Credit Weekly: The Right Tail Creditors Ignore

AMC, Hertz, Carvana. Now Avis. The industry keeps calling it luck.

Here’s an interesting situation you might’ve missed.

Going into March, Avis was a deteriorating but not yet broken credit. Net leverage around 7.5x. Negative FCF in 2025 of ~$700mm. Bonds widening but not distressed. A 2027 maturity and a management team in the middle of a turnaround that hadn’t yet shown results.

The 4Q print made it worse. EBITDA missed by $100mm+. DPU blew out to $338 against a sub-$300 guide. A $518mm impairment on the EV fleet. The 2026 guide came in $150mm below where anyone was modeling. The business had not stabilized and the credit trajectory was clearly lower, not higher.

That was the setup 8 weeks ago. Coming out of that print, the consensus framing was straightforward. Avis would be in trouble if things didn’t turn, and the turn wasn’t visible in the numbers.

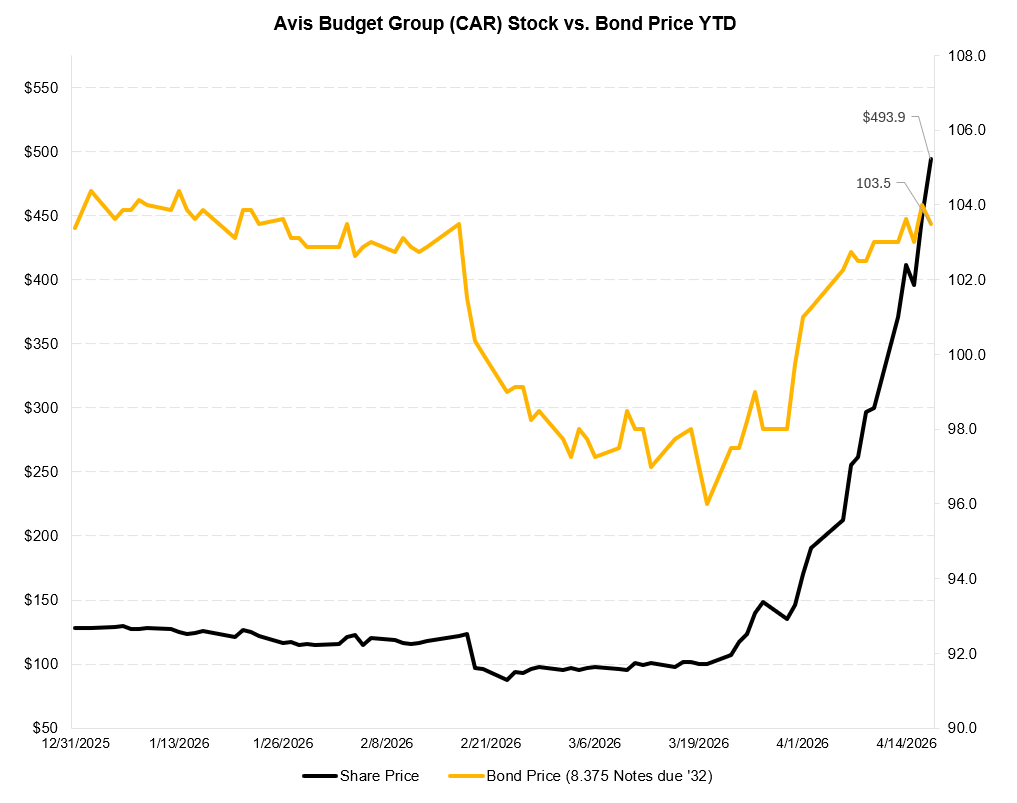

The stock is now up 300%+ from the March lows. The bonds have tightened materially. Management has filed an ATM shelf that’s about to take out most of the 2027 maturity wall through an equity raise. None of that was in the consensus credit model 8 weeks ago.

Worth walking through how we got here, because the answer isn’t a fundamental improvement.

