Credit Weekly: The Wrong Binary

The safe name got bombed. The doomed one got saved. The sector label called neither.

Every credit desk now runs the same screen. AI-exposed or AI-safe. Software and disruptable services in one bin, hard assets, infrastructure and contracted-revenue names in the other.

This week the sort broke, in both directions.

Verra, the kind of recurring-service credit everyone had in the safe bin, got bombed this week. Rackspace, a services name the market had left for dead, has spent the spring getting saved. Same force, opposite outcomes.

The bins do not hold. The mechanism underneath them does, and it is the better cut anyway.

The Safe Name That Broke

Until now, AI disruption in credit has been a slow story. Terminal value, net revenue retention, who loses pricing power over the next three years as the models improve. Erosion you could see coming.

Verra is something faster.

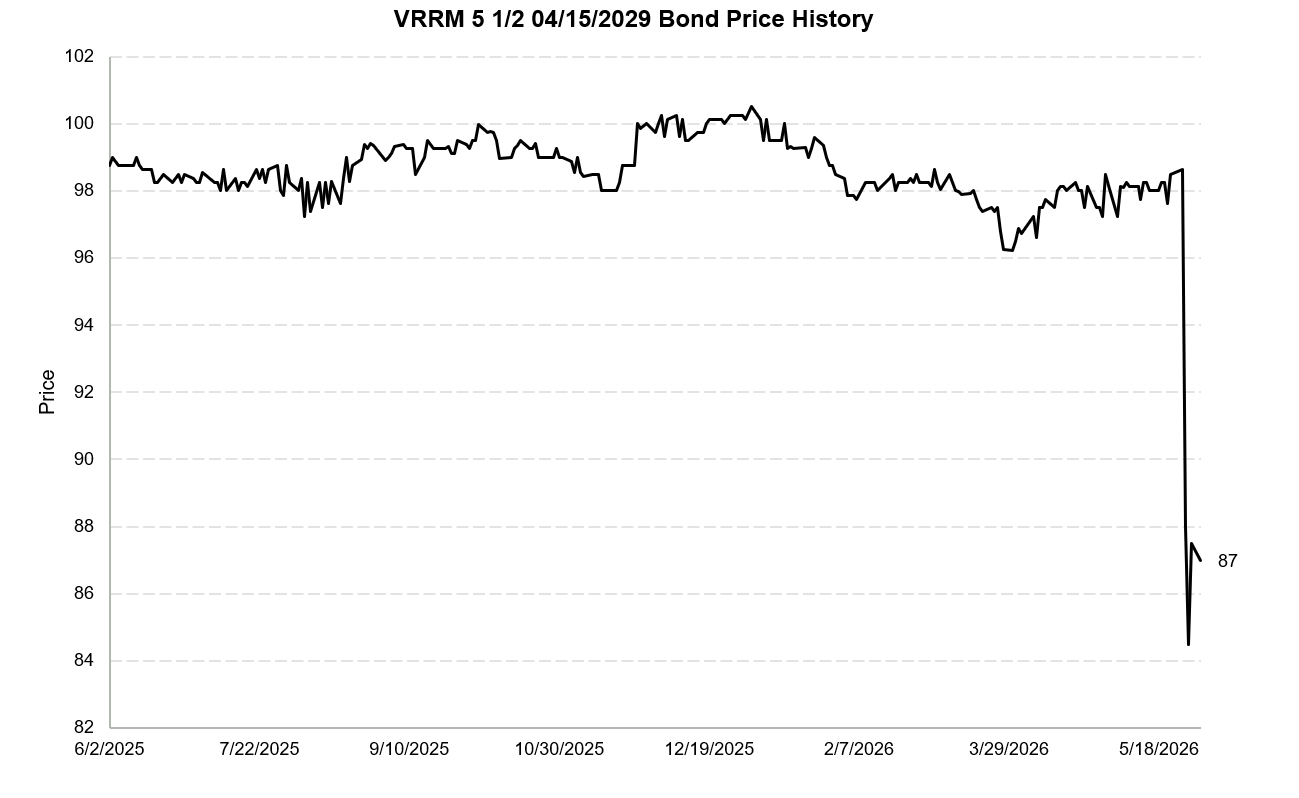

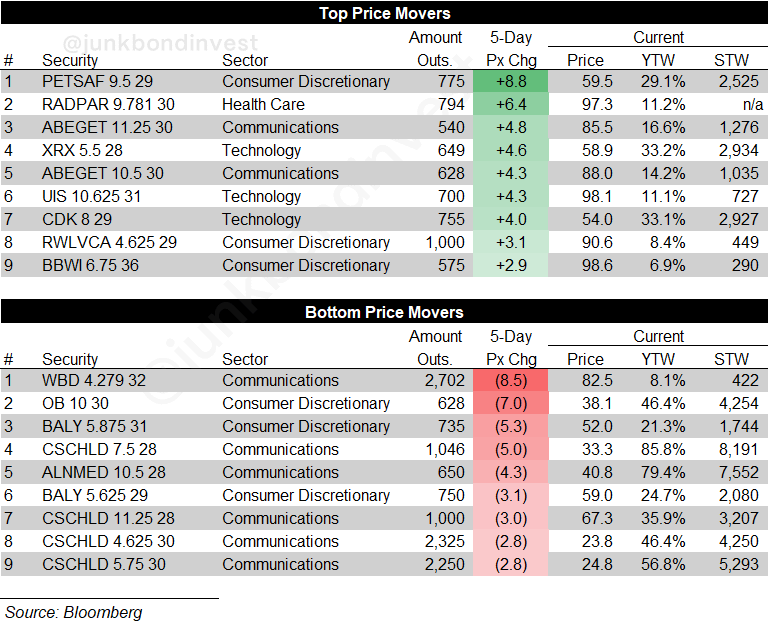

Avis terminated its tolling contract, a high-margin slice of Verra’s commercial services and more than a tenth of total revenue, effective September. The equity was cut in half on the day. The bonds had traded near par. They fell into the high 80s. Suddenly and violently.

The headline 2026 numbers barely moved, because the loss only lands for one quarter of the year. The real damage is a 2027 event, and 2027 is also when Verra’s other two big rental-car customers, Hertz and Enterprise, renew. The three contracts together are something like 80% of commercial services and a third of the company. So the market did not reprice this year’s print. It repriced whether Avis is one-off or the first of three, a year before the income statement will say.

The market’s shorthand for the fear is vibe coding. But nobody has confirmed Avis is even building this in-house rather than just switching to a competitor, and the real issue was never whether an AI tool can write the software. It is what one termination did to belief. A workflow the market had underwritten as mission-critical plumbing got re-underwritten, overnight, as something a determined customer might rebuild. The cause of the cancellation barely matters. The repricing of substitutability is the event.

Verra’s defense is that the moat was never the code. It is the plumbing. Millions of vehicles, hundreds of toll authorities, and the violations, billing, disputes and registration machinery that took years to wire together. AI writes code. It does not stand up that network over a summer.

The bulls will tell you the government and parking businesses carry the debt even if every rental-car dollar walks. Maybe. The point is not who wins that argument. It is that the market repriced the credit to stressed before anyone could have it.

The Doomed Name That Didn’t

The names that screen as most exposed did the opposite of Verra this week. The most-active paper in high yield was CoreWeave and the rest of the AI-infrastructure complex, which has printed oversubscribed in primary all year. For those credits AI is not a threat to the revenue line. It is the revenue line. The more AI there is, the more compute, memory and power the customer buys, and the better the credit gets.

That is the easy half of the pole. The harder half is the inversion, and Rackspace is the cleanest version of it I have seen in credit.

