Credit Weekly: The Wrong Kind of Strong

For two years, bad news was good news. Friday ended that trade.

For two years, the reflex never changed.

Soft data prints, everyone reaches for the cut, credit grinds tighter. Bad payrolls meant the Fed was coming. Weak retail sales meant the Fed was coming. Every disappointment got bought because the disappointment was the catalyst for rescue. Good news was good news and bad news was good news too.

Friday broke that.

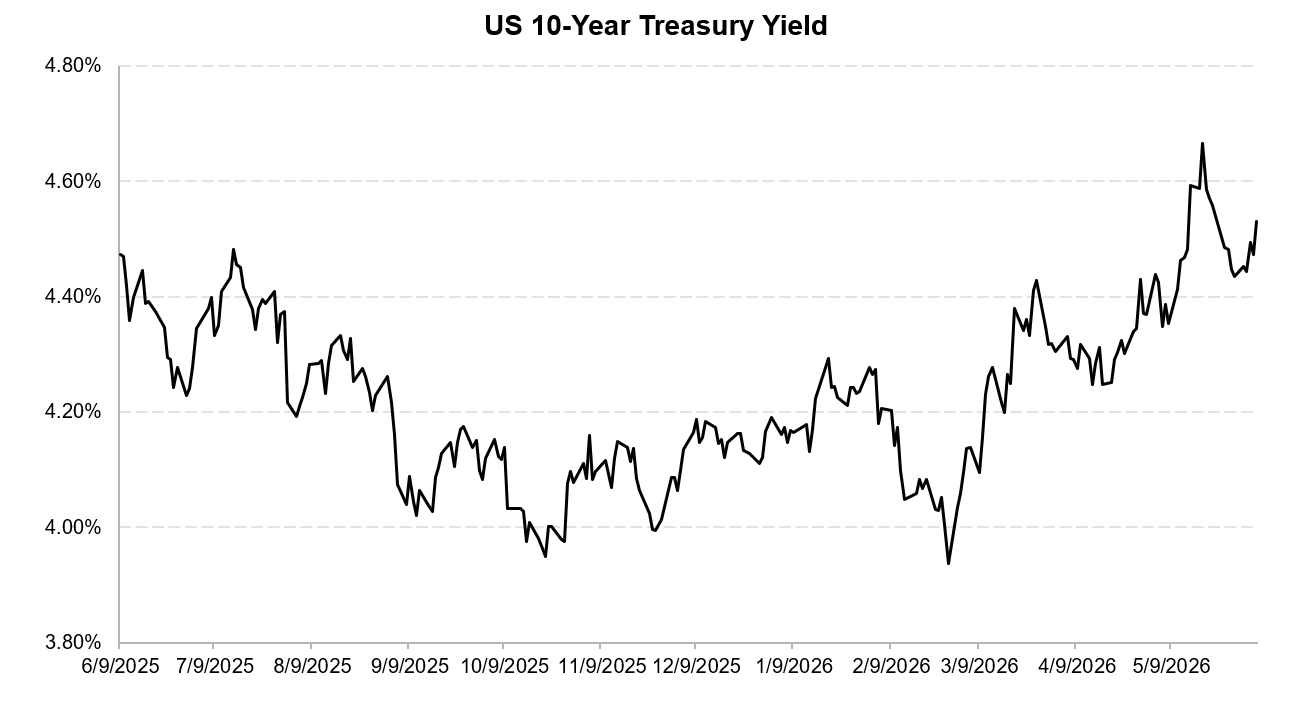

172,000 jobs against an 85,000 estimate. Roughly double, with the prior month revised up to 179k. The 10-year ripped to 4.53%. Equities had their worst week since October, ending a winning streak that had run essentially uninterrupted, on a payroll number that would have been celebrated in any normal cycle.

The pain trade for 2026 was never recession; it was reacceleration.

A labor market that inflects up instead of rolling over. An AI capex cycle that keeps getting supersized. Energy prices held firm by a conflict that won’t resolve. And a Fed that suddenly can’t ease into any of it. Strong growth stops being a comfort and becomes the risk.

We’re there now. The next move from the Fed may not be a cut anymore. It may be a hike. Maybe soon.