What actually happened

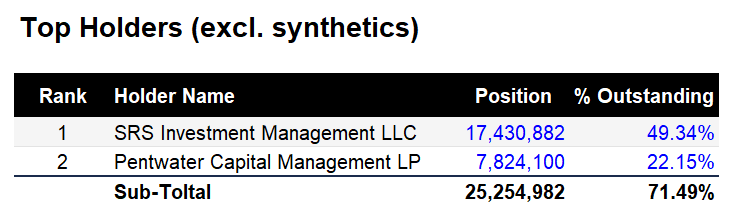

In late February, Pentwater Capital disclosed a 10% stake in Avis. An April Form 4 showed the direct stake had grown to 22%, plus synthetic exposure through cash-settled total return swaps. Combined with SRS Investment Management’s 49% position, two holders controlled over 70% of the shares directly, and more than 100% once the synthetics were layered in.

Short interest at 54% of the float. Section 16(b) kept the sellers on the sidelines. The squeeze math was visible in the filings by late March.

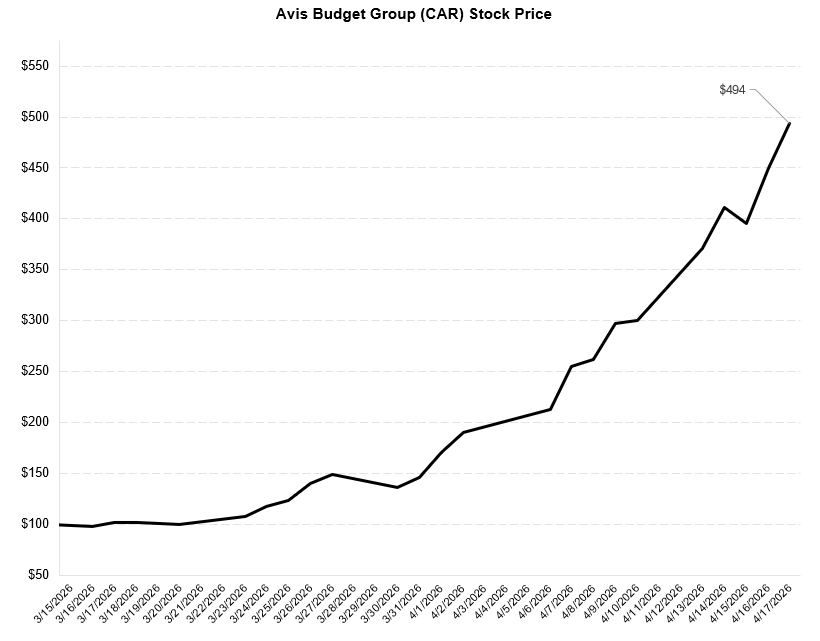

The stock roughly doubled from late February through early April on the ownership math alone, moving from around $97 to $190 before Iran escalated on April 7. Everything Avis did beyond the rental car tailwind was the squeeze.

A few things about the Iran conflict worth unpacking.

First, the domestic travel substitution. Americans who had planned European trips are expected to start rebooking domestically, which is supportive for airport rental car demand. Avis’s US business captures that directly. Not enormous in dollar terms, but directionally positive for 2Q and 3Q rental days and RPD.

