Bath & Body Works ($BBWI) Bonds: Cheap for a Reason, or Just Cheap?

2.0x leverage, $600mm of FCF, nothing due until 2028, and an 7.7% YTW long bond. What's the catch?

Everyone hates retail credit, and the reasons are good ones.

The category has been a graveyard for a decade. E-commerce hollowed out anything you could buy without touching it, store leases turned into a fixed cost that crushes you the moment comps go negative, margins are thin enough that one bad season tips the model, and the list of names that went from investment grade to liquidation is long enough that the reflex to pass is rational.

So you skip it. You see a fragrance-and-candle retailer with declining sales and you move on.

Bath & Body Works gives you every reason to do exactly that. Comps have been negative for quarters. Body Care is bleeding share. The CFO is walking out mid-turnaround. On the surface, this is the same retail story you’ve passed on a hundred times.

But the debt might not need the turnaround to work. And it’s trading wide. So the question is whether that’s a mispricing or the market getting it right.

Situation Overview

Bath & Body Works (Ba2/BB+) is a specialty retailer of personal care and home fragrance. You know the brand: the body lotions and mists, the hand soaps and sanitizers, the candles and Wallflowers that anchor the Home Fragrance line.

BBWI 0.00%↑ came out of the old L Brands in the 2021 split that also created Victoria’s Secret. The result left a clean, pure-play operator with ~1,900 company-owned stores across the US and Canada, an e-commerce channel it calls Direct, a franchised international fleet that costs almost nothing to run, and, since February, wholesale distribution on Amazon.

Three categories carry the business.

Body Care is the core, the franchise the brand is known for.

Home Fragrance is the candle business, weighted to the holidays.

Soaps and Sanitizers is smaller and steadier.

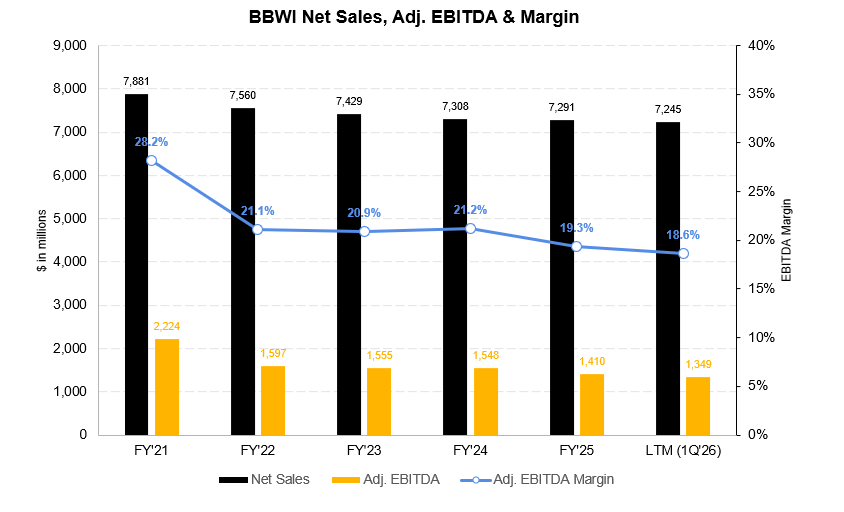

From a lender’s perspective, the credit appeal is these are consumable, replenishment categories, so the revenue base holds up better than apparel. Customers come back on a cadence, gross margins sit in the low-to-mid-40s%, and the business throws off $600-800mm of FCF in a normal year.

Fragrance is bought after sampling, which is why these stores never got hollowed out the way commodity apparel did. That cash flow profile, not the growth, is what keeps this retailer at BB-ratings instead of single-B.

What’s been happening

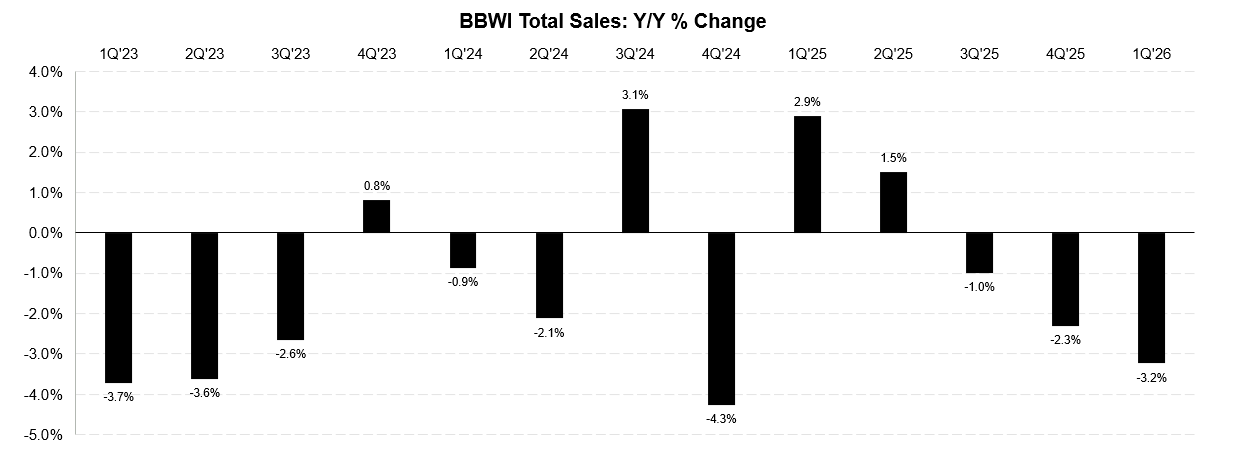

For most of the past year the story hasn’t changed: comps down, and getting worse. 1Q’26 kept the trend going. Net sales dropped 3.2% to $1.38bn, and Adj. EBITDA declined about 22% to $212mm. Gross margin gave up nearly 270bps, pressured by tariffs, inflation, and the deleverage of spreading a fixed cost base over a smaller top line.

