Credit Weekly: The Holdout Trade

The most contrarian trade in software credit isn't buying the dip. It's waiting.

Everyone’s trying to figure out the right move in software credit right now.

Here’s an idea: maybe the best trade is to actually do nothing.

You already know the setup. The 2028 software maturity wall. The AI disruption overhang. The terminal value problem we’ve been talking about the last couple of months.

The question was always whether the restructuring wave would be consensual or coercive. It won’t be. The lawyers are already circling and salivating.

So what’s next? If the sponsor plays nice, you get an A&E. The more cynical view, and the more likely one based on everything we’ve seen over the last three years, is that you’re about to get your collateral stripped.

Which raises the question nobody is asking: if that’s where this is going, is the holdout actually the better trade?

Here’s how it goes. The large holders negotiate themselves into new senior paper. They get their deal, they get their collateral back. Meanwhile if you hold out, and just the right number of other lenders hold out with you, the stub remaining after the LME might be small enough that the company just pays you back at par with cash on hand.

No negotiation or haircut. You waited and got paid.

At least, that’s the theory. Here’s what it looks like in practice.

How the Playbook Works

Bloomberg reported this week on Vibrantz Technologies, a paint-additives company owned by American Securities. The owner wouldn’t share restructuring details until lenders signed NDAs barring any communication with peers. Once lenders were siloed, the sponsor cut different deals with different groups.

I mean, c’mon!

The larger creditors got first-out paper. Smaller lenders were approached after the structure was already set, offered something worse, on a take-it-or-leave-it basis with 90% of the lender base already signed.

Scott Greenberg described it aptly:

“Weaponizing NDAs and side deals to prevent lenders from coordinating pushes the limits of the collective action provisions in credit docs that are supposed to require coordination.”

Supposed to.

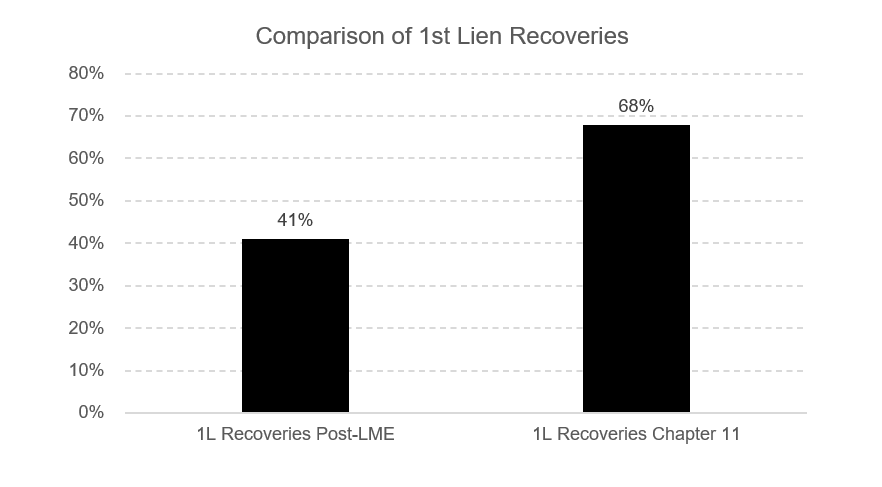

You probably already have a view on the recovery math. But the Fitch data is worth stating explicitly because it’s starker than most people realize. Companies that went through an LME before eventually filing recovered ~41 cents on first lien. Companies that skipped the LME and went straight to Chapter 11 recovered closer to 68 cents. You’d think that would slow things down. It hasn’t.

A Harvard Law paper from earlier this year found that a majority of coercively restructured firms end up filing anyway. The LME buys time. It doesn’t fix the balance sheet. And it leaves certain lenders materially worse off than a straight filing would have.

And it’s not evenly distributed.

The reason this matters now is timing.