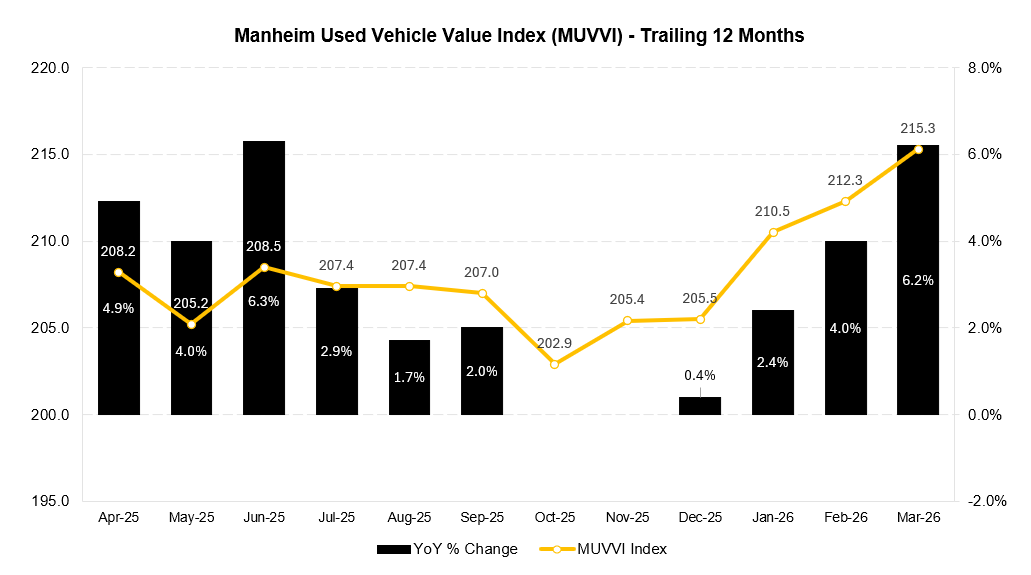

Second, the used car price channel. Crude up meaningfully pushes input costs higher on new vehicles, which supports used vehicle residuals and therefore Manheim. The March Manheim rental risk index was already up 6.2% y/y, the best since July 2023. Iran escalated that trend. For Avis, higher residuals flow through DPU, which is the single biggest line item on the rental car P&L. A sustained Manheim tailwind matters more than the rental day volume.

Third, the macro backdrop. The Iran ceasefire last week opened the HY primary market to its biggest week since September 2020. Stressed paper got bid aggressively. The window for a stressed issuer to execute an opportunistic equity raise is as open right now as it’s ever been.

Add it up and Iran is unambiguously good for Avis on the fundamentals. Rental days up modestly, DPU down modestly, risk appetite up meaningfully. But the fundamental improvement is maybe $100-200mm of EBITDA if the ceasefire holds, against 2026 guidance of $800mm-$1bn. Useful but not enough to fix a credit with 7.5x leverage and a 2027 wall.

The pattern is mechanical. Shorted company with concentrated ownership sees a technical squeeze. Iran adds a geopolitical tailwind that makes the equity move more durable. Retail attention compounds it. Market cap expands faster than fundamentals justify.

Management, paying attention and not being stupid, files an ATM shelf and drips equity into strength. A $500mm raise at current prices deleverages the company by 0.5-0.7x and takes out most of the 2027 wall. The recap happens quietly while the bonds follow along. From signal to potential recap, about 60 days.

