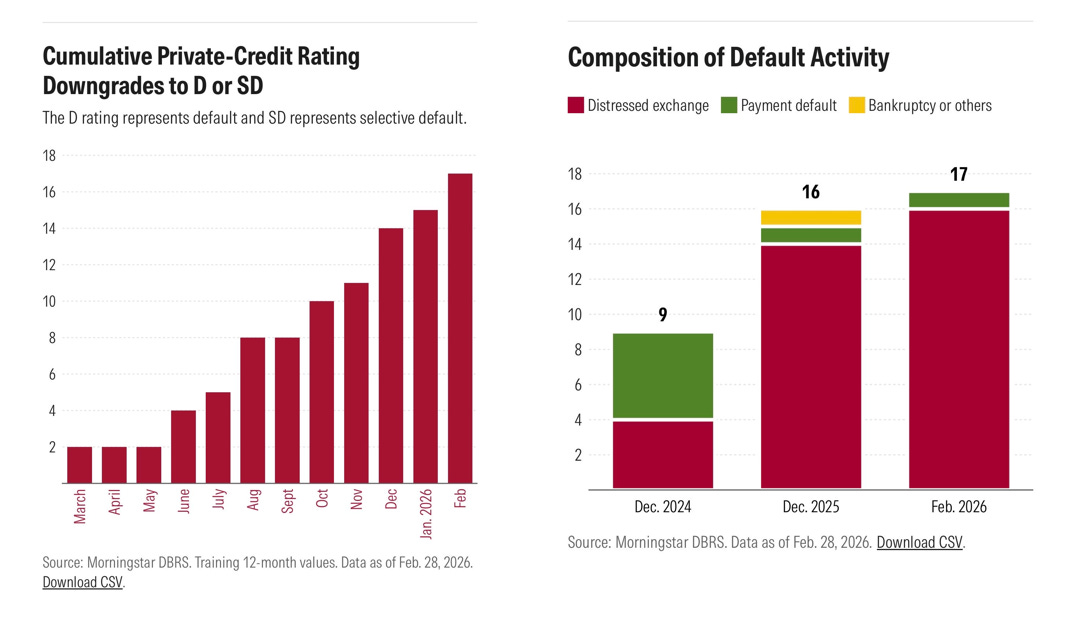

The default trajectory is moving. Morningstar DBRS recorded a 78% year-over-year increase in private credit default events in 2025. Distressed exchange transactions now account for 94% of all downgrades to default or selective default. Not hard payment defaults. Restructurings where lenders accept worse terms to avoid triggering a formal event. Extend maturities. Accept PIK. Loosen covenants.

And the assets that didn’t find a secondary bid, the software loans and PIK positions the sophisticated buyers passed on, are the same ones staring down a specific refinancing wall.

Over $160 billion in private credit software loans mature by 2029. These need to refinance in an AI-disrupted environment on timelines now measurable in months.

The mask slips when a secondary transaction clears at a visible discount, a forced sale implies the marks are wrong, or non-accruals start climbing because the cleaner names have already been sold.

When any of those happen, the loop tightens.

NAV moves. Queue gets longer. More assets sold. Portfolio concentrates further into the names with the fewest bids. A liquidity problem creating the conditions for a credit problem that doesn’t yet exist in the reported data. The investor in the middle of it, watching a stable NAV, may have no way of knowing how far along this already is.

You Are Holding What’s Left

Most of the coverage treats the redeeming investor as the protagonist. The one who read the headlines and got in line. That investor is out. Their problem is over.

You stayed. Maybe the quarterly report looked fine. Maybe you believed the NAV. Maybe you requested a redemption, got a fraction of what you asked for, and remained in the fund involuntarily. Either way you are now holding a concentrated position in the assets that survived the selection process. The clean paper is likely gone.

You are not holding private credit. You are holding what’s left of it.

The quarterly report next month won’t tell you that. The NAV will look roughly the same. The manager’s letter will sound the same. The non-accrual rate will look stable because the names approaching stress are still accruing, still marked at cost, still waiting for the quarter that forces the issue.

The instrument panel can look fine longer than it should.

The Structure Was Always the Problem

The non-traded BDC was designed to solve a distribution problem for asset managers, not a liquidity problem for investors.

Quarterly redemption windows against 5-7 year loan maturities was never going to hold under sustained stress. The industry watched this play out in non-traded REITs in 2022. Same structure, same redemption caps, same manager-determined NAVs, same retail investors discovering what semi-liquid actually meant when everyone reached for the exit at once.

Among BDCs with aggregate NAV over $1 billion, redemptions have already risen 217% quarter over quarter. Sixth Street said it directly: if the non-traded REIT segment is any guide, this capital flow dynamic will last multiple years.

Then the industry built the identical structure in private credit anyway, with more capital and a broader retail distribution network than the REIT market ever had.

Apollo moving toward daily NAVs is the right direction. Blue Owl eliminating the tender offer mechanism on OBDC II is a confession that the structure couldn’t hold, packaged as an orderly solution.

The managers who use this moment to genuinely redesign the product will own the next cycle of retail private credit inflows. The ones who rebuild the same structure will face this again, at larger scale, with less goodwill.

What’s Behind the Gate

The gate is not the story. The gate is the moment you find out what’s behind it.

What’s behind it is a portfolio that survived the redemption process for one reason. Not because the manager protected it. Not because the underlying credits are strong. Because the assets with bids left first.

You didn’t panic. You stayed. You trusted the quarterly report and the stable NAV and the manager’s letter.

None of those are the price at which the remaining portfolio clears today.

Private credit is not broken. The non-traded retail vehicle is. And the investors still inside it are holding something that looks exactly like what they bought, right up until the quarter it doesn’t.

Very nice article. I totally agree with the following…..”The non-traded BDC was designed to solve a distribution problem for asset managers, not a liquidity problem for investors.”

That’s essentially a bank run without a backstop. The only rational decision for an investor is to join the run; otherwise, you are left with worthless assets, and because there are senior creditors ahead of you, you could end up with nothing.