Private Credit Unfiltered: Medallia is a Win for Direct Lending

Why taking the keys beats amend-and-extend when terminal value is gone

You’ve probably read 10 different Medallia takes by now. All largely the same.

Thoma Bravo eats five billion. Lenders take the keys. AI breaks software. Private credit can’t underwrite risk. Fine, we get it.

But the people writing about it have no idea what they’re looking at.

Medallia is actually a win for private credit. And that’s coming from me. Here’s what I mean.

Take the Keys Now

When a software borrower can’t refinance, the lender has two choices.

Amend and extend. Collect a fee. Push the maturity 18 to 24 months. Hope the AI question gets less scary or the business stabilizes. This is what most situations get.

Or take the keys. Cut the debt to a serviceable level, take the equity, run the business for cash.

A&E is rational when the business has terminal value. Borrower stabilizes, growth resumes, the credit refinances in 2029 or 2030.

When it doesn’t, A&E is just “kicking the can.” The interest is still going out the door. The business is still shrinking. The equity below you is impaired. You’ve delayed the inevitable for 2 years in exchange for an amendment fee that hits NII this quarter and a sponsor who’s playing for optionality with your principal.

You should always take the keys when terminal value is gone. Cut interest. Run the business for whatever cash flow it produces. Harvest the recurring revenue book until all the remaining customers churn. Distribute the cash up to LPs as the asset winds down.

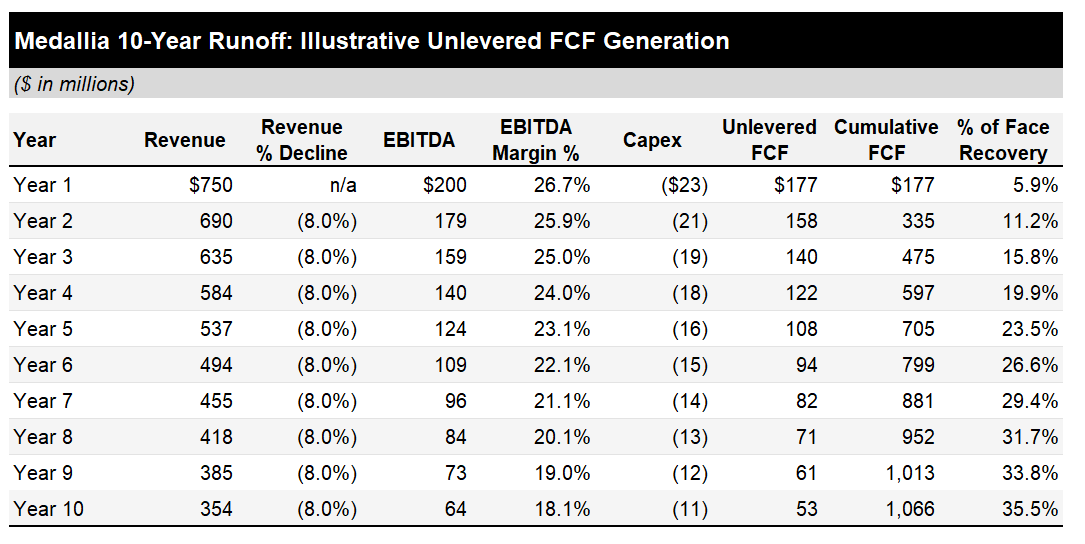

The runoff math at Medallia is directionally workable, even if it’s ugly. To be clear, what follows is illustrative. I have no real visibility into Medallia’s financials beyond the $200M EBITDA figure reported in the press. The numbers are meant to show order of magnitude, not precision.

Start with the $200M of EBITDA. Assume the business declines 8% a year as enterprise customers move to AI-native alternatives and Qualtrics continues taking share. EBITDA margin compresses 100 bps a year from operating deleverage. Capex at 3% of revenue. Cash taxes near zero with LBO NOLs.

Cumulative unlevered FCF over the 10-year hold: ~$1.0 billion. Plus residual sale value at year 10 on a $355M revenue business doing $64M of EBITDA, call it 3-4x trailing for $200-250M.

Nominal recovery on a $3 billion loan: $1.25-1.35 billion, or 40-45 cents.

The PV is a different number. Discount those cash flows at 10% and you’re looking closer to 25-30 cents on a present value basis, plus the discounted residual. Still real money. Better than zero. But the nominal recovery and the PV recovery aren’t the same thing, and anyone modeling this should run both.

A 5% revenue decline gets nominal recovery to 55-60 cents. 12% drops it to 30-35 cents. Margin compression assumptions move the answer further. The point is the order of magnitude. To be clear however, a 55-60 cent nominal loss on a workable runoff isn’t a defense of the investment.

The actual disaster on Medallia is the PE side. Thoma Bravo loses essentially all of the $5 billion of equity. PE economics need multiple expansion or EBITDA growth. You can’t run a SaaS business in managed decline when your LPs hired you to compound capital.

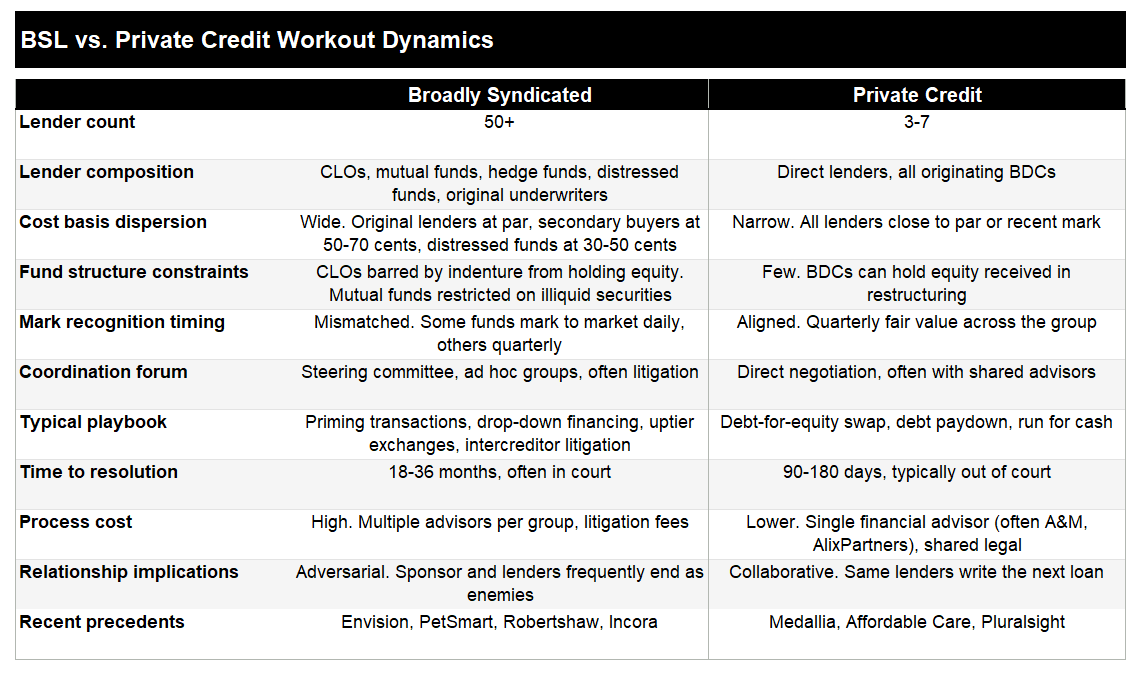

Why Private Credit Beats BSL Here

Picture the same loan in the syndicated market. $3 billion of debt, software business, 2021 vintage, AI disruption baked in. Run the workout.

50+ lenders. CLOs whose indentures don’t permit holding equity. Hedge funds who bought at 60 demanding fast equitization while the original lenders at par need to defer recognition because their fund mark depends on it. Distressed funds running the same creditor-on-creditor violence playbook they perfected in Envision and Serta. Everyone in the credit with a different cost basis, fund structure, and book to defend.

That coordination problem is why BSL software workouts in this cycle are probably going to recover 10-20 cents below the equivalent private credit outcome, all else being equal1. Not a function of weaker businesses. The lender group can’t act coherently. Slow value destruction through process.

Trey Parker at Sycamore Tree said something useful on the Credit Edge podcast last week. He flagged a slowdown in LME volume because sponsors are starting to figure out that creating enemies in the lender base has consequences when you need to come back to the same market two years later. Boomerang LMEs and repeat defaulters are the evidence that the BSL LME process doesn’t actually rehabilitate the borrower. We shall see if sponsors actually mean it.

The Medallia process looks nothing like that. Five lenders, give or take. Blackstone in the lead with KKR, Apollo, and Antares around it. Same vintage, similar fund vehicles, all carrying lofty marks until the recent moves. They hired A&M and started negotiating among themselves. Debt comes down. Equity goes to creditors. Business runs for cash.

No priming because the lenders are already first lien. No uptier because the lenders are aligned by structure rather than fighting each other for residual value.

Ninety days, outside of court, no litigation, with the same lenders who’ll be writing the next loan to the next sponsor next quarter.

This is where private credit pulls ahead, and it shows up exactly when the cycle turns. When everything is fine, BSL and private credit look interchangeable. When things break, BSL is litigation and value destruction. Private credit can be a quick handover. In theory.

The Business Was Already Broken

The AI narrative is doing too much work for people who don’t want to look closely at what actually happened.

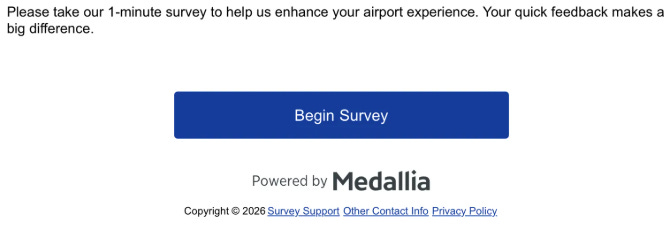

I actually caught Medallia in the wild last week. “Please take our 1-minute survey to help us enhance your airport experience.” Powered by Medallia. Begin Survey button.

I did not begin the survey. Nobody did.

This is the asset. $200 million of EBITDA. A survey button at a boarding gate that nobody presses. Terminal value already in question before AI showed up.

On top of that, Medallia’s interest expense shot up in 2022 when the Fed raised rates. Sales suffered from competition with Qualtrics, itself another PE-owned software business with its own debt issues.

Cap stack sized in 2021 for a 0% rate world and a growth path that didn’t materialize. Rates went up. Growth slowed. The interest burden ate the cash flow. AI is the accelerant. The fire was already lit.

Diameter’s Lewinsohn used the right framework on Bloomberg TV last week. Vulnerable software businesses are the “call the weather” phone services that died with the internet. He gave data visualization as his example. Customer feedback survey software fits the same description. The terminal value is in serious doubt before you start adjusting for the operating issues that already existed.

The Refi Window Is Shut

The BDC unsecured bond market was effectively closed for six weeks until PIMCO took down the entire Blue Owl deal at 270 over. That market is open again, at the BDC level, for the largest names and increasingly others.

The market for refinancing single-name software LBOs is not. New direct lending spreads are 100 bps wider than 18 months ago. Capital is flowing into opportunistic and special situations vehicles, not into refinancing 2021-vintage sponsor-owned software at the same multiples and terms that originally got them done.

Roughly 40% of software debt maturing in 2028-2029. Capital markets shut at the borrower level. The take-the-keys vs. A&E choice is going to play out hundreds of times over the next 24 months.

But not the same way every time. The market has finally started pricing dispersion within software. Software engineering loans are down 16 cents since January. Horizontal SaaS down 10. Cybersecurity barely moved. Vertical SaaS held up the best. 11 cents of spread between the best and worst software sub-sectors, where there was almost none three months ago.

The dispersion matters for what comes next. Not every software credit is headed to a take-the-keys outcome. Some are vertical SaaS businesses with sticky enterprise contracts, deep workflow integration, and limited AI substitution risk in the near term. Those might get refinanced or A&E’d through the maturity wall and maybe come out fine on the other side.

Others sit closer to Medallia. Horizontal tools that solve a generic problem AI can also solve. Customer feedback. Survey. Document automation. Basic analytics. Those credits don’t get to A&E their way out. The terminal value isn’t there to support the pretense.

The lender’s job over the next 24 months is figuring out which credit is which. The marks are starting to tell the story. The PIK insertion rate will tell more of it. By 2027 the dispersion will be obvious. Right now it’s still emerging, and the managers who get this triage right will own the next vintage.

PIK Was the Leading Indicator

Affordable Care is the other story to pay attention to. Blackstone and KKR are restructuring a $1.4 billion private credit loan made in 2021 for Harvest Partners’ buyout of the dental services platform. They marked it at 69.8 cents this quarter and moved it to non-accrual.

Read what Blackstone said about it. “We first marked down the loan 18 months ago and continue to be proactive in addressing underperformers.”

The mark moved 18 months ago. The non-accrual classification came this quarter.

Medallia tells the same thing on a faster timeline. 80 cents in December. 60 cents this month. Now non-accrual. Three quarters of mark deterioration before the official credit metric moved.

Credit deterioration in private credit runs through a long sequence. PIK toggle activation, covenant amendments, watchlist additions, fair value markdowns, non-accrual designation, restructuring, realized loss. The full sequence takes 18-36 months from first stress to final loss recognition.