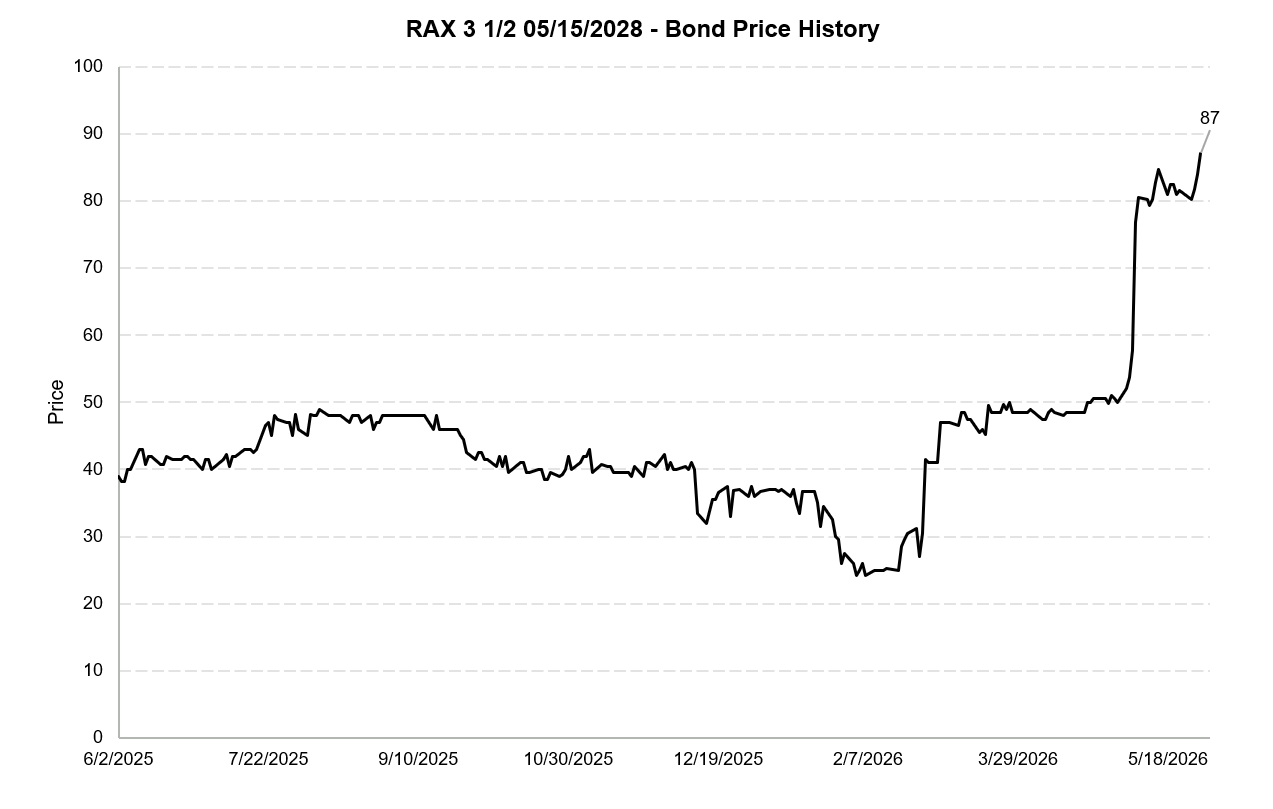

Rackspace ran an LME two years ago to cut debt and buy liquidity. Earlier this year the debt traded around 30 cents, and it fell further in February in the same AI selloff I was writing about then, priced as one more business about to be disrupted into the ground. The company used the weakness to buy back nearly 100 million of its own paper.

Then the story turned. A non-binding MOU with AMD in May to build an enterprise AI cloud, the companies explicit that talks were preliminary, on top of earlier tie-ups with Palantir and Uniphore. The secured debt ran from the 50s to north of 80. Look at what moved it. Not contracted revenue. A framework. The bonds repriced optionality, not cash flow, which is exactly the convexity you want in a name the market had buried.

The driver is the cleanest consumed mechanic there is. AI moving from training to inference broadens demand for exactly the GPU and CPU workload management Rackspace sells. Roughly 2.5 billion of 2028 maturities still hangs over it, so this is not finished. But it is a credit the disruption tape left for dead and the consumption tape brought back.

Two credits, opposite outcomes. The sector label called neither. The mechanism called both.

