The BDC Primer (Part 3)

BDC debt for the fixed income investor, and what equity holders should know about the liability stack

Parts 1 and 2 were about the assets.

This one is about how the whole thing can blow up.

BDCs borrow money to lend money. That’s the business. And when you’re a levered vehicle investing in below-investment grade loans, how you fund yourself matters as much as what you own.

Maybe more.

The equity investors obsessing over NAV and dividend coverage are looking at the right numbers in the wrong order. The liability stack tells you what happens under stress. Whether management is forced to sell assets at the worst possible time. Whether the dividend gets cut before the portfolio even goes bad. Whether a ratings downgrade turns a contained problem into a full-blown crisis.

Roughly $60-70 billion of BDC unsecured bonds sit inside IG portfolios right now. Rated BBB-, backed by loans that would be rated B or B- on their own. The math works until it doesn’t.

And right now some of it isn’t working. TCPC 0.00%↑ just got downgraded to high yield. FSK 0.00%↑ and OCSL 0.00%↑ are on negative watch. A maturity wall is coming due at higher rates than the paper it’s replacing.

The bond market already knows this. Spreads are widening. The question is whether equity investors are paying attention.

They should be.

What’s inside:

Why BDC debt exists and who’s buying it

The liability stack: secured revolvers vs. unsecured notes vs. SBIC debentures

Asset coverage requirements and what happens when they bite

How to read a BDC’s funding profile

The 2026 maturity wall and refinancing math

Spread framework and relative value

Fallen angel risk: what happens when a BDC loses investment grade

What equity investors should take from this

I. Why BDC Debt?

BDCs need leverage to generate competitive returns. The math is straightforward.

A portfolio yielding 10-11% on assets doesn’t get you to a double-digit ROE without debt. At 1.0x leverage, a BDC earning 10.5% on assets and paying 5.5% on debt generates roughly 15.5% on gross assets, minus fees and expenses, leaving 10-11% ROE. Without leverage, you’re stuck at single-digit returns that aren’t as appealing.

