$WIX Converts at 78: AI Loser or Buying Opportunity?

AI disruption, a $1.6bn tender, and a 2030 maturity wall

Every SMB software company is being asked the same question right now. What happens when the customer stops needing you and just asks a chatbot?

Most are pretending the question doesn’t exist. Wix decided to do something about it. Went out and spent on the answer. Bought Base44. Built Harmony on a proprietary LLM. Pushed distribution into ChatGPT and Claude. Ran a Super Bowl ad.

You can see the spending in the numbers. You can also see it in the share price. Down 48% this year alone.

The convert has moved but not to the same degree. Busted and trading on yield. High-70s, ~6% YTM, priced like IG-adjacent software paper. The question now: is 6% enough?

Situation Overview

Wix sells subscription software that lets SMBs, freelancers, and agencies build and run websites without writing code, plus a layer of business apps on top (payments, commerce, bookings, domains, email, paid ads). Mostly recurring, paid upfront, low capex. Until recently it ran at low-to-mid 20s% FCF margins with a clean balance sheet.

Three things changed that.

The first is AI. The customer question shifted from “I need a website but can’t code” to “I should be able to describe what I want and have software build it.” Wix’s attempt to answer that is two products:

Wix Harmony is an AI site builder integrated into the core platform that launched in late Jan’26.

Base44 is a “vibe coding” tool that lets non-technical users describe an app or workflow in plain English and have software build it. Wix acquired Base44 in mid-2025.

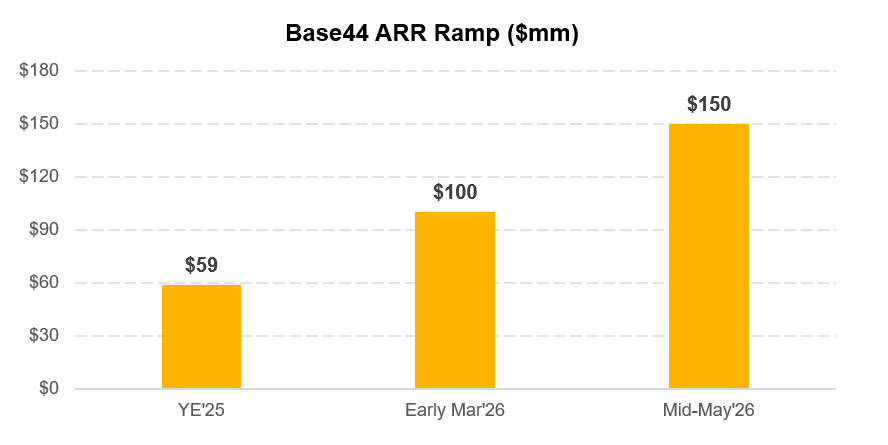

Base44 has scaled fast: $59mm at YE’25, $100mm by early Mar’26, $150mm by mid-May’26. Harmony now runs on a proprietary in-house LLM, which management has described on the Q1’26 call as meaningfully lower cost than 3P alternatives. Wix is also pushing distribution into AI platforms, including Base44 inside ChatGPT and MCP integrations with tools like Claude and Cursor.

The pitch is that these products move Wix out of website builder land and into a bigger AI-powered web, app, and workflow market.

The second change is that the cost of all this showed up in Q1’26.

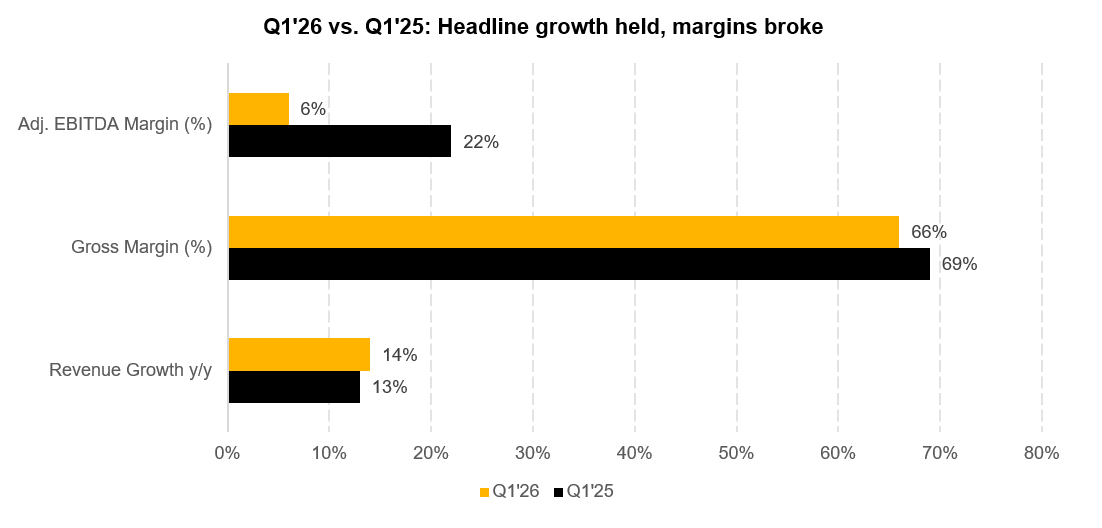

Revenue grew 14% y/y to $541mm. Bookings grew 15% to $585mm. New user cohort bookings up ~46%, with the Q1’26 cohort adding ~6mm new users. Headline looked fine. Go down the P&L. Adj. EBITDA was $34mm (6% margin) vs. $106mm (22% margin) in Q1’25, well below consensus.

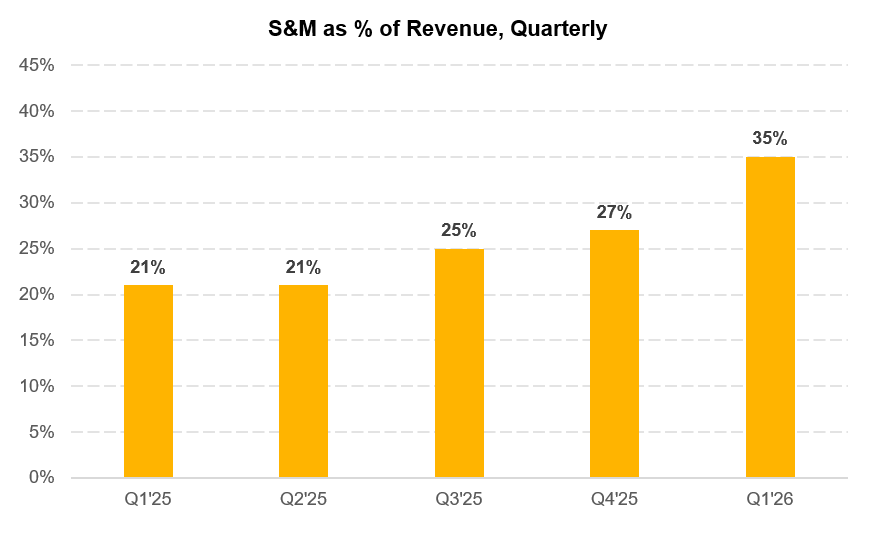

S&M nearly doubled y/y to $191mm, or 35% of revenue vs. 21% a year ago. That includes $20mm+ of Super Bowl spend. Per management commentary, the other ~$90mm went to acquisition marketing across core Wix and Base44, with blended TROI extended to 7-9 months. FCF was $75mm, $112mm ex-acquisition costs, against $142mm in Q1’25.

The stock fell 27% on the print.

Guidance moved with the print. FY’26 revenue and bookings stayed at mid-teens, but FCF margin guidance (ex-acquisition costs) was cut from low-to-mid 20s% to high-teens. Management attributed ~$100mm of that to foregone interest income and new interest expense from the tender, plus a ~$64mm FX headwind from a stronger Israeli shekel weighted to 2H’26. None of those explanations are wrong. But taken together, they describe a business that now requires more marketing spend and more capital.

The third change is the balance sheet.

In Apr’26, Wix completed a modified Dutch auction tender, buying back ~17.5mm shares at $92 for ~$1.6bn. Almost 30% of shares outstanding. Funding came from cash on hand and a new $500mm credit facility from Bank Hapoalim. The transaction left Wix with roughly $1.65bn of gross debt, including the new $500mm bank facility and $1.15bn of 2030 converts, against the net cash position the company carried for years. Two months later the stock is at $55.

The facility terms are more interesting than the headline borrowing capacity. Hapoalim got liquid assets sitting with the lender, contractual and statutory lien and setoff rights, a negative pledge against a general floating charge, and a financial covenant. Specifically, Wix has to maintain ~1bn NIS of Israeli Treasury Bills (Makam) at the bank and keep its existing $120mm cash deposit there, with a Bank Debt / FCF covenant capped at 2.0x.