ARCC 0.00%↑ just reported 1Q’26 non-accruals at 2.1% on amortized cost and noted the figure is “still below long-term averages.” That’s a backwards-looking statistic. Realized losses being reported in Q1 2026 are the resolution of credits that first stressed in 2023 and 2024, before AI fears reshaped the conversation. They tell you nothing about the current cycle.

Moody’s said it explicitly in last week’s sector report. Liquidity is declining among middle-market borrowers. PIK usage remains elevated. In Europe, Moody’s flagged “growing use of PIK and amend-and-extend transactions” as signs of emerging weakness.

The two PIK signals are different animals.

Original-issue PIK, where the loan was structured with a PIK toggle from day one, is benign. The lender priced it in. The borrower used it as expected.

Mid-deal PIK is the leading indicator. A loan that started cash-pay and got amended to allow PIK is a credit officer’s admission that the borrower can’t service the original debt service. The official non-accrual stat doesn’t move because the loan is technically performing. The economic reality is a borrower in trouble.

That’s the number to track. Not non-accruals. Not realized losses. The mid-deal PIK toggle insertion rate.

What to Ask This Earnings Season

ARCC just reported. The other large BDCs follow over the next two weeks.

Every manager will tell roughly the same story.

“Non-accruals stayed low. Realized losses were minimal. Spreads on new originations are wider. Deployment pipeline is strong.”

Two of those four describe a different cycle.

Skip the realized loss line on the calls. It describes the last cycle.

Better questions. The percentage of the portfolio with marks that have moved more than 5% over the last three quarters. The count of names marked between 80 and 90 cents. The Medallia bucket, where most move to non-accrual within 12 months. Watchlist additions, where the acceleration matters more than the absolute level. The percentage of loans where PIK has been added through an amendment. The number of A&E transactions in the quarter and the average extension term.

The harder question nobody asks: what share of the non-accrual book is operationally cash-generative vs. structurally impaired? Medallia is the first version, and it’s a workable runoff. Plenty of names headed for non-accrual aren’t. The first analyst to ask that on a call gets a quotable answer.

Remember, none of these numbers will be volunteered. They have to be asked.

Medallia is the first big software keys handover. Most of what’s coming after it won’t go this cleanly. That’s the part to watch.

JBI Bulletin Board

1) Octus

Most BDC research covers about 19 names. Octus tracks 170+ public and private BDCs across the universe.

Their new whitepaper, The Matured Private Credit Mandate, gets into the maturity wall, what restructurings actually look like when they resolve, secondary market growth, and the $800 billion AI infrastructure gap keeping deployment alive.

Worth a download if you cover the space.

2) Endex Partnership

I’ve been using Endex for a few months now. It’s an AI tool built specifically for credit and equity research, with deep integration into excel. Saves me time when I’m spreading financials natively in excel, pulling data sets, or putting together charts. Worth a look if your job involves any kind of credit diligence work.

2) Wharton Online Partnership

I also recently partnered with Wharton Online and Wall Street Prep on their Restructuring and Distressed Investing Certificate Program. Relevant timing given the current market backdrop in software. The program covers capital structure, bankruptcy mechanics, and distressed investing, led by practitioners at firms like Silver Point and Ropes & Gray. Code JUNKBOND gets you $300 off, with another $200 off if you enroll by May 11. Starts June 8.

3) Job opening: Arena Investors

Arena Investors is hiring a Director / Managing Director, Senior Analyst on their high-yield corporate credit team. NYC-based, hybrid. Sole coverage of companies in specified sectors across their CLO platform and opportunistic credit funds, with flexibility to invest across the capital structure.

Check out the full details on LevFinJobs.

If you liked this, you might also like:

JunkBondInvestor is an independent financial research publication providing general market commentary, corporate credit analysis, and educational content. The information provided is for informational purposes only and does not constitute investment advice, financial planning, or personalized recommendations of any kind. Nothing published constitutes a solicitation, offer, or recommendation to buy, sell, or hold any securities, nor does it guarantee any financial outcome. Any credit opinions or outlooks expressed are solely the independent views of the authors and are intended to reflect general credit trends, not specific investment recommendations. Investing in high-yield bonds, distressed debt, and leveraged loans carries significant risk including potential loss of principal. JunkBondInvestor operates under the Publisher’s Exemption of the Investment Advisers Act of 1940 and applicable state laws. This issue includes sponsored content and partnership links. JunkBondInvestor receives compensation from sponsors for featured placements and may earn referral fees from partner programs. All sponsored content is clearly marked. Editorial views and recommendations are independent and not influenced by sponsor relationships.

To be fair, private credit leverage multiples are generally higher