Verra Mobility ($VRRM): Did Avis Just Vibe Code Its Own Back Office?

What creditors actually recover if Hertz and Enterprise follow.

Ever since the models shipped, somebody on your desk has been asking the same question:

Why can’t someone just vibe code this? Why would anyone pay for it?

And you’ve got the rebuttal ready. The switching costs. The integrations with a hundred counterparties nobody outside the company can see. The years of embedded process knowledge no language model reconstructs over a weekend. You’ve given that speech more than once.

Here’s the first test case.

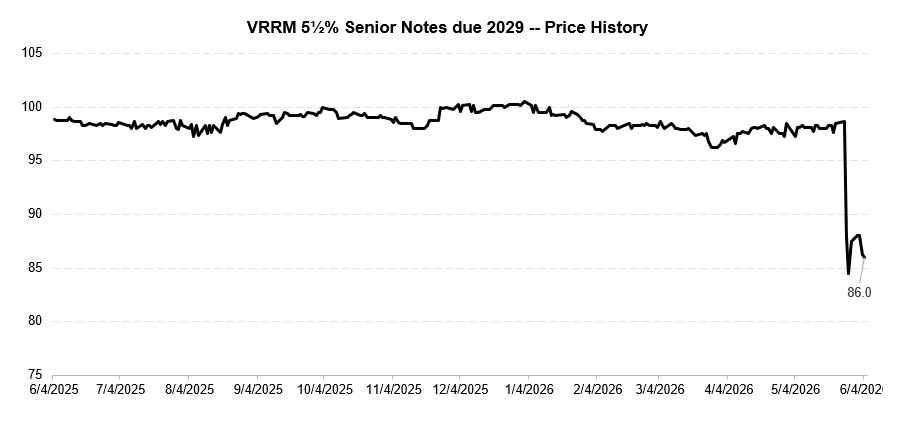

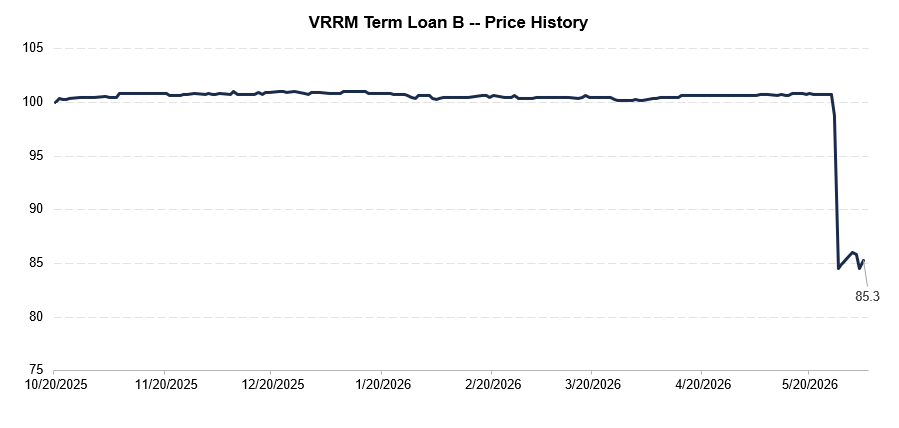

Avis has been a Verra Mobility customer for twenty years. In late May, it terminated the contract, effective September, and decided to run its tolling itself. Vibe coded, insourced, partnered out, nobody’s confirmed which. Doesn’t really matter. The stock fell 70%. The bonds gave up a dozen points, near par into the mid-80s.

And the bigger question isn’t even Avis. It’s the two customers still in the building. Hertz and Enterprise renew in 2027. If Avis can walk and do this itself, why can’t they?

The equity has already picked a side. It’s pricing all three gone. The credit hasn’t moved nearly as far, which means the two markets are looking at the same company and disagreeing about how this ends.

So is the selloff overdone, and if there’s a trade here, where in the cap stack does it sit?

Situation Overview

Verra Mobility is one of those businesses most people have interacted with without realizing it.