What the credit profession actually misses

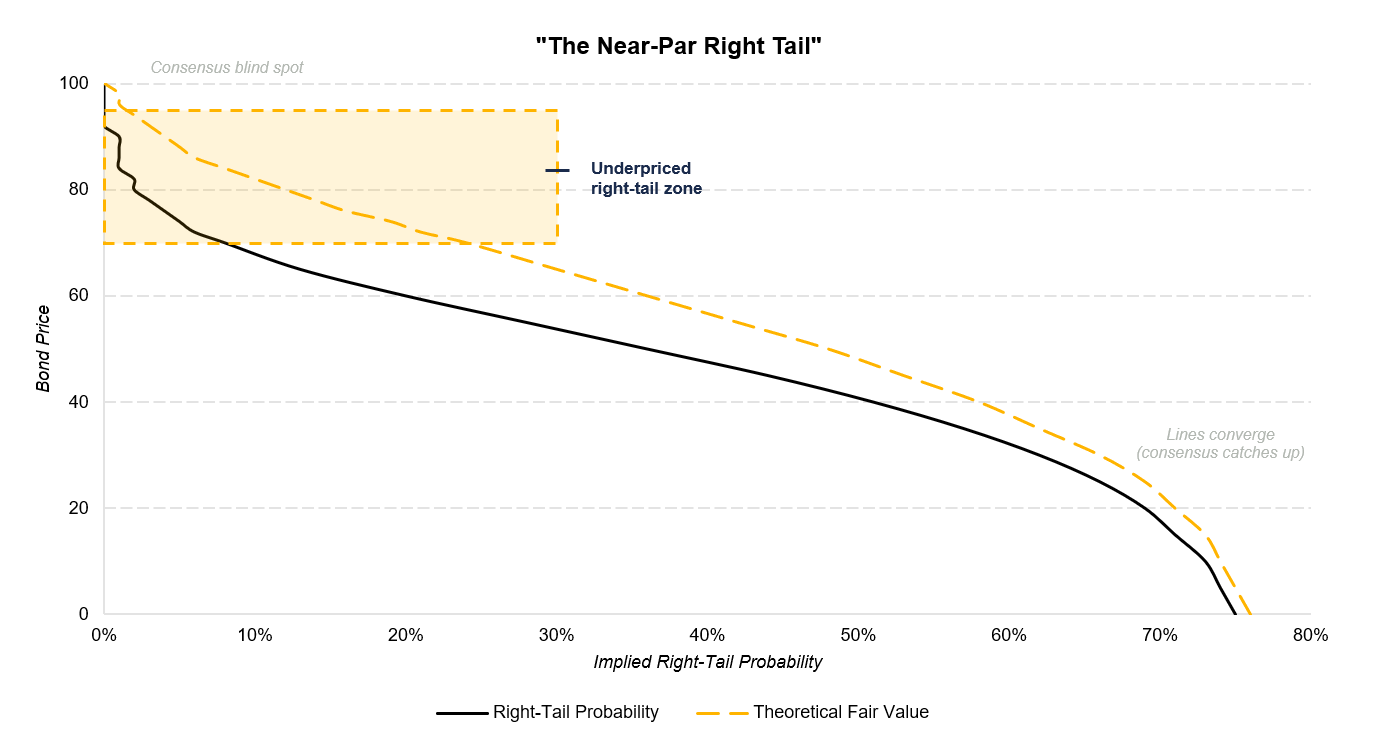

For credit investors, focusing on the left tail is absolutely a rational mindset. You’re buying something with capped upside, so most of the work is figuring out what can go wrong. Recovery math, covenant protection, refinancing risk. That’s the job, and for most credits it’s the right job.

Where the bias shows up is the right-tail probability, and it gets ignored more systematically the closer a bond trades to par. At 40 or 50, distressed investors are already running right-tail scenarios. They have to. That’s the job at that dollar price. At 85 and above, with the credit stressed but not yet distressed, the analyst is still running the near-par playbook. Downside scenarios get modeled. The right tail gets underweighted.

