Credit Weekly: The Fed Can't Cut Transformer Lead Times

Equity Sees Growth. Credit Should See Capex.

AI is supposed to be deflationary.

That is the narrative investors want to believe. Software agents replace back-office labor. Models automate workflows. Productivity rises. Services inflation eventually rolls over because expensive humans get swapped for cheaper code.

Maybe. But before AI becomes deflationary, it has to become extremely capital intensive.

It needs data centers. Data centers need land, power, transmission, substations, transformers, cooling, backup generation, fiber, gas turbines, construction labor, and years of utility planning. The model may live in the cloud, but the cloud still needs a grid connection.

That is the part the Fed cannot solve.

Rates do not fix transformer lead times. They do not clear transmission queues or build gas turbines faster. They do not unwind hyperscaler capex commitments. The Fed can slow demand at the margin, but it cannot print power infrastructure.

That is why the AI trade is starting to become a credit one.

Equity Sees Growth. Credit Should See Capex

Equity investors have treated the AI buildout as a clean growth story. Nvidia gets the multiple. Hyperscalers get the strategic narrative. Power assets get re-rated. Data center landlords get the secular demand story. The entire complex has moved from “infrastructure” to “AI infrastructure,” which is the kind of label that usually makes capital cheaper until everyone remembers capital still has to be repaid.

Credit should be less comfortable with this.

The first stage of the AI buildout is not software margin expansion. It is an industrial capex boom running into a constrained physical system. Power is scarce. Equipment is scarce. Interconnection is slow. Permitting is political. Utility bills are already a cost-of-living issue.

The numbers back this up. Consensus 2026 AI capex estimates are around $750 billion (I’ll take the over on this). Power demand is rising materially for the first time in decades. Grid operators in Texas, Virginia, Georgia, Arizona, and parts of the Midwest are warning that hyperscaler buildouts are reshaping capacity forecasts. Utilities are filing rate cases citing data center demand. Transmission investment requirements are accelerating.

This is not some abstract long-term problem. It is the exact type of supply-side constraint that keeps inflation sticky and makes the Fed’s job harder.

I wrote about this a couple weeks ago through the 1990s telecom analog. Supply doesn’t widen spreads mechanically. It builds the vulnerability. The cracks show up in the marginal cohort first.

Credit Is Still Behaving Like the Rate Environment Doesn’t Matter

You have seen the front-end repricing.