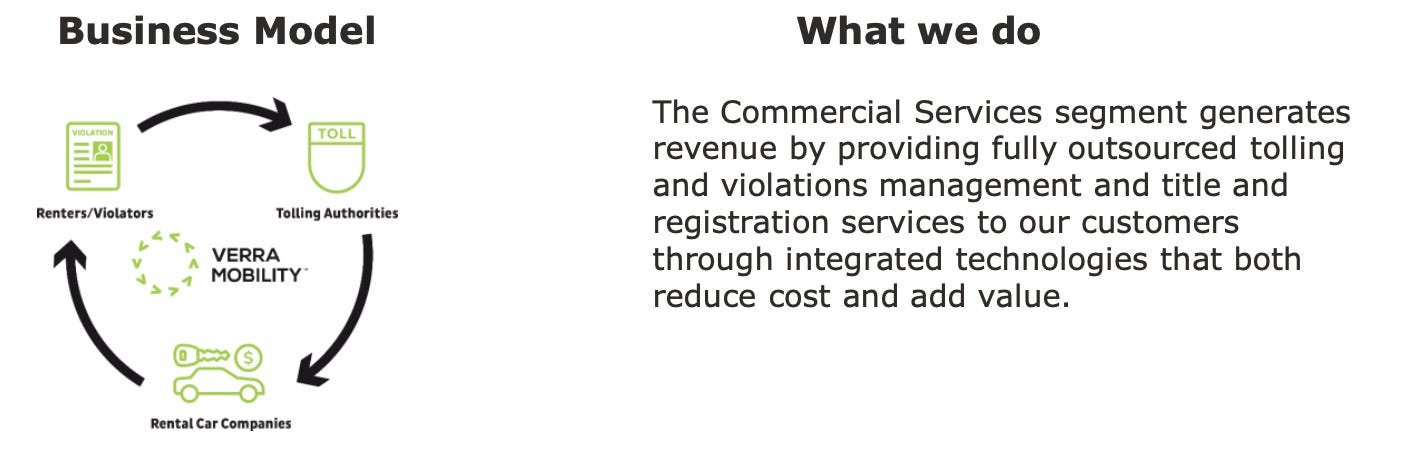

If you rent a car, drive through a toll, and later see a toll-related charge on your rental bill, there is a decent chance Verra was somewhere in the middle. The company helps rental car companies and fleet operators manage tolls, violations, billing, payments, and the administrative mess that comes with moving millions of vehicles across different toll roads and jurisdictions.

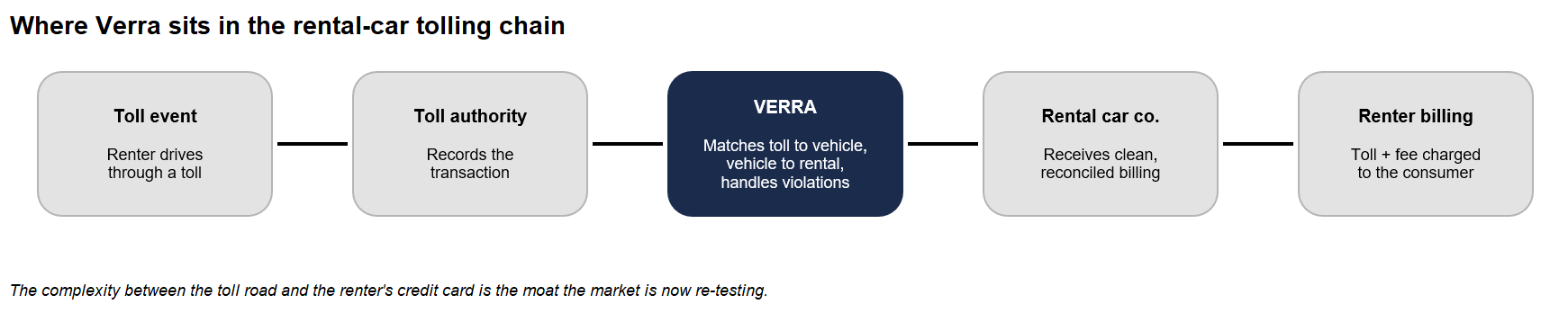

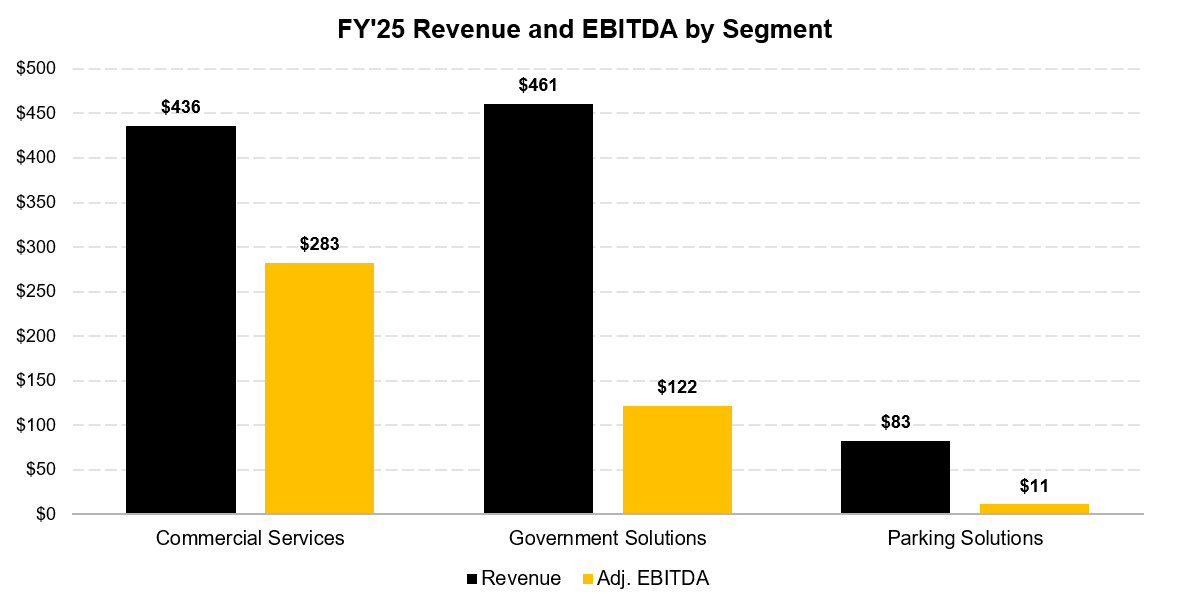

That is Commercial Services, the crown jewel. Verra matches a toll event to the right vehicle, the vehicle to the rental agreement, and the agreement to the renter, then runs the billing, collections, and dispute handling behind it. Unglamorous work, and harder to run than it sounds.

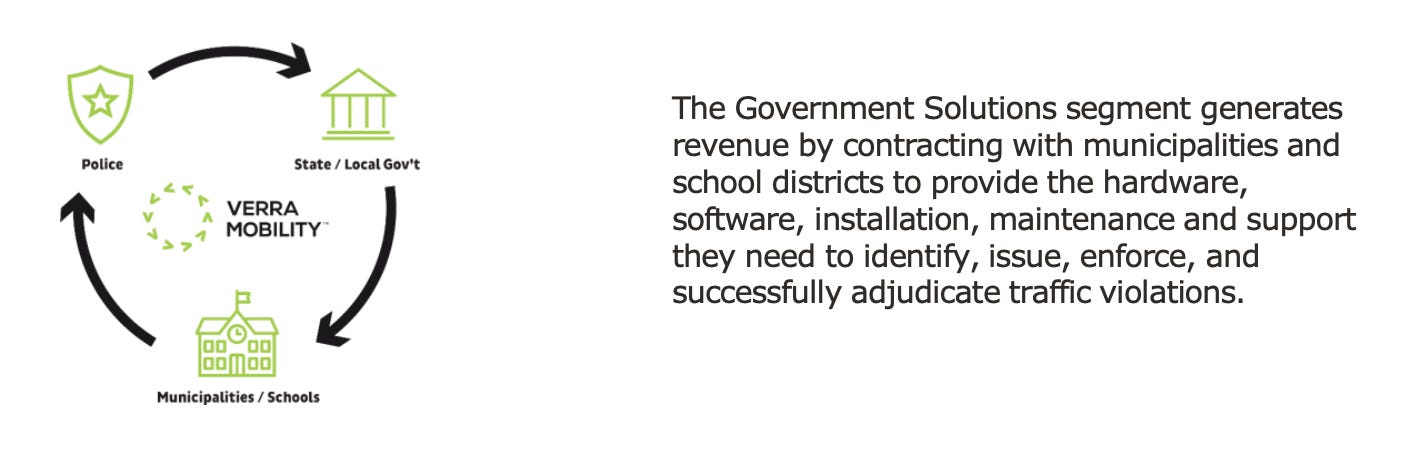

Government Solutions is the other real business: automated traffic enforcement for municipalities, the red-light and speed cameras, school-zone and bus-lane programs, anchored by New York City. Lower margin than Commercial Services, more exposed to politics and regulation, but sticky once the cameras are in the ground. Parking Solutions is small and not why anyone owns the stock, so set it aside.

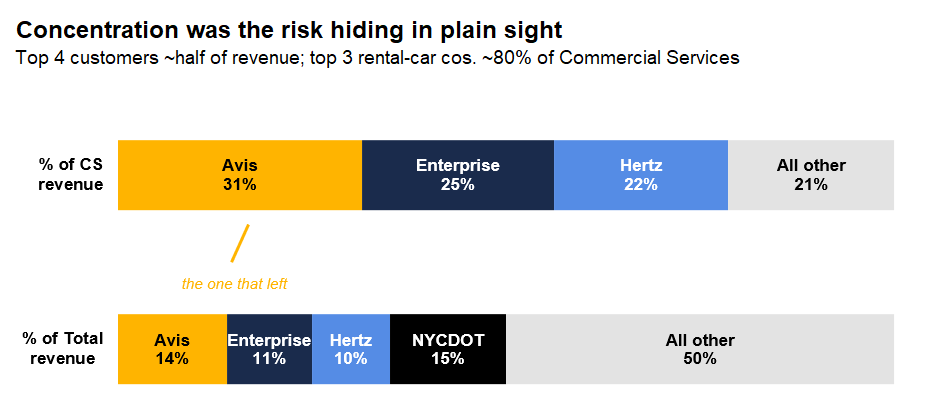

Before the recent drama, the Verra story was that this was a boring, high-margin, infrastructure-like business. Commercial Services was not the largest segment by revenue, but it was the profit engine. In FY’25, Commercial Services represented roughly 45% of revenue but nearly 70% of EBITDA. That margin profile is what made the company look decent.

The pitch was that Verra had built a platform too complex to replicate: a fragmented tolling landscape, consumer-level billing layered on top of fleet tolling, and years of plumbing into authorities nobody else had wired up. Investors treated that complexity as a moat.

Then Avis Budget terminated its contract.