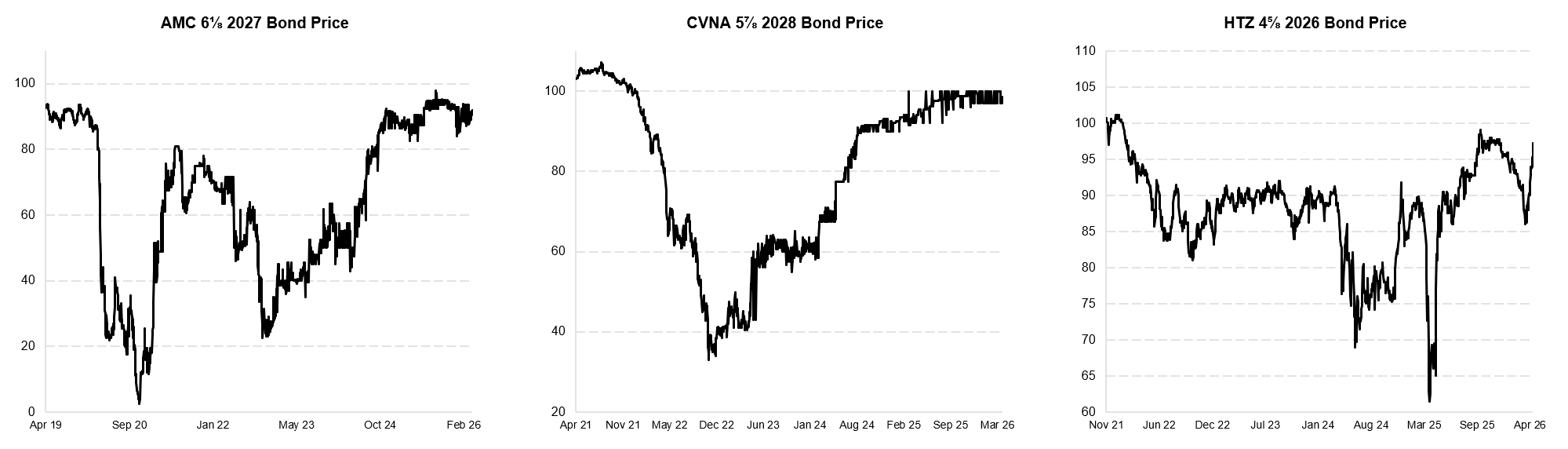

The mechanism isn’t new. AMC, Carvana, and Hertz each went through a version of it. Stressed public company sees an equity catalyst, management issues into strength through an ATM or follow-on, and the proceeds deleverage the balance sheet. The bondholders benefit directly. By the time these outcomes got priced, the bonds were already distressed. Nobody wrote the recap up as a scenario when those names were still stressed but not broken. The framework didn’t include “management opportunistically issues equity into a squeeze” as a path worth weighting until the bonds had already cratered.

Not theoretical zero weight. Actual zero weight. Sell-side recovery work on AMC unsecured in mid-2020 clustered well below par. Avis is different because the recap is happening while the bonds are still near par. Nobody wrote the ATM recap up as a scenario going into the 4Q print. Eight weeks later the bonds are pricing differently, and they never had to go through distress first.

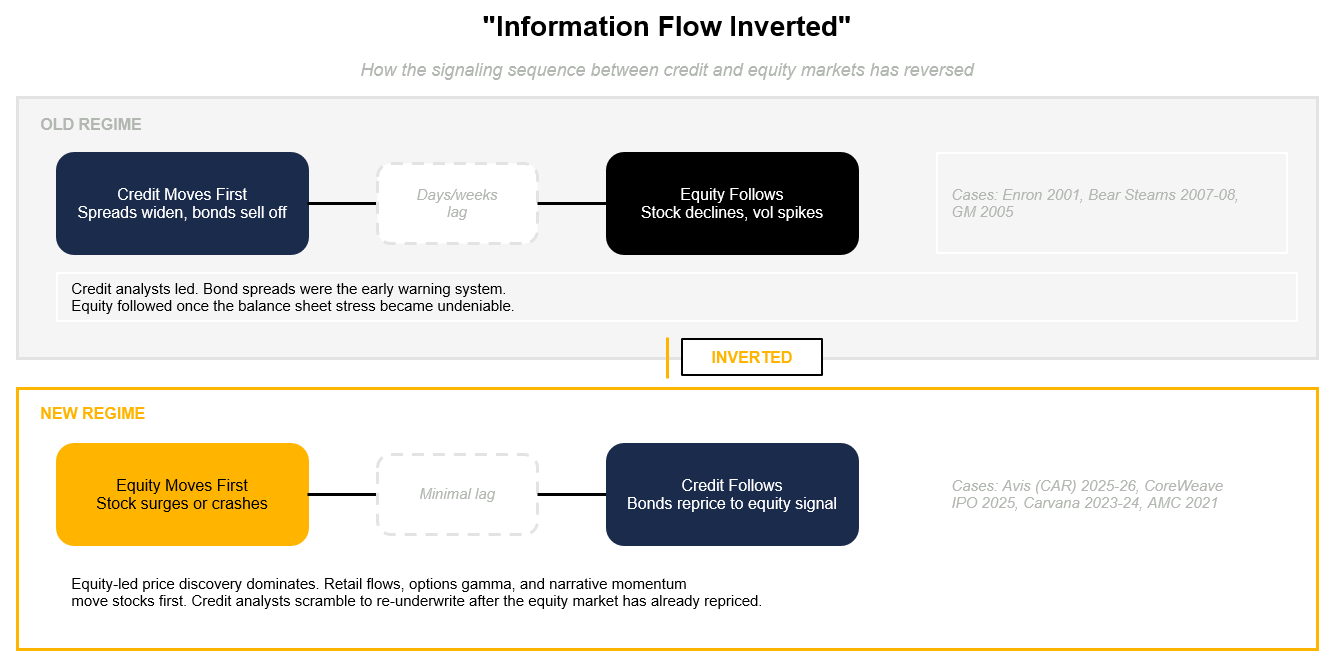

Equity leads, bonds follow

There’s a broader observation sitting underneath the Avis case.