Consumed or Replaceable

Here is why the AI-exposed versus AI-safe binary fails. It sorts on sector. The thing that actually determines the credit outcome is mechanism.

The real axis is whether AI makes your product more consumed or more replaceable.

Consumed means your product is the surface the models run on, or the thing AI creates more demand for. Compute. Memory. The data layer. The fraud defense. The more AI there is, the more of you the customer needs.

Replaceable means your product is a workflow, an output, or a labor arbitrage that a motivated customer can now reconstruct. The proprietary report. The back-office process. The seat of a credit analyst ;)

This axis cuts straight across the old line. Rackspace sits on the consumed side. Verra is being accused of the replaceable one. NIQ, Kantar, Gartner, Accenture, the running joke about advisors replaced by Claude, none of them software, all of them priced as replaceable.

The diligence question is no longer how sticky is the revenue. It is which side of the axis the business sits on.

What the Week Said

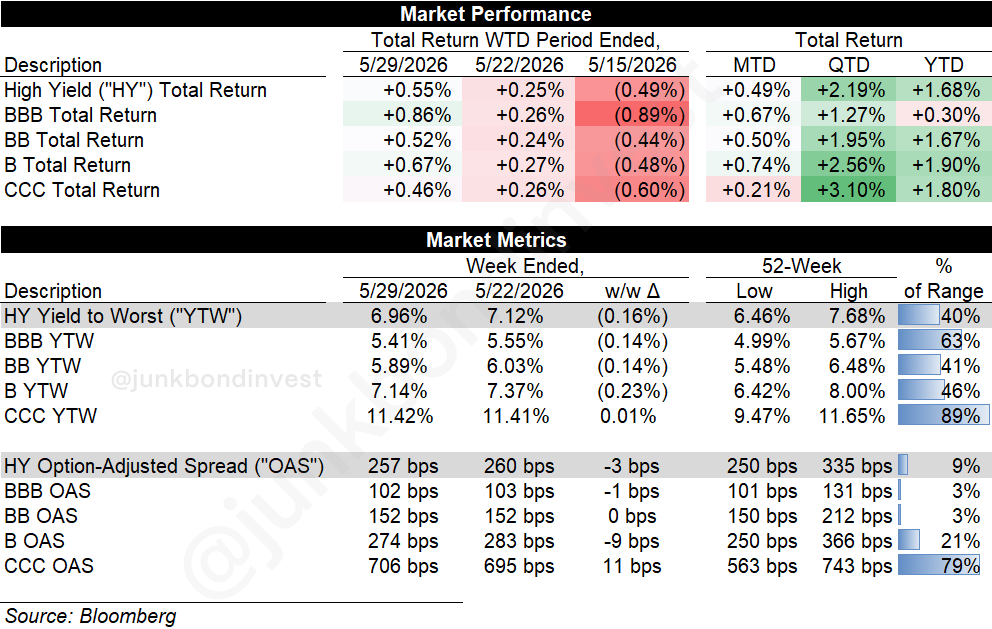

The headline index did almost nothing. High yield returned about 0.55% on the week. Spreads ended flat around 257 bps, the ten-year hovered near 4.44%, and the all-in yield came in 16 bps to 6.96%, with effectively all of that move coming from rates rather than spread.

Underneath, the dispersion that the index always hides. Flight to quality within high yield, the B-versus-BB differential pushing toward the top of its historical range. The rating buckets are pulling apart while the headline sits still. The index is lying to you, again.

Equities went the other way and went hard. The Nasdaq 100 cleared 30,000, Micron crossed a trillion dollars for the first time with its high-bandwidth memory already sold out for the year, and May closed up double digits for a second straight month.

The two poles sat on the same leaderboard. Avis’s bonds were among the most-traded names in high yield this week, right next to the AI-infrastructure complex. The tape that bid compute to the top of the volume list took the name AI was used to threaten from near par into the high 80s.

Which is the problem with owning high yield as a number right now. You are being paid less than you have all cycle for a tail that is quietly getting fatter.