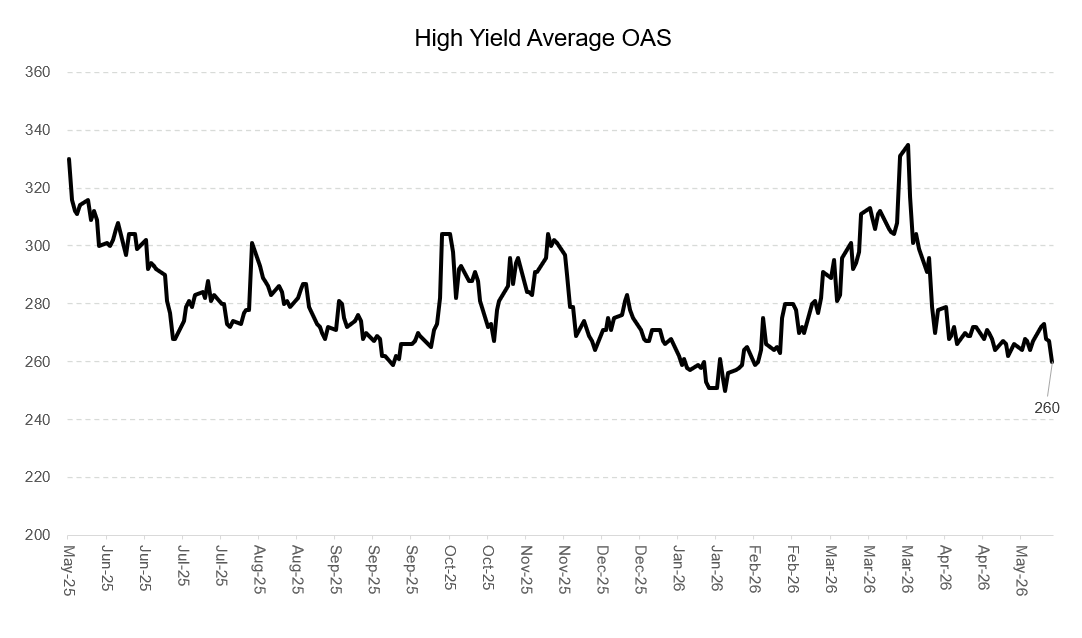

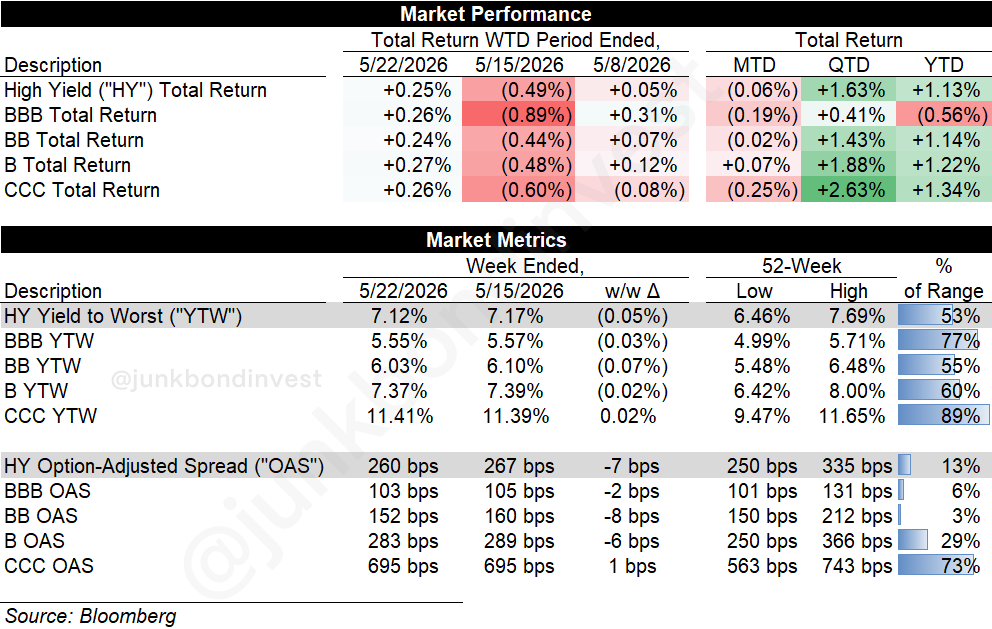

Front-end pricing for 2026 has flipped from cuts to hikes in a matter of weeks. The move in the implied policy path is on the order of 80 bps. The rates market has done most of the work. Credit has barely moved. High yield spreads are actually tighter over the same period.

Those two things do not sit comfortably next to each other. The rates market is saying the Fed may not have room to cut. Credit spreads are still behaving like the Fed path does not matter much.

The incoming data is easier to square with the rates move than the spread move. April PPI ran hot at 1.4% m/m and 6.0% y/y, and the pressure was not isolated to energy. Goods passthrough showed up across transportation, metals, building materials, and industrial chemicals. ISM prices indices stayed elevated on both the manufacturing and services side, with services prices back near the highs of the current cycle. The ADP weekly pulse firmed into a monthly run-rate well above what the Fed itself characterizes as breakeven payroll growth.

None of these are individually decisive. Together they do not describe an economy giving the Fed cover to cut. None of this is obvious, especially in BB spreads at 152 bps.

HY index spreads now sit 10bps wide of their 52 week lows. Meanwhile, the 10-year Treasury is up nearly 50 bps YTD at 4.56% vs. the HY index yield at 7.12%. The attribution is not flattering: returns have been carried by coupon, while rates have been a drag and spread compression has done very little.

Carry is still printing. That part is true. The issue is whether the conditions that made carry easy survive another quarter where AI capex keeps pulling on the same physical inputs the Fed cannot conjure.

The Market Is Open, But the Price Discrimination Is Real

A Fed stuck between sticky inflation and political pressure does not shut the new issue market. It splits it.

RR Donnelley priced an upsized $900 million five-year senior PIK note. 11% coupon, 95 OID. Fitch moved the outlook negative on higher pro forma leverage in the low-5x area.

Same week, Granite Construction priced $600 million of 6.375% eight-year senior notes at par to refinance old converts.

Granite at 6.4%. RRD at 12.4% PIK. Same week. Roughly 600 bps apart on clearing yield.

The market is not closed. Strong credits refinance. Quality borrowers extend maturities. HY spreads stay tight. Weaker borrowers can still get deals done, but the price starts to look like punishment.

The interesting part is that AI is now on the other side of that triage. The market has infinite imagination for the capital needs of the AI buildout. It has much less patience for old-economy borrowers trying to refinance levered balance sheets at the wrong point in the rate cycle.

AI gets the growth multiple. Legacy refi risk gets the coupon.

Power Is Where the Politics Starts

Certain credits have treated the AI power complex as a clean tailwind.

Talen, Vistra, NRG, and Constellation traded as utility or power names two years ago and now trade as AI infrastructure plays. CoreWeave moved from novelty borrower to somewhat accepted institutional credit. Bitcoin miners, electrical equipment names, power generators, utilities, and cooling assets all sit somewhere on the same narrative map.

The demand story is real. The supply response is slow. That is why the trade worked. The next phase is harder.

US electricity demand is rising for the first time in decades and ratepayers are being asked to absorb more of the bill. Iran has pushed gas prices higher. Power bills are climbing too, partly because hyperscaler buildouts are driving demand growth that utilities pass through to customers.

The cleaner AI story gets harder when the power bill leaves the data center and lands in the regulated rate base. A hyperscaler PPA may be contracted. The household bill is political.

The cost-of-living backdrop is already strained. Real incomes have not kept pace with prices for most households, inflation approval is in the high 20s for the administration, and energy is back in the headlines as a household-budget item rather than a macro abstraction. Higher power bills hit the same working-class base through a different channel than the pump.

The political coalition that has tolerated the AI buildout starts to look less stable when the buildout shows up as utility bills, transmission fights, land-use battles, and local permitting pressure.

The issue is whether the local cost allocation case becomes politically intolerable before the productivity gains show up in household incomes. That is a credit problem before it is a macro problem, because the names exposed to local cost allocation fights are levered, regulated, and trading like the tailwind is one-directional.

That is not an anti-AI argument. It is the politics of who pays.

The PUC Is Where the AI Trade Meets the Customer Bill

State Public Utility Commissions (“PUCs”) are political animals. They feel pressure faster than federal regulators.

In states like Virginia, Georgia, and Ohio, data center cost allocation is already becoming a live regulatory issue. The direction of travel is toward less socialization, more scrutiny of large-load tariff structures, and higher customer contributions to interconnection costs. Virginia rate cases over the next two quarters are worth watching closely.

If the politics turns, the IPPs and utilities are probably easier pressure points than the hyperscalers. Hyperscalers bring jobs, capex, lobbying capacity, and federal influence. Utilities and IPPs sit closer to the customer bill, which makes them easier to drag into the state-level fight over who pays for the grid.

That does not mean the demand story is fake. It means the easy “AI infrastructure is a one-way tailwind” phase is probably over. The next phase has more regulators, more politics, and more attention to who absorbs the cost.

The question is whether these AI-credits should trade like a clean infrastructure credit, or whether the market eventually demands a larger concession once power, permitting, and regulatory risk are priced more explicitly. Same question across the IPPs, data center names, and power-linked credits. Some have contracted demand. Some have merchant exposure. Some have regulatory protection. Some have regulatory risk.

The market is still learning the difference.

What This Means for Credit

The first AI trade was Nvidia and the direct GPU ecosystem. The second was power. The third may be higher funding costs for everyone not attached to the buildout, and a political ceiling on some of the names that are.

That matters for broader credit because the AI capex cycle is not happening in a vacuum. It is happening while inflation is sticky, the Fed path has repriced hawkishly, and spreads are still trading like carry is the only thing that matters.

There are three implications: