Credit Weekly: The Terminal Value Problem

Software, Spreads, and the Question Nobody Can Answer

🚨 Connect: Twitter | Instagram | Reddit | YouTube | Job Board

Here’s a question nobody in leveraged finance can answer right now:

What is a software company worth in five years?

Not what it earns today or next quarter. Not what the sponsor paid for the business. What it’s actually worth when the AI labs are telling their investors they plan to replace Salesforce, Workday, and Adobe. When Google is doubling model performance every three months. When the capability curve is moving faster than any corporate strategy team can respond to.

Nobody can answer that question. Nobody.

If you can’t answer that question, you can’t underwrite a refinancing at par for a mediocre software company with a 2027 maturity. And if you can’t underwrite the refi, the loan shouldn’t trade at 95. It should trade where the amend-and-extend math takes you, which is somewhere considerably lower and considerably uglier.

That uncertainty is now the defining feature of the credit market. Not spreads. Not rates. Not whatever’s happening with Iran. The inability to assign a terminal value to a huge slice of the credit universe. In the public markets, the repricing has already started. In private credit, nobody wants to say it out loud because the moment you do, the marks have to move.

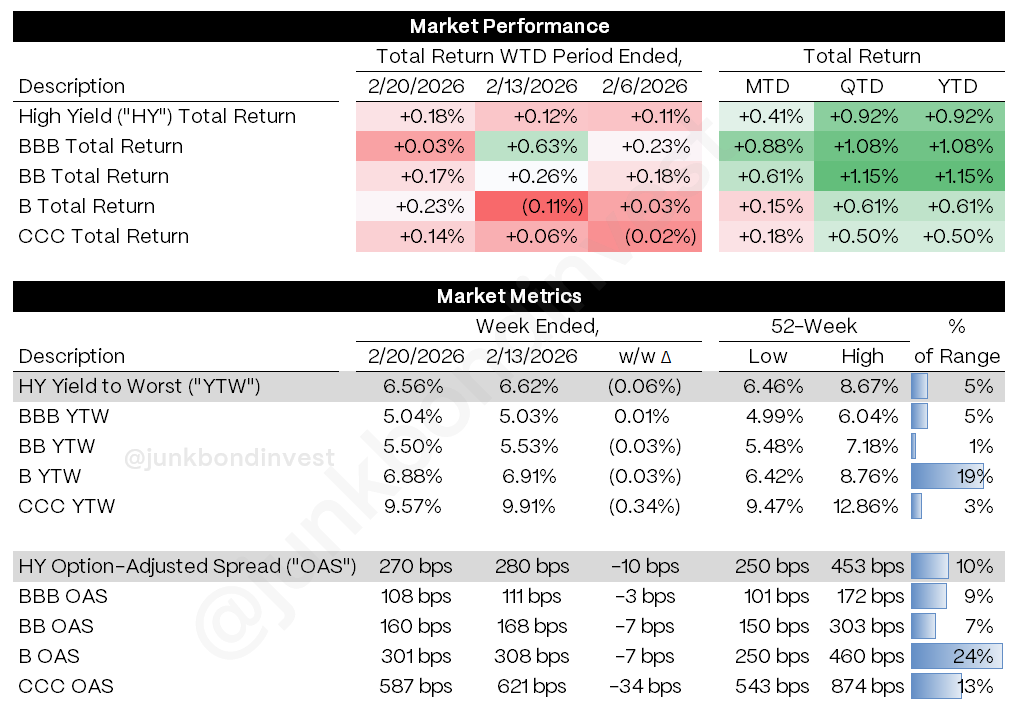

This is all creating a dispersion regime that the index-level data completely obscures. Over the past month, the HY index has ground tighter week after week. Looks calm. But underneath, the leadership has been rotating violently. The index averages all of it into a number that looks stable while the components are tearing apart.

The SaaSpocalypse: Not What You Think It Is

AI capabilities are compounding on a monthly cadence. Google released Gemini 3.1 Pro last week with double the reasoning performance of the version it launched three months ago. OpenAI is burning cash at unprecedented rates. Anthropic is launching enterprise agent products. The competitive intensity among these labs is accelerating faster than any single software company can adapt.

And they’re not being coy about who they’re coming for.