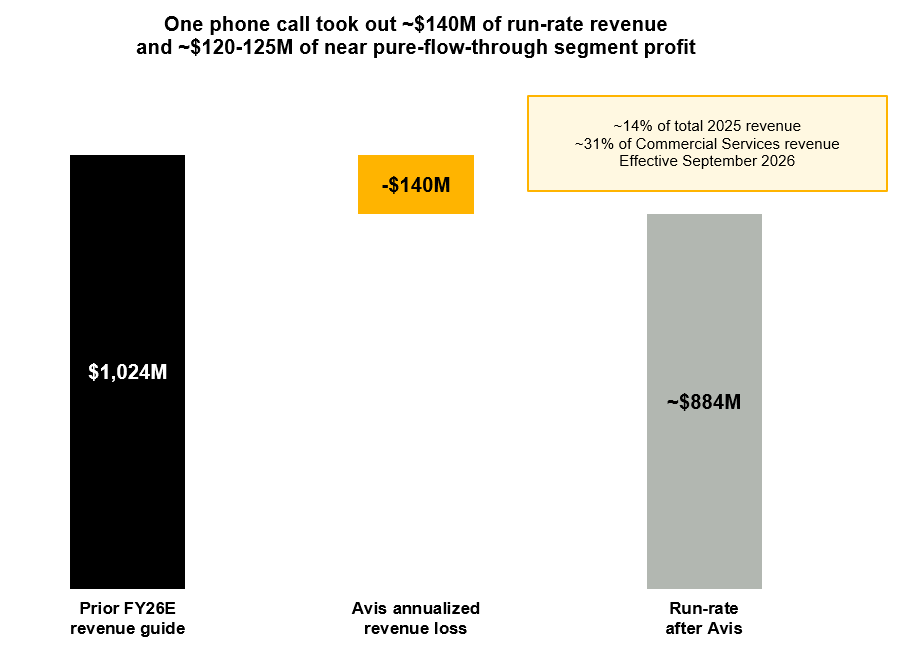

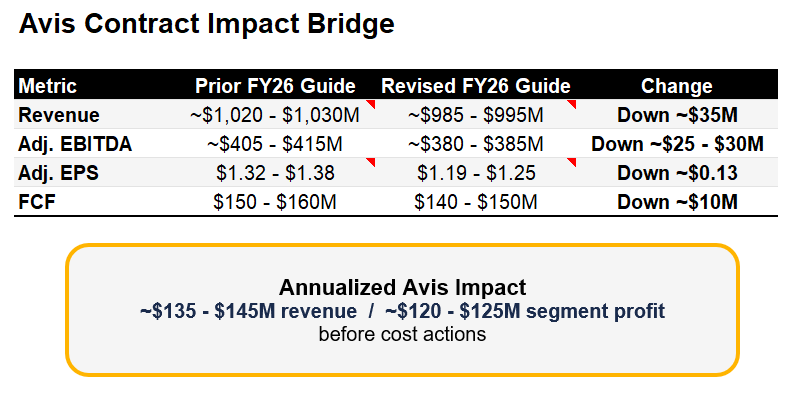

In late May, Verra announced that Avis had sent a termination notice effective September 2026, ending a relationship of almost twenty years. Management put the hit at roughly $135mm to $145mm of annualized Commercial Services revenue and $120mm to $125mm of segment profit, before any cost reductions.

The problem was never just the lost revenue. It was what Avis was saying about the business. If one of the three largest rental car companies thinks it can insource this, the next question writes itself: why not Hertz, why not Enterprise, both up for renewal in 2027.

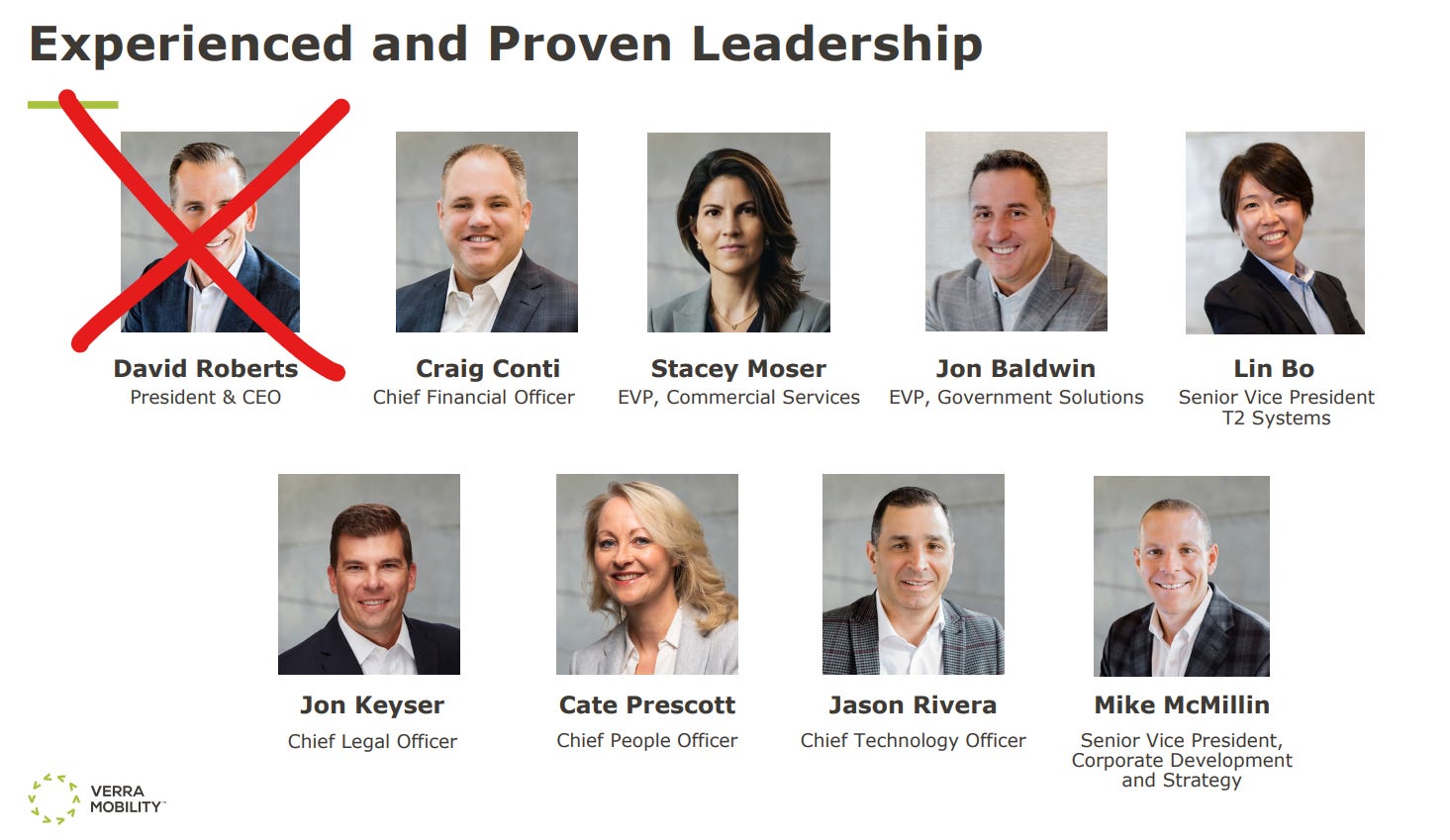

The reaction was brutal. The stock fell about 70%, the CEO stepped down a week later, and the credit stopped trading like a simple multiple reset.

The first-lien term loan dropped into the mid-80s. The 2029 notes sold off too. What the credit is pricing now is not the Avis earnings hit. It is the possibility that the highest-margin segment has been structurally impaired.

Two ways to read it. The bull read is that Avis is underestimating the work, hits billing errors and authority friction, and either crawls back or quietly proves the platform was worth paying for, in which case Hertz and Enterprise stay and the worst you get is harder pricing. The bear read is that Avis does not need a perfect clone, just a good-enough internal solution that keeps more of the economics for itself, and once that exists Hertz and Enterprise hold a much stronger hand and the old Commercial Services margin is gone for good.

Which one you believe is the whole call, and it is a credit question now, not an equity one. If the remaining customers stay, Verra is still a cash machine and the debt is money-good. If both eventually follow Avis, you are no longer valuing a premium tolling platform, you are valuing a lower-margin government enforcement business with a damaged commercial segment. That range of outcomes is wide enough that the equity and the credit have drifted apart, and that gap is where the trade lives.

Can Avis just vibe-code this?

This is the question the whole selloff hinges on, so it is worth being precise about what Verra actually does.