Super Micro's ($SMCI) Busted Converts: What the 11% Yield Is Not Telling You

A special situation credit analysis of SMCI's convertible bond stack

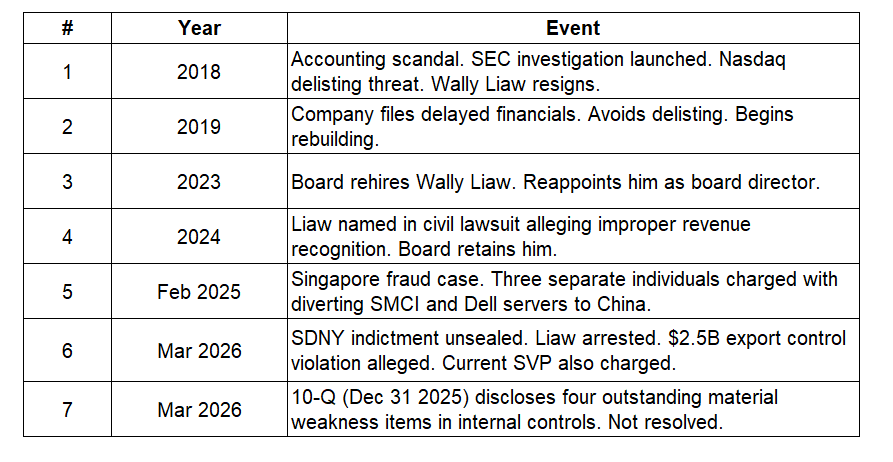

In 2023, Super Micro Computer’s board made a decision.

Revenue was growing triple digits. The stock was near all-time highs. The board looked at all of that and decided to rehire Wally Liaw, the co-founder they had pushed out 5 years earlier after an SEC accounting investigation, and put him back on as a director. With full knowledge of the 2018 history. Nobody forgot. They just decided it didn’t matter anymore.

Three years later Liaw was indicted by the SDNY.

On March 19th, federal prosecutors unsealed charges against Liaw and two others. The alleged scheme: conspiring to divert $2.5 billion in Nvidia-equipped servers to China through falsified documentation. To defeat auditors (allegedly), serial numbers were physically removed from the hardware and reaffixed using a hair dryer. SMCI was not named as a corporate defendant.

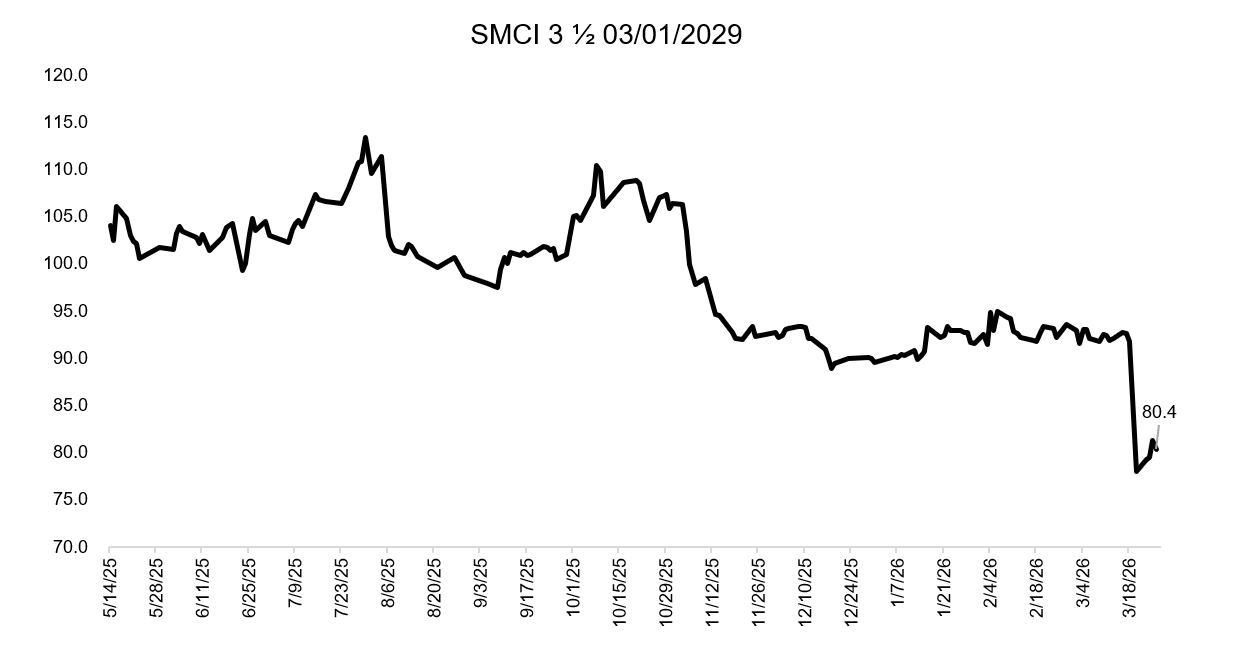

The stock fell 33% overnight. The converts dropped 10 to 20 points. The 2028s now trade at 87 cents, the 2029s at 81, the 2030 zero coupon at 73. The 2029s yield ~11% on a company carrying over $4 billion of cash, $10 billion of inventory, and net leverage of ~0.5x. On those numbers, the bonds look like an opportunity, right?

It’s not so obvious. This is the 5th governance episode in 8 years at a company that has consistently looked at its own history and decided it did not apply anymore. The balance sheet is real, sure. The question is what is standing behind it.

Not the First Time

To understand why this indictment is different from a typical governance shock, you need to know what came before it.

In 2018, the SEC charged SMCI 0.00%↑ with widespread accounting violations, including premature revenue recognition and improperly reduced accrued liabilities. Wally Liaw resigned under pressure. The stock spent two years in the penalty box before the AI server cycle rescued it. In 2020, the SEC charges were settled.

In 2024, Hindenburg accused SMCI of channel stuffing. SMCI’s own filings disclosed family-linked entities tied to CEO Charles Liang accounting for 4.3% of cost of sales. A civil lawsuit named Liaw for improper revenue recognition.

In October, E&Y resigned as auditor, stating it could no longer rely on management’s or the Audit Committee’s representations. Three months before the current indictment, SMCI’s 10-Q disclosed four outstanding material weakness items in internal controls. Not historical. Outstanding.

A company with a governance incident you can underwrite: model the liability, estimate the fine, apply a discount, and move on.

What the evidence describes is an institution that tolerates escalating misconduct, and that distinction matters because the legal liability becomes harder to bound, supplier relationships harder to underwrite, and regulators who feel misled tend to look harder at what they missed.

The Balance Sheet

On the surface the balance sheet looks fine. SMCI has approximately $4.9 billion of total debt against $4.1 billion of cash, leaving net debt of roughly $800 million. The revolving credit facilities, $2 billion from JP Morgan and $1.8 billion from CTBC, are entirely undrawn. Net leverage sits at ~0.5x. By any conventional measure this looks like a company with options.