The Refi Tax

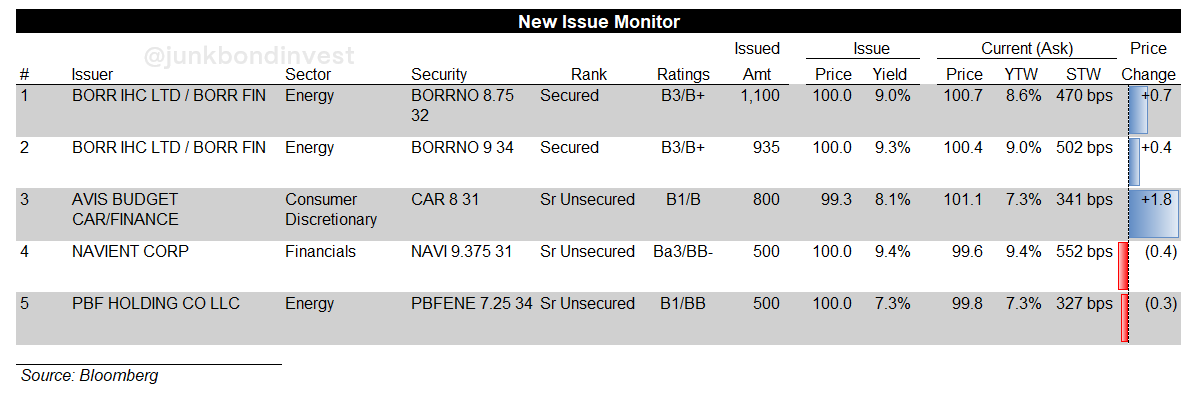

Four billion priced across five deals, bottom of the syndicate range, a holiday week pinched around the GS leveraged finance conference.

The theme was the cost of capital, and it cut both ways. The low-coupon maturities got repriced sharply higher. Navient paid 9.375% to take out 6.75s. PBF came 7.25% to refinance 6s. Avis printed its 8% add-on at 7.77% to chip at the 5.75% 2027s.

And the names refinancing down still landed expensive. Borr Drilling upsized to 2.035 billion of secured to retire 10% and 10.375% paper, and the best it could print was 8.75% and 9%.

Whichever direction the refi ran, everyone cleared at eight to nine and up. The maturity wall is not a wall. It is a repricing, and it lands hardest on exactly the levered names the feature says AI is already pressuring.

And before anyone reads consumed as safe. The most consumed credits alive, the AI-infrastructure names, are also the most capital-hungry, rolling enormous capex into this same eight-handle market. In the third quarter the largest tech firms spent more on capital investment than they earned from operations.

The revenue tailwind sits on top of a balance-sheet hole. Consumed protects the top line. It does nothing for the refi. It is a second tail, not the absence of one. And the rate relief that would close either tail may not be coming, for the reasons I laid out last week.

The Screen Worth Running

Stop sorting the book by AI-exposed and AI-safe. Re-sort it by consumed versus replaceable. The mislabeled names are where the edge lives: a credit whose real moat is operational plumbing, priced by the tape as if it were replaceable code.

The replacement-fear overshoot is a buy list, not a short. When a credit gaps on a replacement headline and the customer that pulled the contract is itself running negative EBITDA, that is convexity, not confirmation.

Fade nothing in AI infrastructure on valuation alone, but respect that the most-traded paper in high yield is now the most consensus. Crowded is not the same as wrong. It is just crowded, and it gets repriced faster when the story wobbles.

And do not confuse a melt-up with a healthy credit tape. The equity index is green because ten names are green. Underneath it the buckets are separating, and the headline is the last place you will see it.

JBI Bulletin Board

1) Built for the Desk

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. Buy-side experience required, ideally software or building-products coverage. You know the names, the docs, and the playbooks. If that’s you, or someone you’d vouch for, reply with a short note on your background.

I think you’ve covered this dynamic previously but part of the move in RXT is just following the equity higher. And the equity could just be in a squeeze on the PLTR and AMD headlined plus high short interest relative to float. That said, it’s been impressive to see the equity stay resilient and even squeeze further despite ABRY fully exiting their sizable stake. There must be real believers.