The Information reported that during a recent investor presentation, OpenAI leadership told investors they expect their future products and agents to replace software from Salesforce, Workday, Adobe, Slack, and Atlassian. This came alongside updated financial forecasts showing OpenAI expects revenue to hit $30 billion this year and $62 billion next year, with $25 billion of cash burn in 2026 alone. They’re not messing around.

Every credit investor holding paper in the enterprise software stack should be paying attention to that.

Remember when Steve Jobs went on stage and said the iPhone would replace your phone, your iPod, and your internet communicator? Nokia and BlackBerry were still printing record revenues that quarter. Didn’t matter. The terminal value of those businesses dropped sharply within five years. You just couldn’t see it in the earnings yet.

For a B-rated enterprise software company with $500 million of ARR and 5x leverage, the near-term is probably fine. Customers still paying. Contracts still renewing. But the willingness to renew at current pricing starts eroding as AI alternatives improve. That compresses net revenue retention. Compresses growth expectations. Makes the leverage ratio look worse on an enterprise value basis even if EBITDA hasn’t moved yet.

The relevant question isn’t “will this company default in the next 12 months?” but “will anyone underwrite the refinancing at par when the maturity comes due?”

For a growing number of names, the answer is no.

The data backs it up. A record $25 billion of US software loans slid into distress in January. But look at Europe. Almost nothing. Just 3.6% of European institutional loans maturing before 2027 are software-related, compared to 17.3% in the US.

That divergence tells you this isn’t purely an AI story. It’s also a leverage story.

US sponsors loaded 7-8x leverage onto subscription revenue streams they told lenders were “recurring and predictable.” European deals were smaller. More conservative. When sentiment shifts, the US book has zero margin for error while Europe shrugs.

AI just revealed that leverage was always too high.

Think about it: 8x leverage on a SaaS business was always insane. The only thing propping it up was the assumption that the subscription stream would last forever and switching costs were permanent. That net revenue retention above 110% was a law of nature rather than a cyclical artifact of a market with no real alternatives.

Assumptions like that die slow. Then they die all at once.

You know what’s telling? Several sponsor-backed software firms released earnings ahead of schedule last week. Voluntarily. To calm lender nerves. Historically secretive companies proactively opening their books.

Two years ago a sponsor would have told its lender group to pound sand if they asked for interim financials early. Now they’re disclosing because they’re scared of what happens if they don’t.

For the first time in this cycle, lenders have leverage over borrowers. That shift is real, even if it’s probably temporary.

The Software Maturity Wall: Extension Risk Is the Real Risk

So if software companies aren’t going to default en masse, what actually happens when all these loans come due?

The concentration of software loans maturing in 2026-2027, the largest sector cohort in the near-term maturity bracket, is overwhelmingly going to get resolved through amend-and-extend transactions, not through bankruptcy filings. When a borrower can’t refinance at par but isn’t in operational distress, the playbook is familiar: the sponsor and the existing lender group negotiate an extension. Lenders get a fee, a spread bump, maybe some incremental covenant protection. The company gets two or three more years of runway. No default. No restructuring. Everyone claims victory.

But this has implications for loan investors that aren’t being processed. If you own a software term loan trading at 85 with an 18-month maturity and you’re calculating a 12-15% YTM, you’re pricing in a par repayment at maturity. That par repayment likely isn’t coming. What’s coming is an extension where your actual return is the coupon plus a modest fee, not the coupon plus 15 points of pull-to-par. The realized return is going to be something like 8-10%.

And here’s the part that should keep loan investors up at night: the amend-and-extend process is where creditors get coerced, and in this market, they will be. Sponsors know that a fragmented lender base facing a maturity wall has limited options. You can either extend on the sponsor’s terms, which often means PIK toggles, covenant stripping, and priming risk from new money tranches, or you can watch the loan trade down as the maturity approaches without a resolution.

Each extension that adds PIK, strips covenants, or pushes maturities without meaningful deleveraging is a slow-motion impairment that never shows up in the default statistics. The risk isn’t default but extension at terms that are incrementally worse for lenders while the TEV question remains unresolved.

The Fed, the Calendar, and the Noise

None of this exists in a vacuum. The macro backdrop is making everything worse.