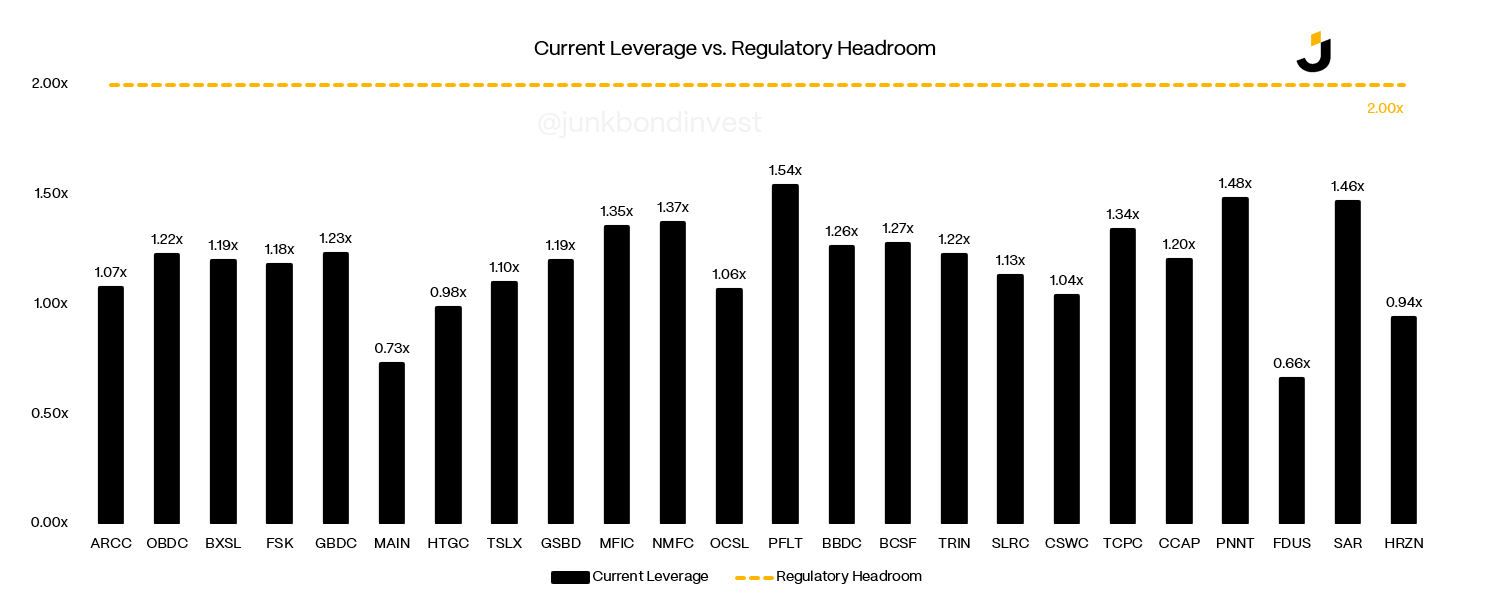

The regulatory cap is 2.0x debt-to-equity (raised from 1.0x by the Small Business Credit Availability Act in 2018). Most BDCs operate in the 0.9x to 1.2x range as prudent risk management. The average across the sector is currently around 1.2x regulatory leverage.

Most debt comes from three main sources: secured bank credit facilities, unsecured bonds, and SBIC debentures. Each has different characteristics, different costs, and different implications for stress tolerance.

For fixed income investors, BDC unsecured notes offer a few things:

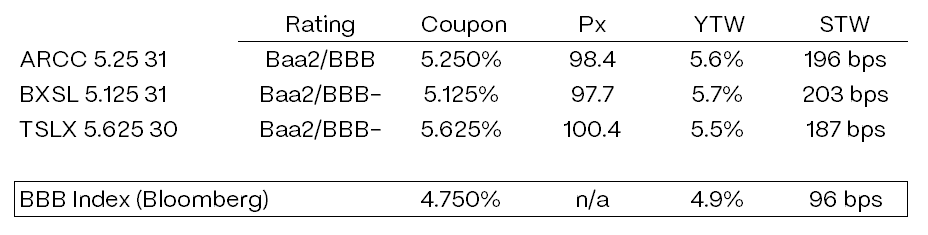

Yield pickup. BDC bonds typically trade wider than comparably rated financials. The highest-quality issuers like ARCC, BXSL, and TSLX trade tighter, in the 180-200bps range over treasuries. Smaller or weaker credits trade wider, sometimes 250bps+. The sector carries a complexity premium and a private credit stigma that keeps some institutional buyers away.

Structural seniority over equity. Unsecured bonds sit above equity, but below the secured facilities. The relevant question for bondholders is less about ultimate recovery and more about whether the structure forces deleveraging before the cycle turns. In stress, the first thing that bites is asset coverage and borrowing base mechanics, not ultimate recovery math. Bondholders can be “covered” on paper while equity gets obliterated through forced deleveraging, dividend cuts, and NAV writedowns.

Diversification. BDC credit risk is tied to middle-market corporate health, not mortgage credit or consumer lending. The underlying exposure is to PE-backed middle-market borrowers across sectors like software, healthcare, and business services, with software often a top concentration depending on how you classify the loans.

The catch: BDCs are essentially levered portfolios of below-investment-grade loans. The underlying assets are non-investment grade even if the BDC itself carries a BBB- rating. A BDC rated BBB- is holding loans that would individually be rated B. That mismatch is what makes BDC credit analysis interesting, and why spreads are wider than typical IG financials. And because marks are quarterly, spreads often move before NAV does.

Who’s buying BDC bonds?

The buyer base skews toward:

Insurance companies seeking yield pickup over core IG

Total return bond funds with flexibility to own BBB- credits

Credit-focused hedge funds playing relative value

Passive ownership is lighter than in vanilla IG financials because BDCs sit in an idiosyncratic corner of “financials” with various index and mandate constraints. The buyer base is more specialized, which contributes to wider spreads and more volatility in risk-off environments.

II. The Liability Stack

Not all BDC debt is created equal. Understanding the stack is the first step to credit analysis.

Secured credit facilities (revolvers and term loans)

Most BDCs have a secured revolving credit facility with a syndicate of banks. The facility is secured by the BDC’s loan portfolio, with the banks taking a first-priority lien on the assets. Think of it as a margin loan against the portfolio.

Secured debt is typically the cheapest funding source. But it comes with borrowing base risk: banks set an advance rate against eligible collateral (typically 50-70%), and if marks decline or assets move to non-accrual, the borrowing base shrinks. The BDC may be forced to pay down the facility even if it has ample liquidity otherwise.

Example: A BDC with $1 billion of collateral at a 60% advance rate has $600 million of borrowing capacity. If marks decline 10% and some loans move to non-accrual, the eligible collateral might drop to $850 million. Suddenly the borrowing base is $510 million. If the BDC had $580 million drawn, it needs to pay down $70 million or pledge additional collateral.

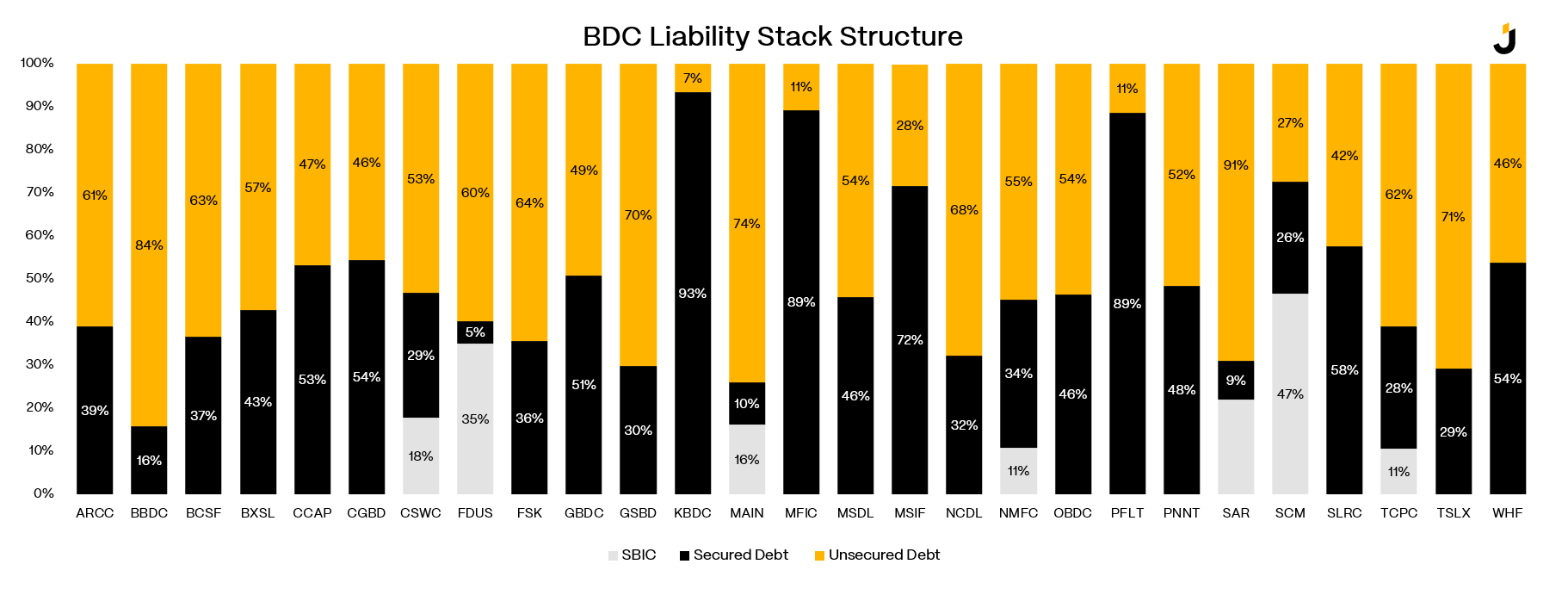

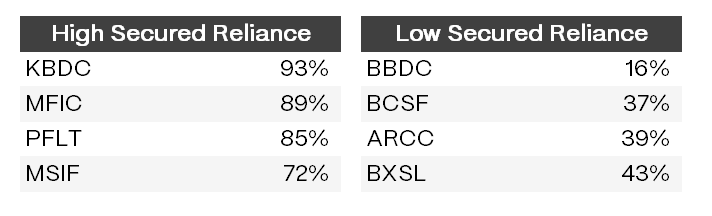

Across the sector, the secured/unsecured mix varies widely by issuer, but dispersion is enormous:

Unsecured notes

Unsecured bonds are typically 5-7 year fixed-rate notes issued in the institutional market. No borrowing base. No mark-to-market triggers. No margin calls. The debt just sits there until maturity (or early redemption).

That stability comes at a cost: unsecured notes price wider because bondholders are structurally subordinate to the secured lenders. In a liquidation, secured creditors get paid first from the pledged collateral. Unsecured bondholders have a claim on what’s left.

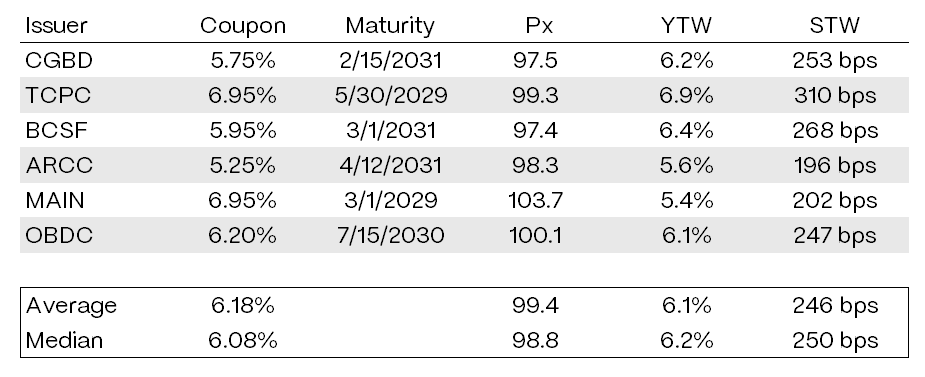

Current unsecured bond pricing (representative issues):

Note the dispersion. ARCC funds at +196bps. TCPC (now high yield) funds at +310bps. That’s over 100bps of spread difference that flows straight through to the income statement.

The BDCs with more unsecured funding have more flexibility. They’re not facing borrowing base pressure when marks decline. That’s worth something in a stress scenario.

SBIC debentures

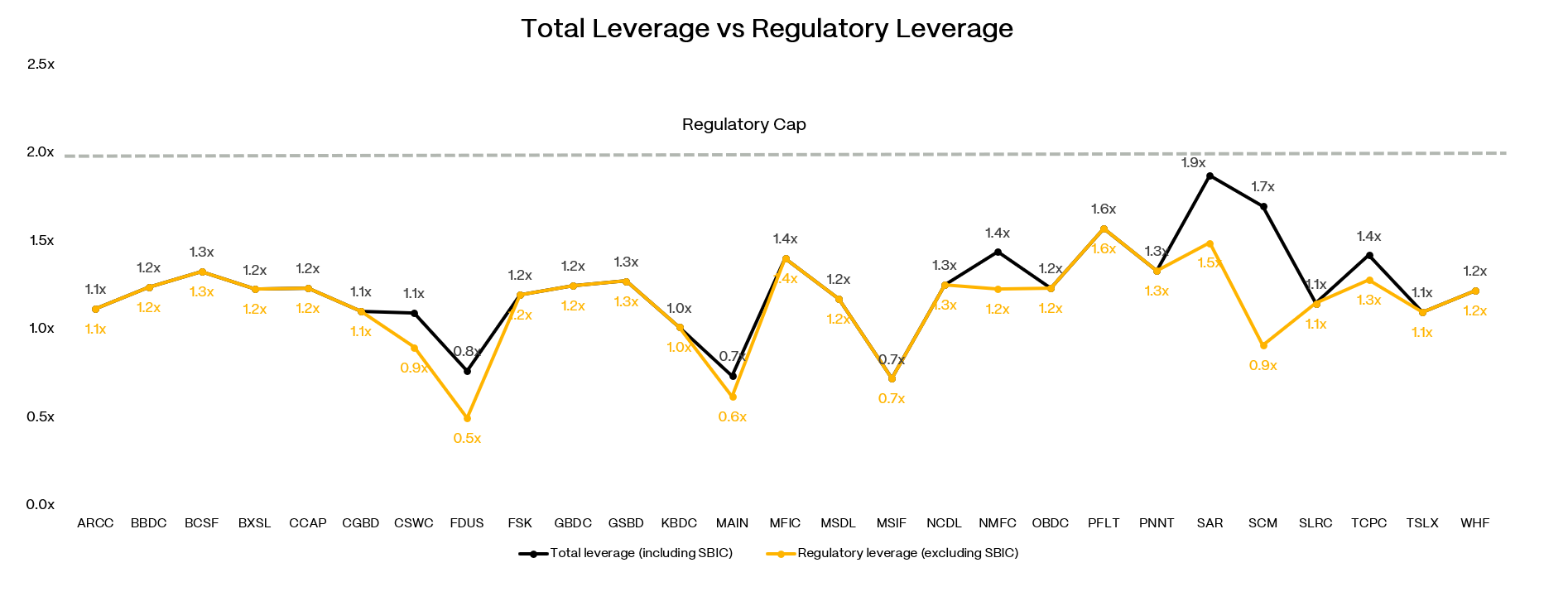

Some BDCs have Small Business Investment Company (SBIC) subsidiaries that can borrow from the SBA at favorable rates. The key feature: SBIC debentures are typically excluded from the regulatory leverage calculation. A BDC can run 1.0x “regulatory” leverage and 1.2x “total” leverage if the difference is SBIC debt.

Look at MAIN: Total leverage is 0.73x, but regulatory leverage (excluding SBIC) is only 0.62x. Or FDUS: Total leverage 0.75x, regulatory leverage 0.49x.

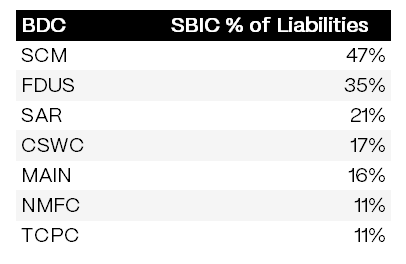

Which BDCs use SBIC meaningfully?

For the BDCs that have it, SBIC funding is a meaningful advantage: cheap, long-dated, non-recourse to the parent, and doesn’t count against the regulatory cap.

Convertible notes

A handful of BDCs have convertible notes outstanding (e.g., GLAD has issued convertible notes). Treat converts as unsecured debt first. Conversion is optional and terms-driven, and only becomes a deleveraging path if the equity performs and the notes actually convert.

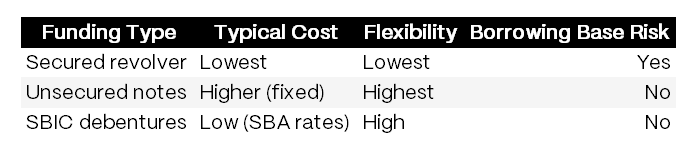

The liability stack framework:

Asset coverage, the tripwire

BDCs are subject to an asset coverage requirement under the 1940 Act. In practice, that can mean distribution restrictions and forced deleveraging, even if the portfolio is still “money-good” over time. In other words, if asset values fall, leverage mechanically rises, and at some point the BDC may stop paying distributions and delever (and/or issue equity) to get back into compliance.

The practical point: you don’t need “ultimate loss” to create stress. Marks down 5-10% plus a borrowing base haircut can force paydowns, dividend pressure, and defensive behavior long before any bondholder impairment is on the table.

III. How to Read a BDC’s Funding Profile

When you’re analyzing a BDC’s liabilities, here’s the framework: