Blue Owl Capital ($OWL): The Book Nobody Believes (Part 1)

Three businesses, one discount, and five debates that determine whether it's earned.

Private credit made one promise above everything else: we solved volatility.

No mark-to-market swings. No margin calls or forced selling. Just senior secured loans to PE-backed companies, locked up for years, generating steady income while public markets lost their minds.

Blue Owl told that story better than anyone.

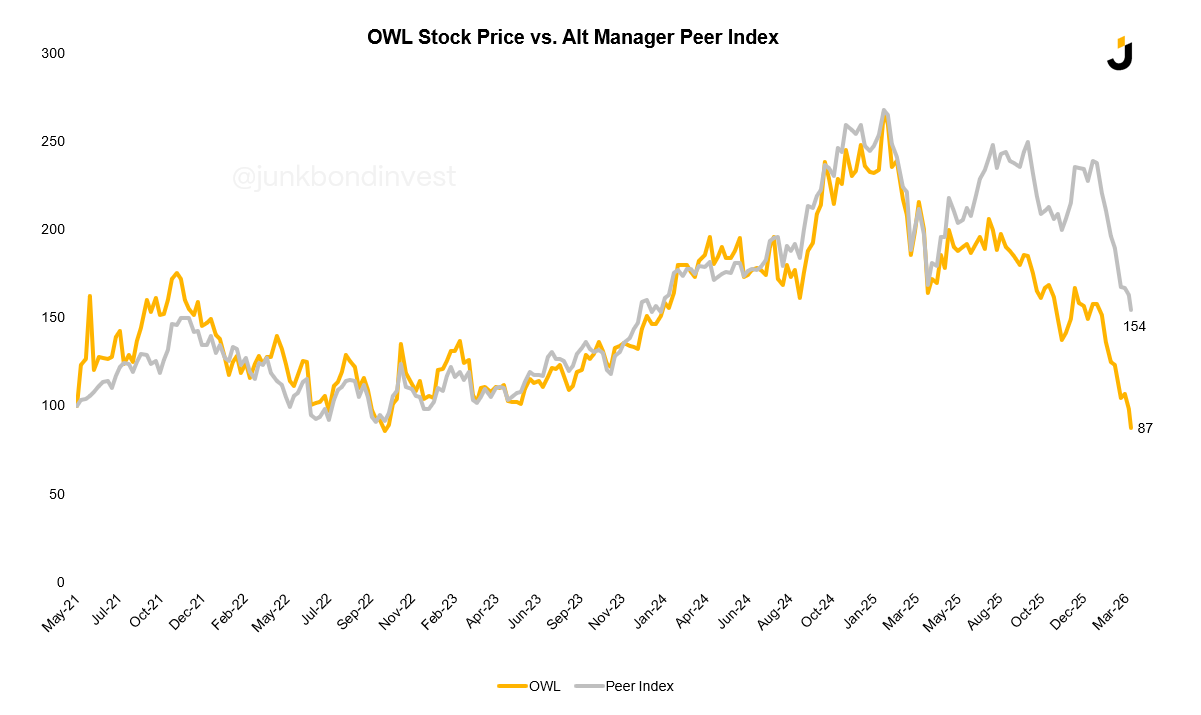

$307 billion in AUM. $42 billion raised in 2025 alone. A stock that nearly tripled off its IPO.

Then OBDC II halted redemptions. A proposed merger that would have forced retail investors to effectively absorb losses. Short interest exploded. The stock crashed 60% from its peak. And the question private credit has been dodging for a decade landed directly on Blue Owl: are the marks on these loans actually real?

The stock is now at $9.11. It trades at a ~60% discount to Blackstone, a 50% discount to Ares, and below the multiple the entire alt manager sector hit at its worst point during COVID.

Nobody in the peer group is cheaper. It isn’t even close.

The marks on the software portfolio are generous. The retail channel takes years to heal, not quarters. The dividend is being paid above earnings. Management is already running behind its own five-year targets after twelve months.

But Blue Owl is three businesses sharing a balance sheet and a stock price.

The credit franchise deserves every bit of skepticism it’s getting. What it doesn’t necessarily deserve is to drag down a GP Stakes business earning permanent fees from owning pieces of other asset managers, and a digital infrastructure operation leasing data centers to Meta, Microsoft, and Amazon on 15-year contracts.

Neither of those cares whether some software company in the loan book can service its debt.

Distrust doesn’t stay contained, though. When your largest business is under a cloud, it slows fundraising everywhere, compresses the multiple on everything, makes the whole harder to separate than the parts.

This is Part 1 of two. Here I discuss what Blue Owl actually is, and the five debates that determine whether the discount is earned. Part 2 does the math, stress-tests the multiple across three scenarios, and answers whether you should own it here.

Three Businesses, One Stock Price

Blue Owl is not one business. It is three, and the market is pricing all of them as if they share the same problem.

The first is credit. The second buys minority stakes in PE firms. The third owns data centers leased to the biggest technology companies in the world. Understanding why the discount may be too large, or too small, starts here. Here’s a quick summary:

Before getting into what is broken, it helps to understand how the machine works. Alt managers make money by charging fees on other people’s capital. The fee stream is the business. What separates the great firms from the average ones is permanence: capital that is locked up for years cannot be pulled in a bad quarter, which means the fee revenue is closer to an annuity than a subscription.

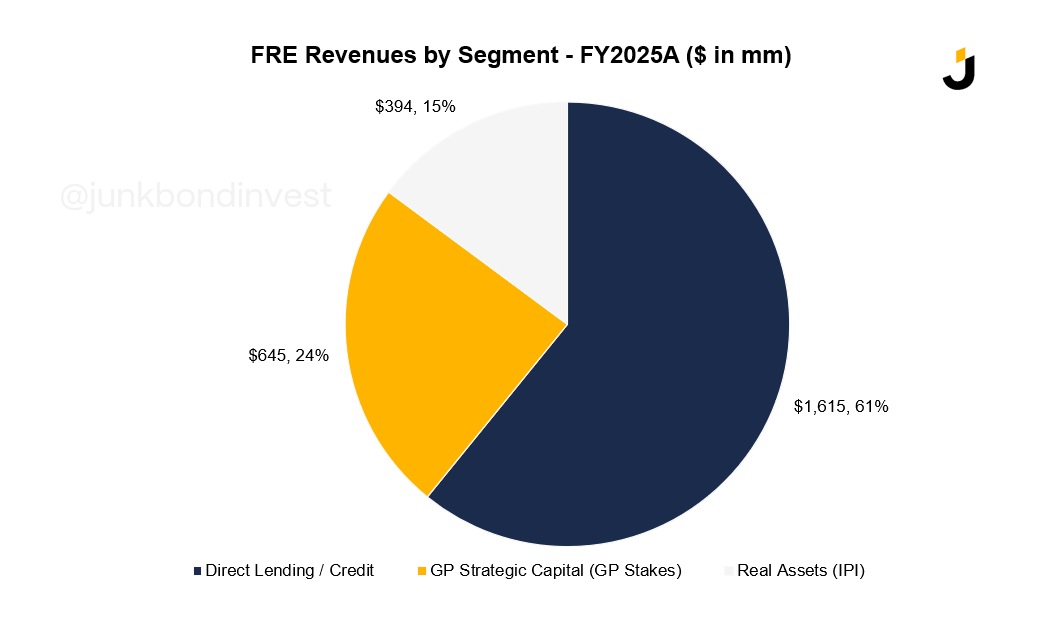

Blue Owl built its model around that principle. Roughly 95% of revenues come from recurring management fees, FRE margins run at ~58%, and at year-end 2025 FRE earnings were running at $1.5 billion annually. The current problem is concentrated in one of those three segments.

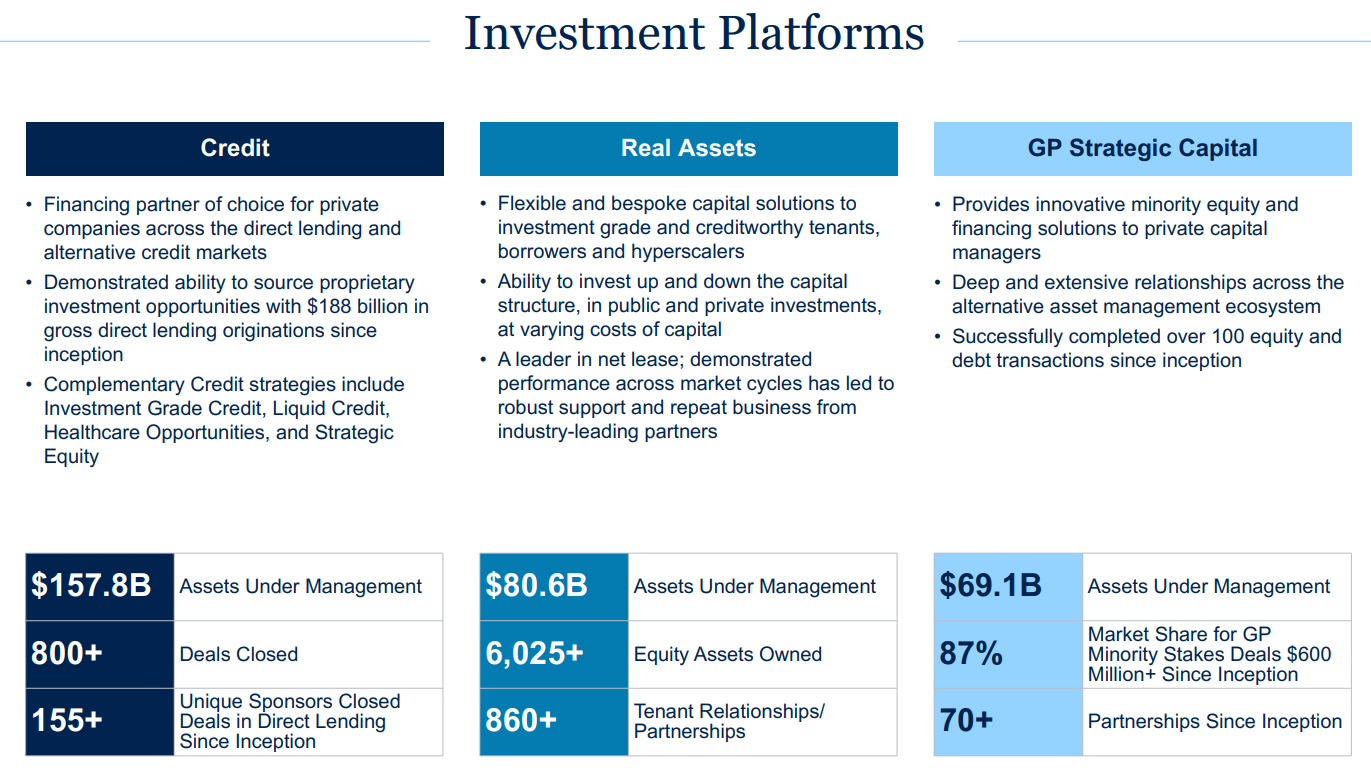

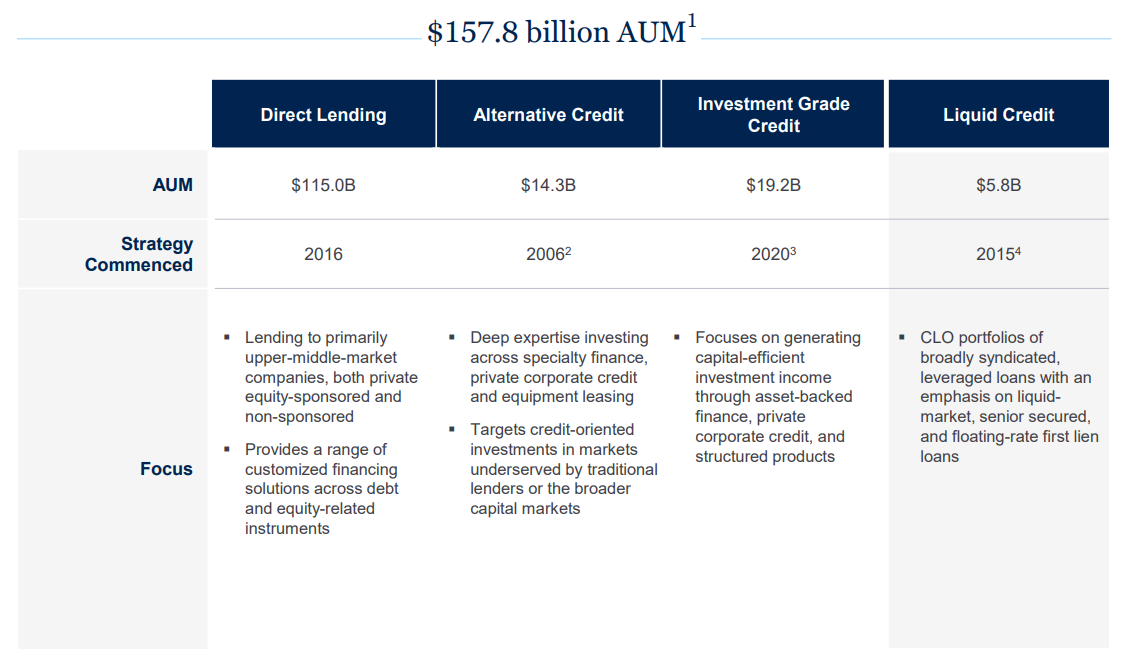

Direct Lending / Credit (~61% of FRE Revenues)

When a PE firm buys a company, it usually needs to borrow money to finance the deal. Historically that meant going to a bank, which would syndicate the loan to other investors. Blue Owl cuts out the middleman. It goes directly to the PE sponsor, offers to fund the entire loan itself, and charges a premium for the speed and certainty of execution that a single lender can provide.

The borrowers are PE-backed companies, mostly in software, technology, healthcare, and business services. The loans are first-lien senior secured, meaning Blue Owl sits at the top of the capital structure and gets paid before anyone else if something goes wrong.

The fee model charges ~1.5% per year on the total assets it manages, regardless of performance. That fee is collected from four separate vehicles. OBDC and OTF are publicly traded; anyone can buy or sell shares on a stock exchange, and the market prices them daily.

OCIC and OTIC are non-traded, sold exclusively through financial advisors to retail investors. There is no exchange. If an OCIC investor wants out, they submit a redemption request and the fund is only required to honor up to 5% of its total assets per quarter. That structure is the permanent capital mechanic: even under stress, the fee base drains slowly rather than all at once.

That same structure is precisely what created the current problem. OBDC II, a fifth vehicle that is now being wound down, replaced its quarterly redemption process with return-of-capital distributions funded by asset sales. Investors who wanted liquidity discovered the exit was smaller than they were led to believe.

The resulting overhang, combined with a surge in redemption requests at OTIC, means the credit fee base is being drawn down at a pace Blue Owl cannot control. Atalaya, acquired in 2024, adds a different flavor of credit: consumer loans, equipment leases, and specialty finance with shorter duration and hard collateral rather than corporate debt.

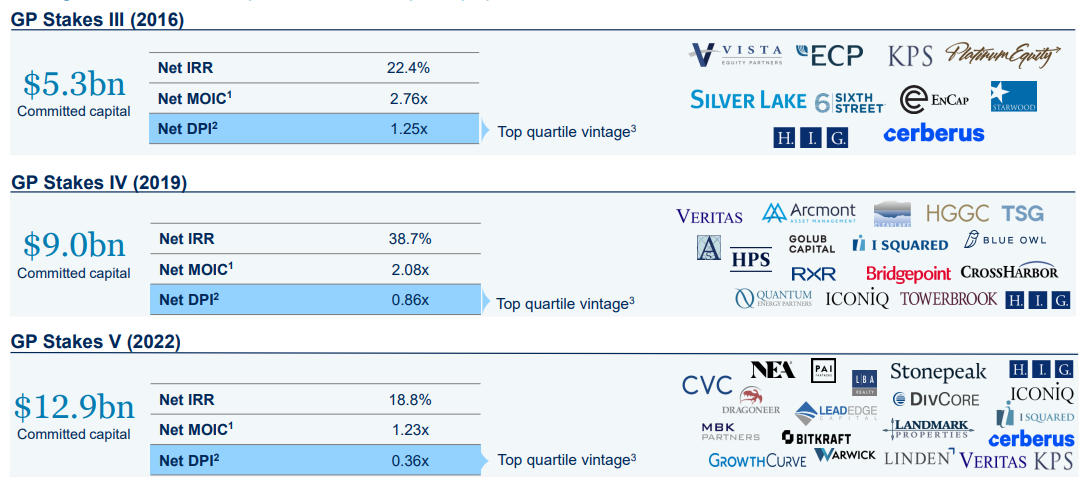

GP Strategic Capital (~24% of FRE)

This business has nothing to do with lending. Blue Owl buys small minority stakes, typically 10-15%, in private equity management companies themselves. Not their funds. The firm. The entity that earns management fees and carried interest in perpetuity, regardless of which fund it is currently raising.

Think of it this way: if you owned 10% of KKR’s fee-earning engine, you would collect a share of every management fee KKR charges on every fund it ever runs. That is the GP Stakes model. The PE firm gets liquidity and a strategic partner. Blue Owl gets a permanent, compounding revenue stream with no credit exposure, no mark-to-market risk, and no connection to what is happening in the BDC market.

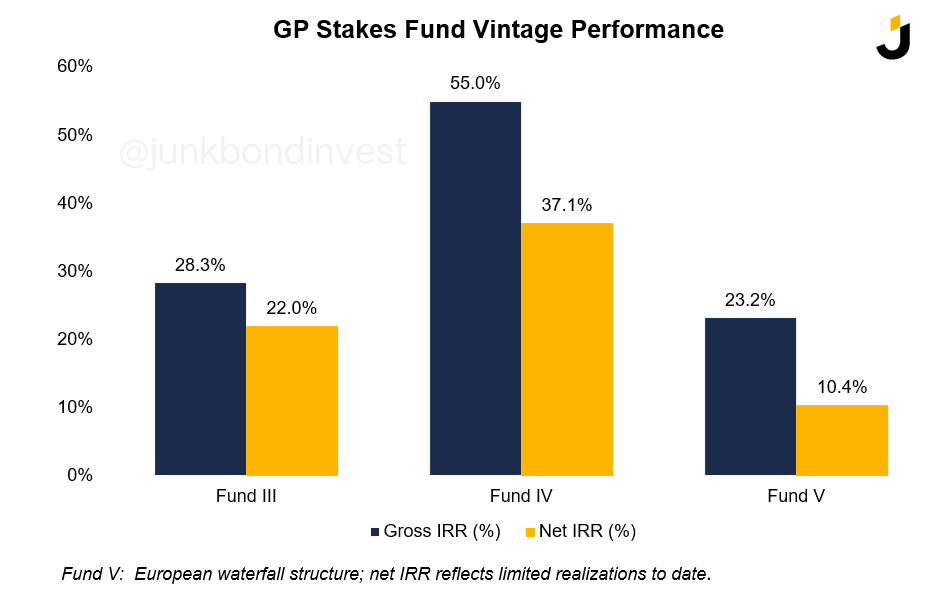

The portfolio spans roughly 40 managers across five fund vintages, including Clearlake, Stonepeak, Veritas, and KPS. The track record is real: HPS was acquired by BlackRock in late 2024 at a significant premium, and CVC and Bridgepoint are publicly traded comps.

Fund VI is the current fundraise, targeting $13 billion. Existing fee streams are unaffected by whether it closes on time. What is at stake is whether the fee base grows.

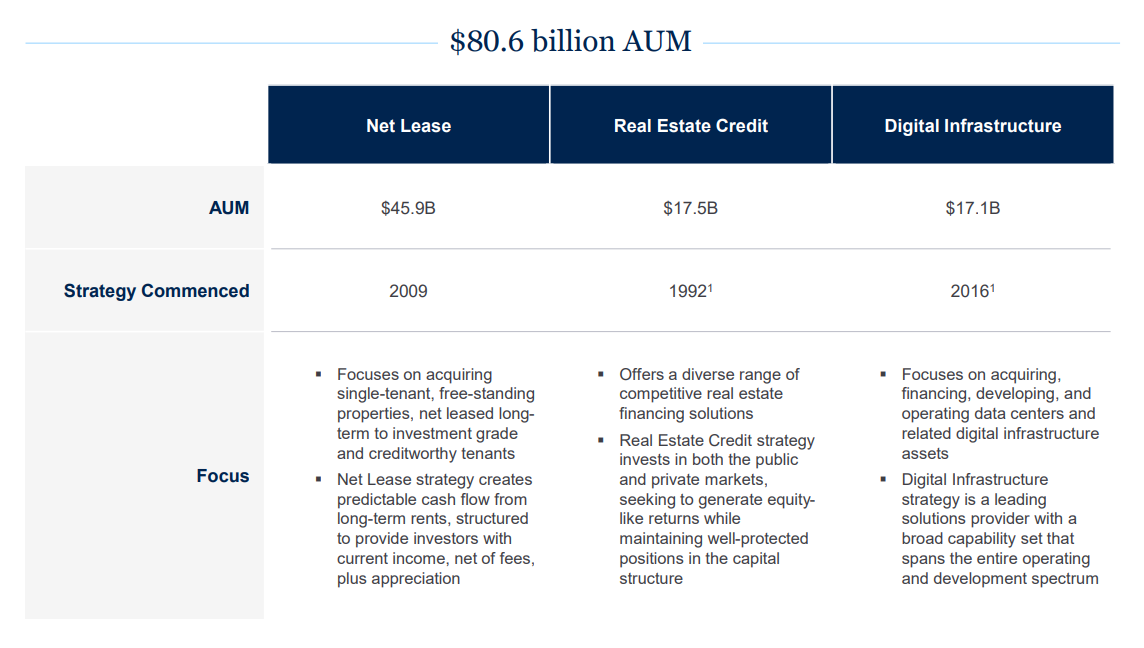

Real Assets / IPI (~15% of FRE)

The Real Assets segment spans net lease, real estate credit, and digital infrastructure, with $80.6 billion in AUM across the three strategies. The piece most relevant to the current debate is IPI Partners, the digital infrastructure business acquired in January 2025.

IPI Partners builds and owns data centers, then leases them to hyperscalers on long-term contracts. The tenants are Meta, Oracle, Microsoft, and Amazon. The leases run 15 years with financial penalties for early exit.

The confusion in the market stems from headlines about data center financing stress in early 2026. Those stories were about speculative AI compute companies borrowing in public debt markets. Blue Owl’s counterparties are IG hyperscalers who have already committed to the capex and need the physical infrastructure to execute it.

Five Debates, One Question: Is the Discount Earned?

The first three debates are about deterioration already underway in credit. The last two are about whether the rest of the platform can grow through it.