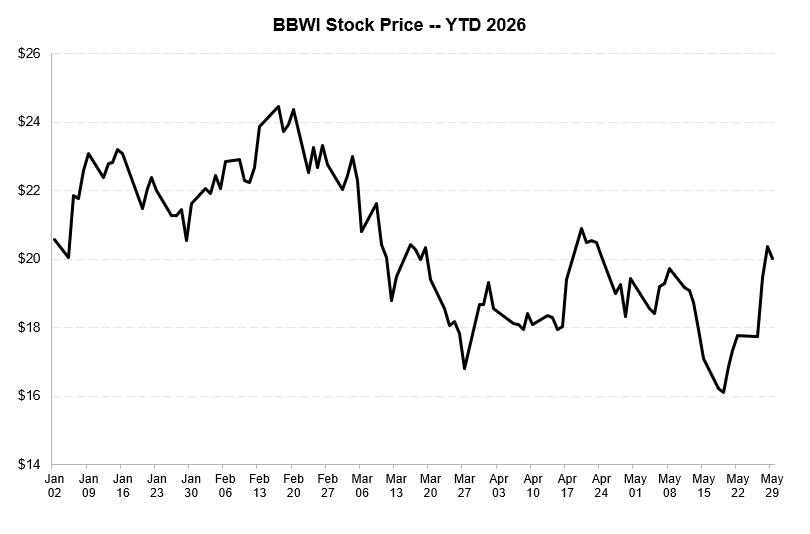

The market actually read it as a relief print. Expectations were on the floor, guidance held, the 2Q’26 guide came in no worse than feared, and the equity rallied.

Taking a step back, nothing in the trajectory actually moved. Sales are still falling, and the recovery is still something management is describing rather than delivering. They have pointed to a second-half inflection for several quarters now, and the inflection has not arrived.

What’s actually broken

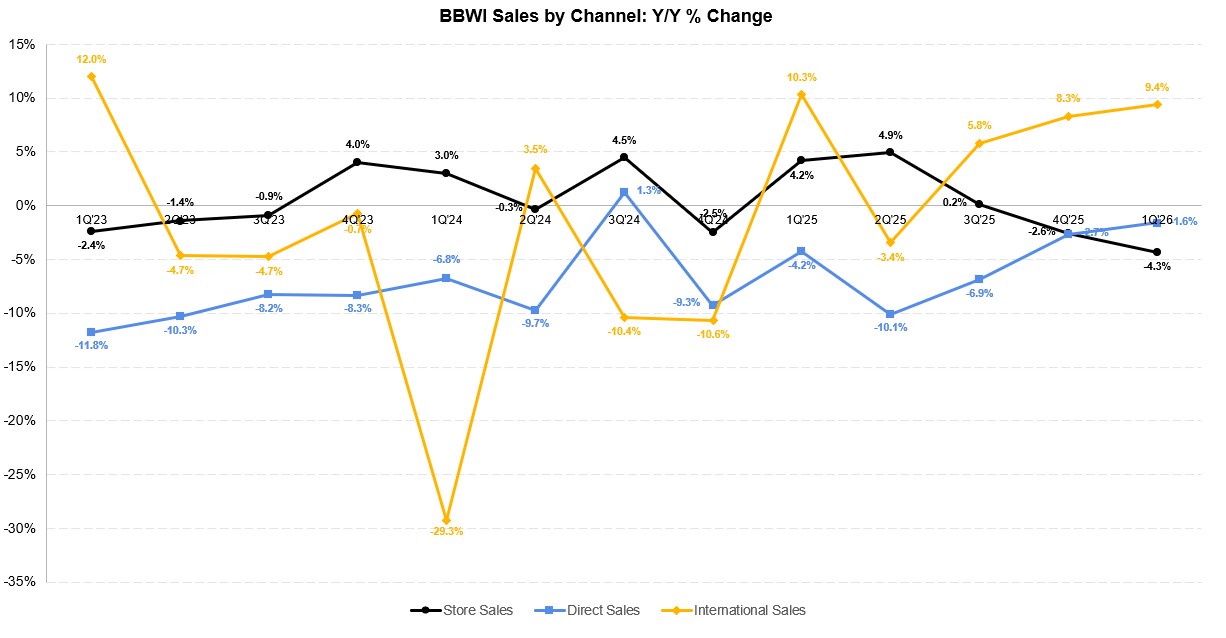

Almost all of the weakness sits in one place. Body Care, the heart of the brand, was down “mid-teens” and has now decelerated three quarters running while the rest of the business held roughly flat. The core is the part that is bleeding.