Start with the Fed. The January minutes were more hawkish than the market wanted to hear. The Committee held at 3.50-3.75%, but several participants raised the possibility of rate increases if inflation stays elevated. The market is still pricing one or two cuts later this year. Maybe they’re right. But the way I read these minutes, the bar for resuming cuts is a lot higher than most people think.

Think about what this means for leveraged loan borrowers.

The entire floating-rate pitch for two years has been: “rates are coming down, so your all-in borrowing cost will decline, and that supports credit quality.”

That thesis is evaporating.

A lot of these LBO models were underwritten assuming SOFR at 3% by now. Every quarter that gap stays wide is another quarter of cash flow getting eaten by debt service instead of building equity cushion.

Then there’s the tariff ruling, which is a bigger deal for credit markets than the initial reaction suggested. The Supreme Court struck down the IEEPA-based tariffs on Friday, and while the equity market shrugged, the downstream implications for rates and fiscal are significant. The ruling potentially creates $150-200 billion in rebate liability as duties collected under the invalidated authority get unwound. That money has to come from somewhere and likely means the fiscal deficit widens.

For credit investors, this is a rates story. More deficit means more Treasury supply. More Treasury supply means upward pressure on the long end. And if you’re holding fixed-rate HY bonds at yields near 52-week lows, a repricing in Treasuries hits your total return hard even if credit spreads don’t move at all. BBs are the most exposed here. They have the most duration and the least spread cushion in the HY complex.

Then there’s the calendar. Early March, historically the worst month for HY spreads. Every year the market finds a reason to reprice around this time (remember COVID)? Dealer positioning is at local lows but that light positioning could mean seasonal weakness is priced. Or it could mean there’s no natural buyer when vol arrives.

I’d lean toward the latter. But consensus expectation for March weakness is widespread enough that a squeeze higher isn’t impossible.

Last but not least, geopolitics. Oil near six-month highs. Significant US military presence in the Middle East. Hard deadline on Iran nuclear talks. It sounds serious, and it might be.

But markets have a long track record of absorbing geopolitical shocks within 48-72 hours. Base case is either a deal or a limited strike that avoids oil infrastructure, with crude settling lower by year-end on surplus supply fundamentals. Unless there’s actual disruption to physical flows through the Strait of Hormuz, this is a vol event, not a credit event. Worth watching. Not worth repositioning around.

The Primary Market Is Open (If You’re High Quality)

Against that backdrop, the new issue market continues to function. But in an increasingly bifurcated way.

Roughly $4 billion of high yield priced last week, down from nearly $11 billion prior. February issuance of $20 billion already cleared last February’s full-month total. But composition matters more than volume.

Over half of February’s deals came from the BB bucket. These issuers aren’t borrowing to grow. They’re borrowing to manage existing capital structures. Window’s open for higher-quality names. Increasingly selective for anything below the BB line.

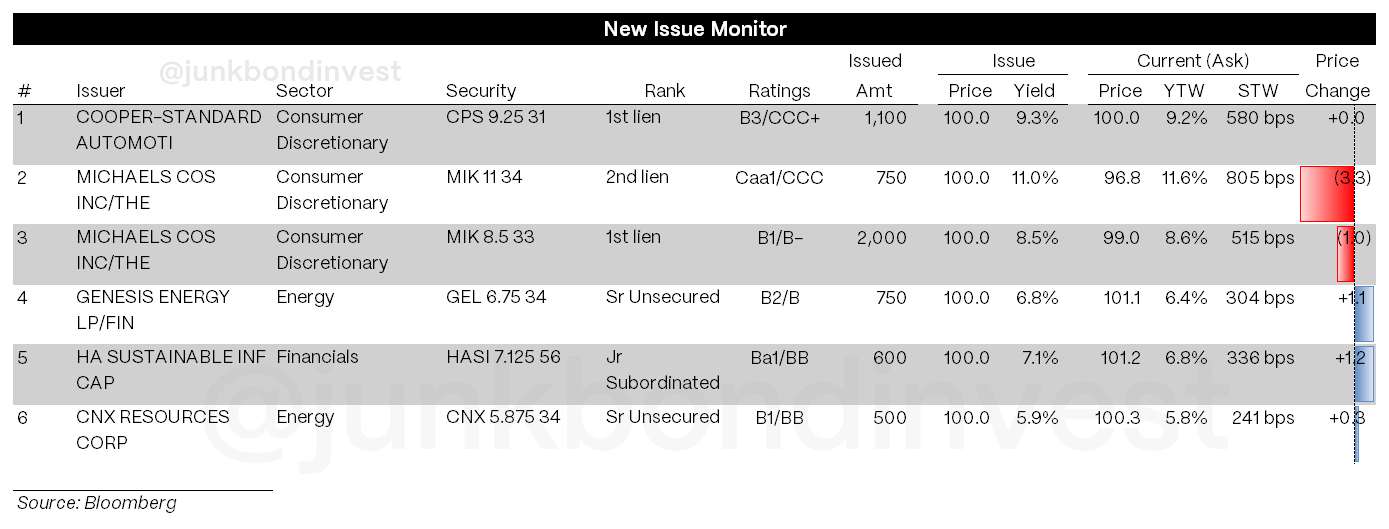

The Michaels Companies deal tells you everything you need to know about where the market draws the line.

Apollo’s arts and crafts retailer came with a $2.75 billion dual-tranche secured bond offering to refinance 2021 buyout paper. The $2 billion first-lien notes were upsized by $1.25 billion from initial guidance, priced at 8.50% after drawing over $4 billion of orders. Strong.

But the second-lien notes? Different story. Cut by $200 million to $750 million. Launched at 11%. Price talk unchanged from initial talk. The accompanying term loan also saw $100 million shift into the first-lien notes.

Money wants to be senior. Money wants to be secured. Anything below that is a harder sell than six months ago.

In energy, the contrast couldn’t be sharper. CNX Resources priced $500 million of eight-year senior notes at 5.875%, tight end of guidance, to fund a tender for its 6% 2029s. Genesis Energy upsized its eight-year offering to $750 million from $500 million at 6.75% after a Moody’s upgrade. Bonds traded up the next day.

No drama. Improving credits accessing capital at tighter levels.

That’s what a healthy primary market looks like. It just happens to exist alongside an unhealthy one.

Two primary markets, running in parallel. One functioning beautifully. The other seizing up. Same Bloomberg screen. Completely different realities depending on which side of the quality divide you’re sitting on.

Private Credit: Blue Owl and the Trust Problem

Blue Owl was in the spotlight again this week, and not in the way any asset manager wants to be.

The firm sold a $1.4 billion portfolio of loans from its Blue Owl Capital Corp II fund at 99.7 cents on the dollar. Management called the sale “an extremely strong statement.” The marks are real, they said. The demand is there.

Let’s look at who was actually buying. Three North American pension funds and Kuvare, Blue Owl’s own insurance asset management affiliate. When one of the buyers in your “arm’s length” transaction is your own affiliated entity, questions about genuine price discovery aren’t cynical. The pension funds provide some independent validation, but Kuvare’s involvement means Blue Owl was on both sides of this trade. I wouldn’t call that a “market-clearing” price.

And remember why this sale happened in the first place. Capital Corp II was hit with a wave of redemptions last year. The original plan to return capital by merging the fund into a publicly traded vehicle was scrapped after investors balked at the losses they’d take. This wasn’t a portfolio sale from a position of strength. It was a liquidity solution for a fund under pressure, executed through channels the manager controls. Meanwhile, Blue Owl collects management fees on the assets regardless of which vehicle they sit in. The assets move. The fees don’t.

The public market isn’t buying it. The publicly traded BDC trades at roughly 77 cents on the dollar in terms of price-to-NAV. Boaz Weinstein is offering to buy BDC shares at 65-80 cents on NAV.

If the underlying loans are truly worth 99.7 cents, the wrappers around those loans shouldn’t be trading at 20%+ discounts. That gap tells you the market doesn’t trust the marks. Period.

Make sure to read the BDC primers I published (parts 1, 2, and 3). I’ll be doing a thorough review of OBDC 0.00%↑ over the next couple of weeks. Keep an eye out for that.

Where the Opportunities Are, Stripped of Narrative

So where does all of this leave you if you’re trying to actually put money to work?