The macro people have been writing “more growth, more inflation” for weeks. The credit market spent those same weeks pricing the opposite. That gap closed on Friday, and it closed in the one way the leveraged credit complex is least equipped to handle: through rates, not through spreads.

Rates First, Spreads Second

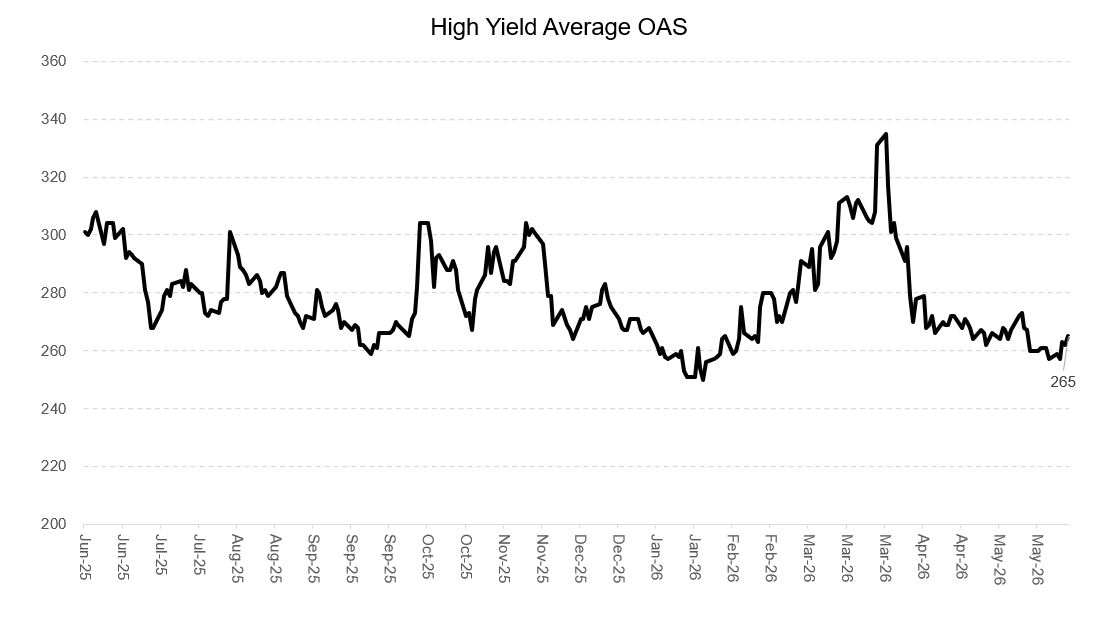

The S&P fell 3%, snapping a nine-week win streak. The Nasdaq dropped nearly 5%, the Russell 3%. Crude closed higher on the week. And HY spreads?

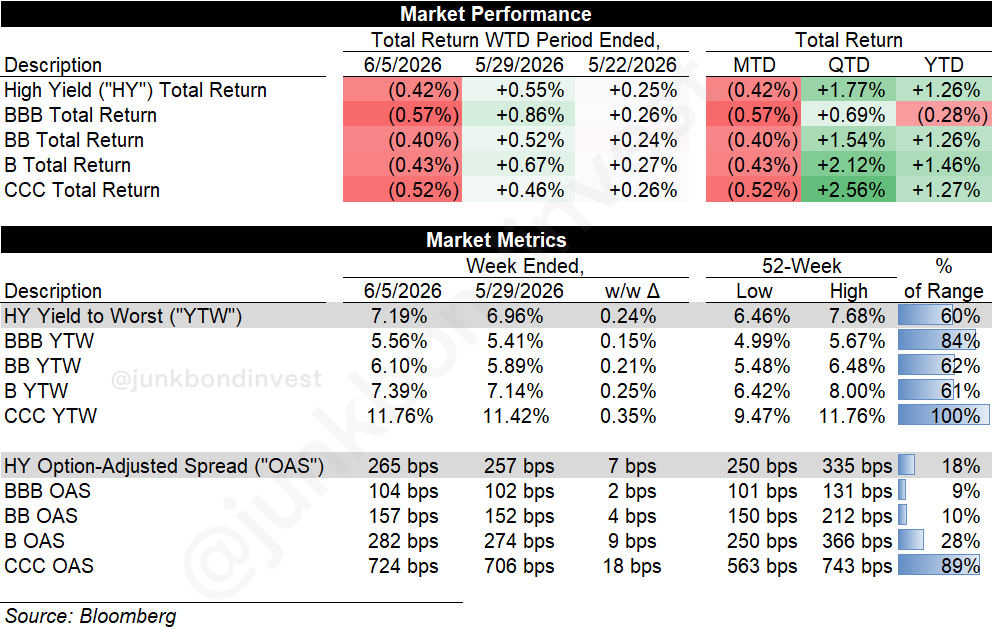

They widened just seven basis points, to 265. But HY still returned -0.42% on the week, because the yield moved even if the spread didn’t.

The bigger point may be that the equity move was largely mechanical, not fundamental: a Google $80 billion-plus equity secondary, index providers keeping inclusion rules unchanged ahead of major IPOs, and tech concentration unwinding. A rotation, not a credit event, and spreads treated it as one.

Then look at the dispersion, because it confirms this was rates, not fear.

The worst total-return cohort on the week wasn’t the junk tail. It was BBB, down 0.57%, the longest-duration, lowest-spread paper in the stack, punished precisely because it has the most rate sensitivity and the least spread to absorb it. In a genuine credit panic you’d see the reverse, the CCC tail blowing out while quality holds and everyone hides in BBs. This was the opposite.

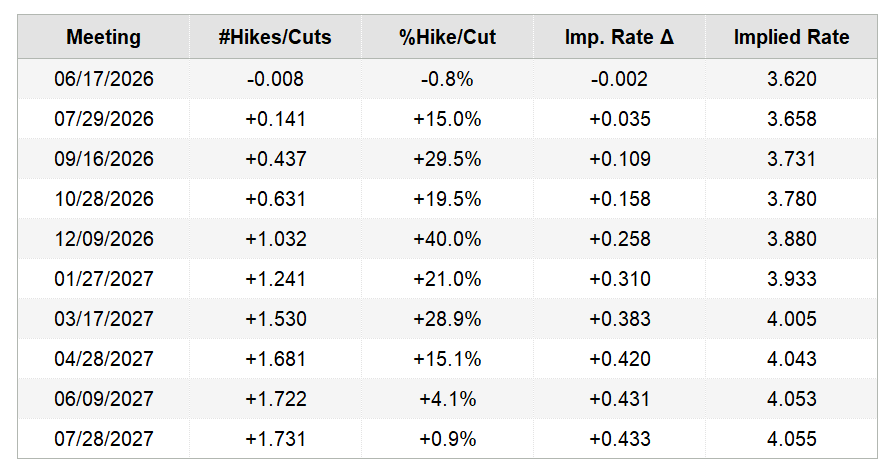

The forward curve spent the back half of last year pricing meaningful cuts. By Friday it was pricing a real chance of a hike by year-end. Seven FOMC participants already see zero cuts in 2026. Waller has gone from advocating cuts to arguing the Fed should drop the easing bias entirely; Logan has openly floated that rates may need to go higher.

The Two Economies, One Rate

None of this resolves, because the thing driving the reacceleration is structurally insensitive to the tool the Fed would use to slow it.

The US is running two economies on one policy rate.

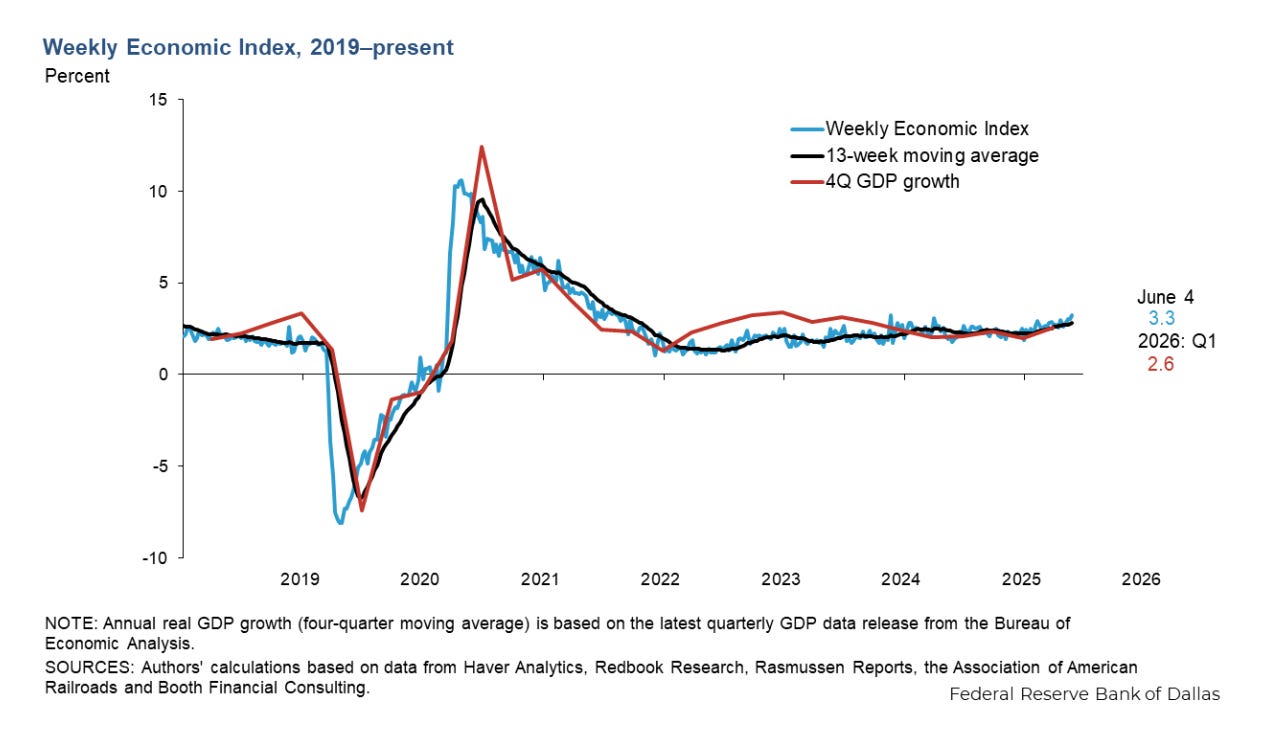

Economy One is AI infrastructure, hyperscaler capex, and the power buildout underneath it. Commitments to spend north of $750 billion on capex in 2026 alone. The Dallas Fed’s high-frequency tracker has GDP running at 3.23%.

And critically, this is no longer a pure capex story. Dell’s AI server revenue is up more than 750% year over year. Enterprise adoption is translating into real, booked demand. This part of the economy does not care what Powell does with the funds rate. It is spending regardless.

And here’s the part the soft-landing crowd keeps getting wrong: this boom is stoking employment and inflation at the same time. There’s still no real evidence of AI-driven job losses in the data. It’s Jevons paradox playing out in real time, cheaper compute creating more demand, more buildout, more hiring. The capex that was supposed to be deflationary is, right now, inflationary. That’s why a 172k payroll print isn’t a fluke. It’s the mechanism.

Economy Two is everyone who borrowed at 6-8x assuming SOFR normalizes lower. Housing frozen. Building products cyclically impaired. Consumer-facing credits grinding. Every quarter rates stay higher than the LBO model assumed is another quarter of cash flow eaten by debt service instead of equity cushion.

The Fed has one rate for both. Too low for the first, too high for the second. Cut, and you pour fuel on an AI-driven nominal growth fire while energy is already firm. Hold or hike, and you keep grinding down the levered cohort. The “Fed put” that underwrote credit since 2008 is functionally suspended, and a lot of spreads still price it as active.

And the inflation side is getting stickier, not softer. Even if the Strait reopens tomorrow, the effects persist. Inventories drawn down during the conflict have to be rebuilt, which is incremental demand after the disruption ends. Firms and governments are rebuilding around energy security: bigger buffers, redundant supply chains, diversified sourcing. All of it embeds cost.

Layer the AI power-demand curve on top, with data-center bottlenecks bidding up transformers, grid connections, construction labor, and cooling, and the pressure spills well beyond a narrow set of sectors. Structurally firmer, not transitory.

The AI Narrative Is Turning Quietly

Here’s the part that complicates my own software thesis: Software credit bounced.

The loans had their best month in nearly a year in March, and the re-rating has continued. The market is revising down the speed of AI disruption while continuing to reward the infrastructure layer. Semiconductors and data-center beneficiaries keep getting paid. Software incumbents are clawing back.

I don’t think this is the resolution of the terminal value question. I think it’s the market repricing the adoption timeline, and there’s a real argument underneath it.

The whole infrastructure trade assumes more compute is unambiguously good. But more capable models also consume more compute, and unlike traditional software, AI carries a meaningful, ongoing cost to serve each user. The economics depend on whether productivity gains scale faster than the cost of generating them.

There are already tentative signs that cost is becoming the constraint: enterprises scrutinizing AI budgets, surprise token bills, agentic workflows that don’t always survive contact with the unit economics.

If AI proves more expensive to deploy than the bulls assume, adoption gets slower and more selective. That’s bad for the infrastructure credits financing buildings against shifting revenue timelines, and paradoxically good for the software incumbents everyone spent the winter selling, because the disruption clock extends too. Both sides of the trade are betting the buildout happens on schedule. It might not.

So my framing on software hasn’t changed, it’s just gotten more textured. The terminal value question isn’t resolved. It’s deferred. And a deferred problem on a 2027-2028 maturity wall is still a problem.

Two Markets, One Screen

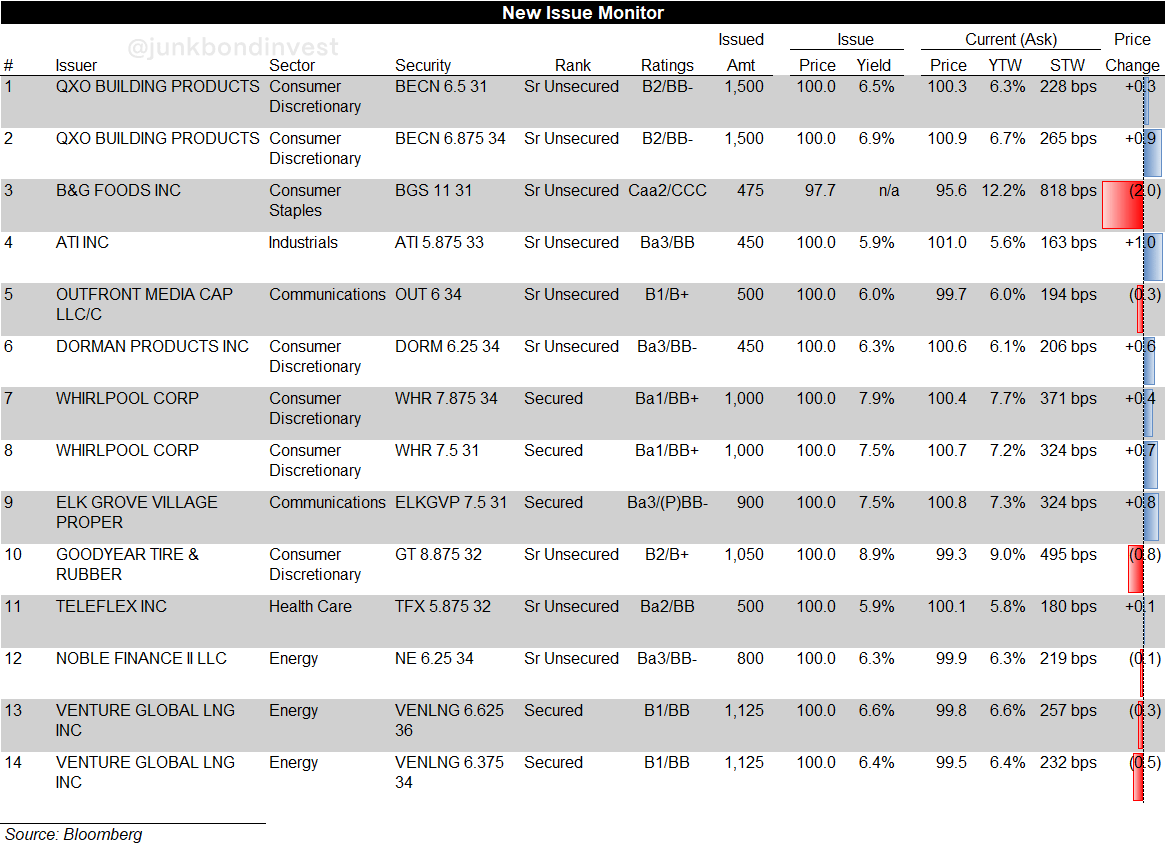

New issue came roaring back. More than $13 billion in the first three days. On volume alone, a wide-open market.

The composition and the aftermarket explain the actual situation.

QXO tapped the market for its roughly $17 billion acquisition of TopBuild. The bond piece cleared as an evenly split $3 billion deal: 6.50% five-year and 6.875% eight-year, both at par, both at the tight end of talk. Both tranches held a ~101 handle after the break.

Now hold that against the rest of the sector. The names I’ve been tracking on the distressed side, Cornerstone Building Brands, Jeld-Wen, US LBM, Cabinetworks, are a different animal. PE-owned, financed in leveraged loans, levered for a rate environment that never showed up and earnings exposed to exactly the commodity inflation we’re now staring at. Fuel and input costs will pressure margins across that group into the second half.

Two building products markets, running in parallel. The well-capitalized acquirer prints at par. The over-levered 2021 vintage sits in the 70s waiting for a spring selling season the macro just made harder. The difference isn’t the sector. It’s the capital structure and who owns the equity.

If QXO is the market open and cheap for the right borrower, B&G Foods is the other side of it. The food company paid 11.625% to refinance a 2027 maturity and still watched the bonds fall to the mid-90s, and that coupon came after it had already halved its dividend. That’s the point. The market is open, but for the wrong borrower it’s open after the dividend cut, after the deleveraging promise, and still at an 11-handle.

What to Watch: CPI Wednesday

The verdict on all of this lands Wednesday.

The desks are penciling May CPI at +0.52% on the month, which pushes the year-over-year rate to roughly 4.2%, a three-year high. Energy goods, mostly gasoline, up around 8%. Core a more contained +0.23%, but airfares set to jump on the jet-fuel surge and the Spirit Airlines bankruptcy. Gas is back above $4 a gallon for the first time since 2022.

A 4.2% headline doesn’t give the Fed room to validate the cuts still half-embedded in the curve. It does the opposite. And it’s not just a US issue: the ECB looks set to start hiking, 25bp with a hawkish bias, and the Bank of Canada is holding at 2.25% with the path tilted to hikes. This is a Treasury-supply and term-premium story before it’s a credit story.

If CPI prints hot, the rates move that drove this week extends, and the BB complex takes the next leg of damage while the short-duration, high-carry tail keeps outperforming. If it surprises soft, you get a relief squeeze into a heavily short book. I lean to the hot side on the data, but I hold the squeeze risk in mind.

And the oil side just got worse, not better. Crude finished the week higher, and the comment that matters came from Trump: the blockade may not lift until Labor Day. That pushes any reopening of the Strait well past the point where it would help.

One thought I keep coming back to.

For two years, this market was conditioned to believe that weakness would always be rescued, because it always had been. The thing that breaks that conditioning isn’t a recession. It’s strength, the kind the Fed can’t lean against without making the inflation worse.

That’s the uncomfortable shape of this cycle. The economy is fine. That’s the problem. The good news is the bad news now.

JBI Bulletin Board

1) Something New is Coming

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. Buy-side experience required, ideally software or building-products coverage. You know the names, the docs, and the playbooks. If that’s you, or someone you’d vouch for, reply with a short note on your background.

Thanks. The May CPI is absolutely crucial. Here are my estimates which have been better than Wall Street 70%-75% of the time:

https://arkominaresearch.substack.com/p/may-2026-cpi-estimate

The Fed put that underwrote credit since 2008 being functionally suspended while spreads still price it as active is the most expensive assumption in the market right now.

The two economies that one rate problem doesnt resolve cleanly. Cut and you pour fuel on nominal growth that doesnt need it. Hold or hike and you keep grinding the levered 2021 vintage that priced for a world that didnt arrive. The BBB cohort taking the worst total return on duration sensitivity rather than credit quality is the data point that tells you this is a rates story not a credit event. For now.