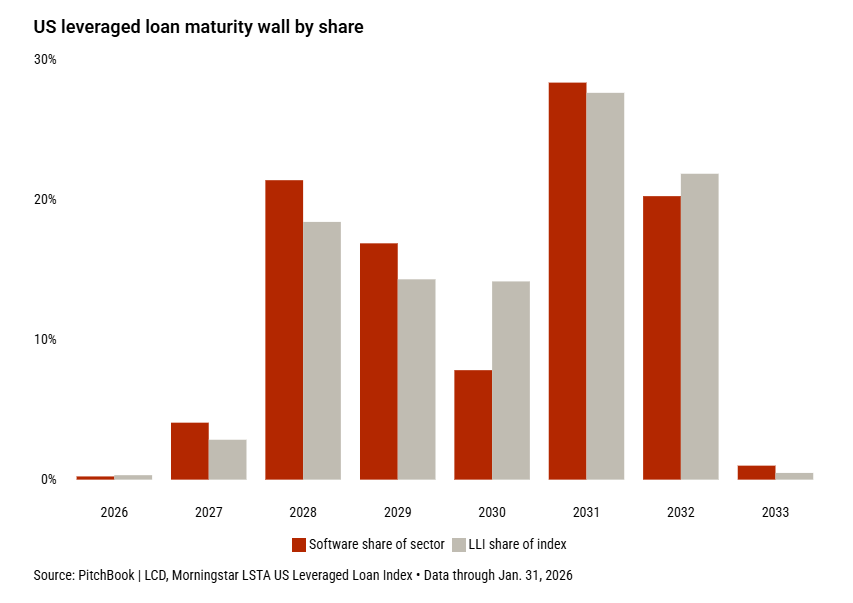

The 2021 vintage is the single largest entry class in the loan index by every measure, with a higher concentration of B3-or-lower borrowers than any vintage on record. 25% of outstanding software loans mature in 2027-28, vs. 21% for the broader index. A meaningful share of those issuers have already defaulted or completed an LME and the wall is still two years out.

The Trade

A lot of these companies are still cash flowing. The AI disruption thesis is real but it plays out over years. Operational deterioration is slow. Debt service is current. The maturity is the problem, not the business.

If the LME is designed to subordinate you, strip your covenants, and leave you in a worse structure, maybe the better trade is to not participate at all. Sit in the 70s on a 2028 maturity. Clip your coupon. The stub maturity that rings post-LME might produce a better outcome than fighting over collateral in a deteriorating negotiation while the sponsor extracts whatever value remains.

The holdout only works if the company doesn’t actually need to file. That’s the whole underwrite. You either believe the business survives to the maturity or you don’t.

But the nuance is the holdout only works as a minority strategy. If enough of the lender base sits on their hands, the maturity wall doesn’t get addressed, the company can’t refinance, and you’ve created the exact outcome you were trying to avoid. A room full of holdouts is just a default waiting to happen. And frankly, that might actually be the better approach if the Fitch data is any indication. It’s basically what’s playing out at Medallia.

It does mean however the actual research required might not be just identifying the right names. It’s understanding who else is in the capital structure and how much they own.

A dispersed lender base with no dominant holder gives the holdout room to work. A cap table where 2 or 3 large funds control majority economics probably doesn’t, because those holders have enough leverage to drive a negotiated outcome on their own timeline regardless of what you do.

Most people are spending their time trying to identify the right names. The smarter work right now is mapping the lender base. Both pieces of the analysis matter.

One more thing before moving on. This is predominantly a BSL and high yield issue. You can’t run the Vibrantz playbook on a unitranche. A single direct lender holding a $500 million club deal doesn’t get siloed behind an NDA the same way a dispersed syndicated lender base does.

Private credit has its own version of the vintage stress problem but the mechanism is different. That market will see its own restructuring wave but the form it takes is a separate question. I’ll be getting into this in Private Credit Unfiltered, my weekly private credit series. Check out the 1st edition below:

What the Pricing Is Telling You

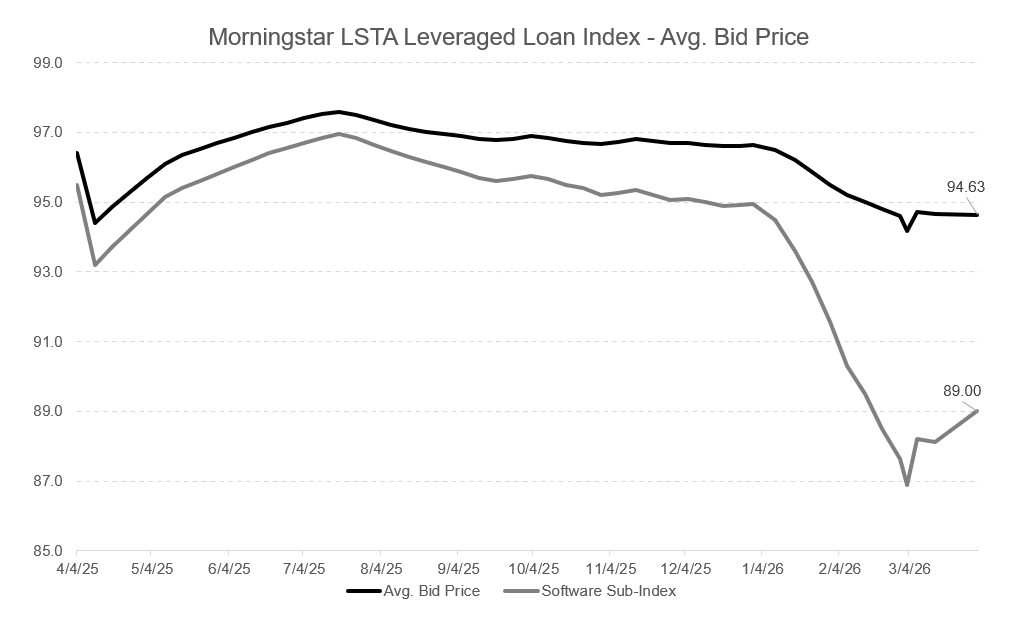

Software loans gained just over 1% in March, best month in nearly a year. Still down close to 6% YTD. The bounce got attention. The structural problem underneath it didn’t.

The bottom chart tells that story clearly. The software sub-index sits at 89 cents vs. 95 for the broad loan index. The divergence opened sharply in early 2026, partially recovered in March, and remains wide. The stabilization is real. It’s not a resolution.

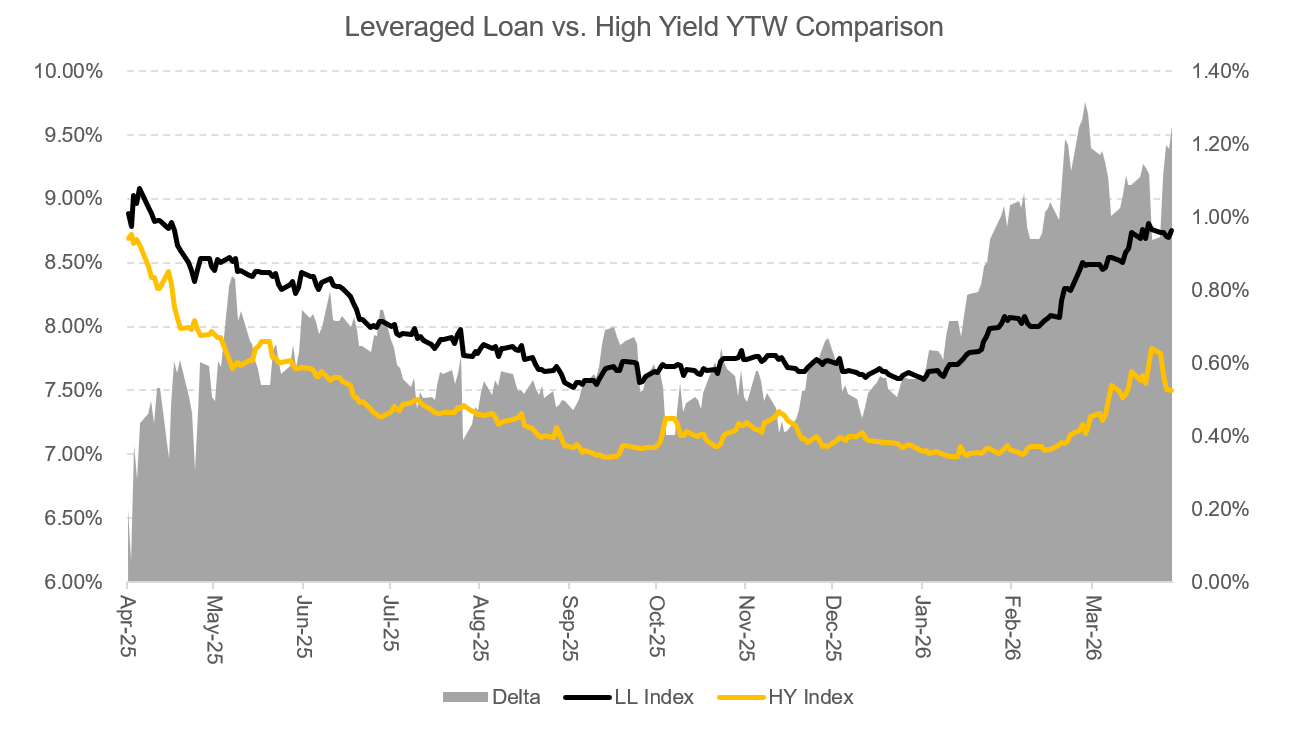

Loan yields came in around 8.75% this week, ~125bps above high-yield bond yields. The one-year average gap runs closer to 66bps and it normally runs in HY’s favor. Loans are floating rate, senior secured, shorter duration. They should yield less than bonds. Right now they yield substantially more.

Part of that gap is explainable. Forced retail outflows hitting loans with no equivalent on the HY side. CLO technical dynamics. Software concentration in the loan index that simply doesn’t exist in HY to the same degree. Some of this is structural and probably persists. The inversion alone doesn’t tell you loans are cheap.

For the names where the business is functional and the problem is the capital structure, the holdout might work precisely because the LME process is designed to give par to someone else. The large holders accumulate, negotiate their first-out paper, and move on. The smaller holder who didn’t participate, sitting in a 2029 maturity on a company still generating cash, collects coupon and waits.

Not every name or even most names. A specific subset the market is currently pricing like all the others.

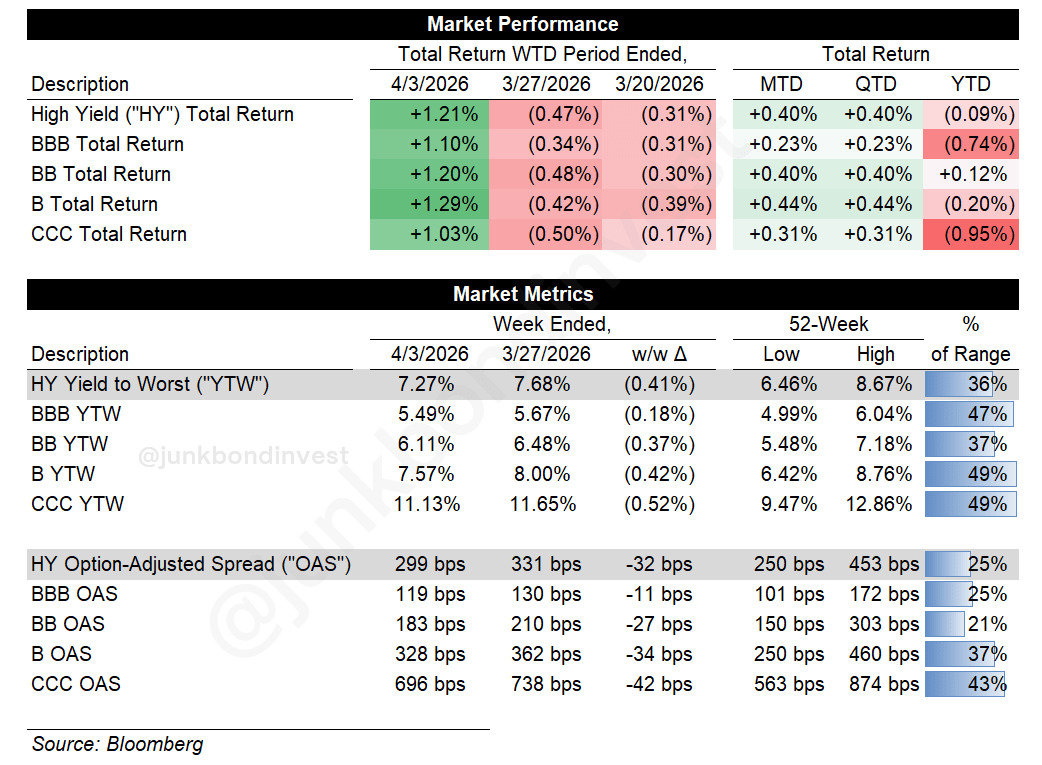

What the Week Said

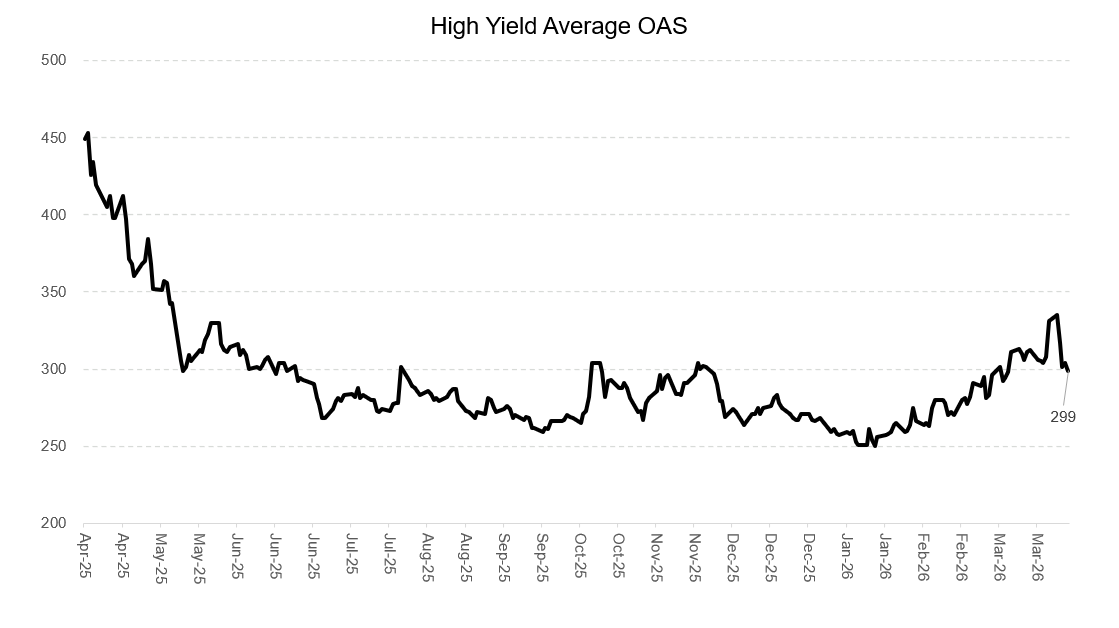

HY spreads tightened roughly 30bps this week. Index yields fell from 7.68% to 7.27%. Equities rallied hard, SPX up nearly 4% from the lows. VIX down too. The 10-year drifted back toward 4.3%. The market recalibrated from pricing a potential hike to none.

Brent crude barely moved.

That’s the disconnect worth sitting with. The commodity at the center of the conflict didn’t confirm what every other asset class was pricing. Two to three week ceasefire timelines have been floated repeatedly over the past month. The equity market tests into them, reverses on headlines, and tests again. This week felt like another iteration of that pattern rather than a genuine reassessment.

Selling in March was historically elevated and the trading community walked into April carrying a considerable short base. A lot of the week’s price action reflected that positioning getting squeezed, not a fundamental change in the outlook.

On Iran, the honest answer is nobody knows. Polymarket is pricing a 61% chance of ground invasion before 2027. Trump is threatening to bomb power plants. Iran rejected the Hormuz ultimatum and says the strait reopens only when war damages are fully compensated. Kuwait’s oil infrastructure got hit again over the weekend.

It does feel like we’re closer to peak negative sentiment than peak escalation risk, but I hold that view loosely. The short base is real, the positioning data supports a squeeze, and neither side has taken the next truly catastrophic step yet. That could mean we’re approaching an off-ramp. It could also mean the worst is still ahead. The market is betting on the former. The headlines are not confirming it.

What’s locked in either way is the economic damage. Inflation is going higher. Gas above $4 a gallon for the first time since 2022. Supply chains disrupted. A ceasefire tomorrow doesn’t undo any of that.

HY primary was quiet. March closed as the lightest month for HY supply since late 2025 and the lowest March total in three years. Four consecutive weeks of outflows above $1 billion each.

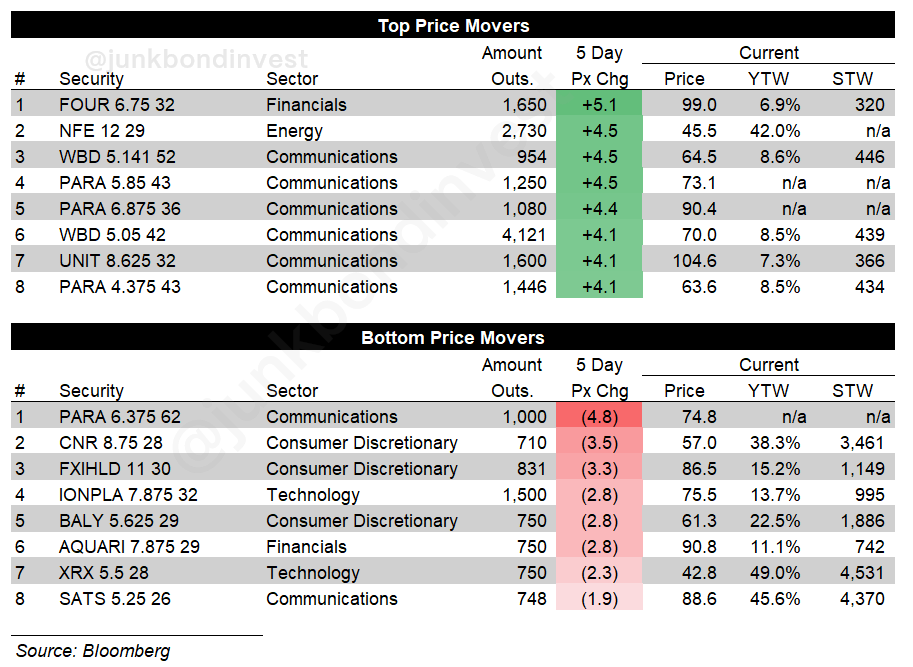

In the secondary, top movers included PARA/WBD, NFE, and UNIT, which rallied on M&A speculation. The bottom of the table was more telling: CNR hitting record lows, ION under pressure from the same AI overhang weighing on software credit broadly, and XRX debt weak.

Where This Leaves You

The LME wave is likely coming and most people in this market already know it.

The Vibrantz situation is an example of how it works. Fragment the lender base, assemble majority control behind an NDA, deliver a structure to the room that was negotiated without them. For most names in the distressed software cohort that process plays out the way it always does.

Be honest about what the trade actually is though.

If you’re an original lender who bought at par in 2021, the holdout framing looks different than it does on paper. You’re not choosing between a 41 cent LME recovery and par at maturity. You’re choosing between crystallizing a loss now or carrying a mark-to-market impairment for two years on the hope that a maturity rings clean.

That depends on your fund structure, your investor base, your ability to absorb the interim pain.

The holdout as described here is primarily a secondary market entry point. Buying in the 70s on a name where the business still works and the maturity is the problem. Most people aren’t talking about it that way.

The other thing most people aren’t doing is the lender base work.

A dispersed cap table with no dominant holder gives the holdout room to operate. A concentrated one doesn’t. You need to know who’s in the room before you decide whether to show up.

Which names does the sponsor actually need to restructure and which ones just need time. Most people are working on the first question. The second one is where the edge actually is.

Are there any recent examples of LME holdouts achieving a meaningful recovery? I’m not aware of any.

This sounds like the Caesar’s palace debacle written up in Caesar’s coup