Credit used to be the smart money. The discipline was built on doing careful work on the cap structure, the docs, and the recovery waterfall, and getting paid for that work because equity people weren’t doing it. Bonds moved first. Equity followed.

For many public credits, that has inverted. Equity moves first. Bonds follow. The variables determining the outcome are often equity-market variables. Float, short interest, insider lockups, retail flows, management willingness to issue into strength. The credit analyst modeling DPU and leverage is doing real work, but the work isn’t sufficient when the outcome is being set in equity markets.

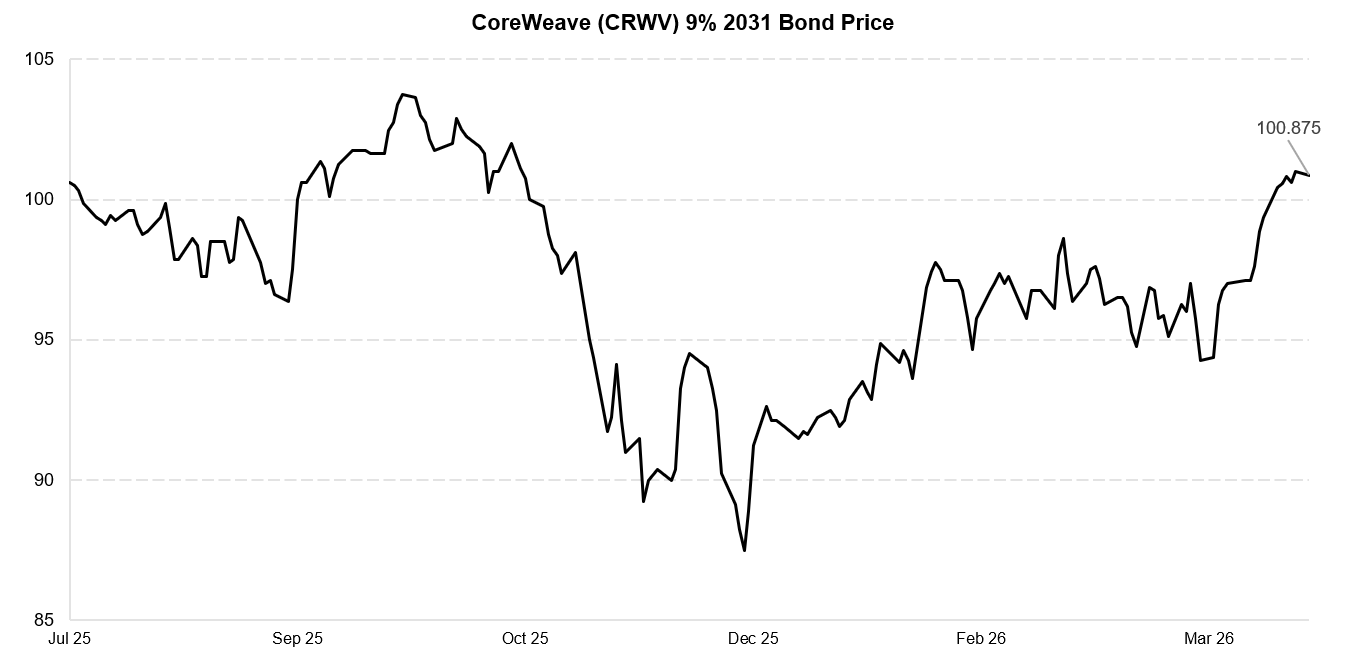

AI datacenters are the cleanest current example outside the Avis pattern. The subsector of HY is massively outperforming the broader index YTD. CoreWeave’s 9% ‘31s are up almost 4 points in two weeks on no meaningful change in credit fundamentals. What changed is the equity narrative around AI capex and hyperscaler counterparties. The credit followed the equity.

That inversion doesn’t typically apply to IG or most of performing HY credit. But for a subset of public credits, equity is the leading indicator and credit is the price-taker. That’s a meaningful change in how information moves between markets, and it has consequences for where analytical effort actually produces edge.

The market this week

The same split shows up in this week’s tape. A primary market running hot for risk-on paper, left-tail names still grinding lower, and the biggest single-name moves sitting in distressed credits that got repriced on non-fundamental catalysts.

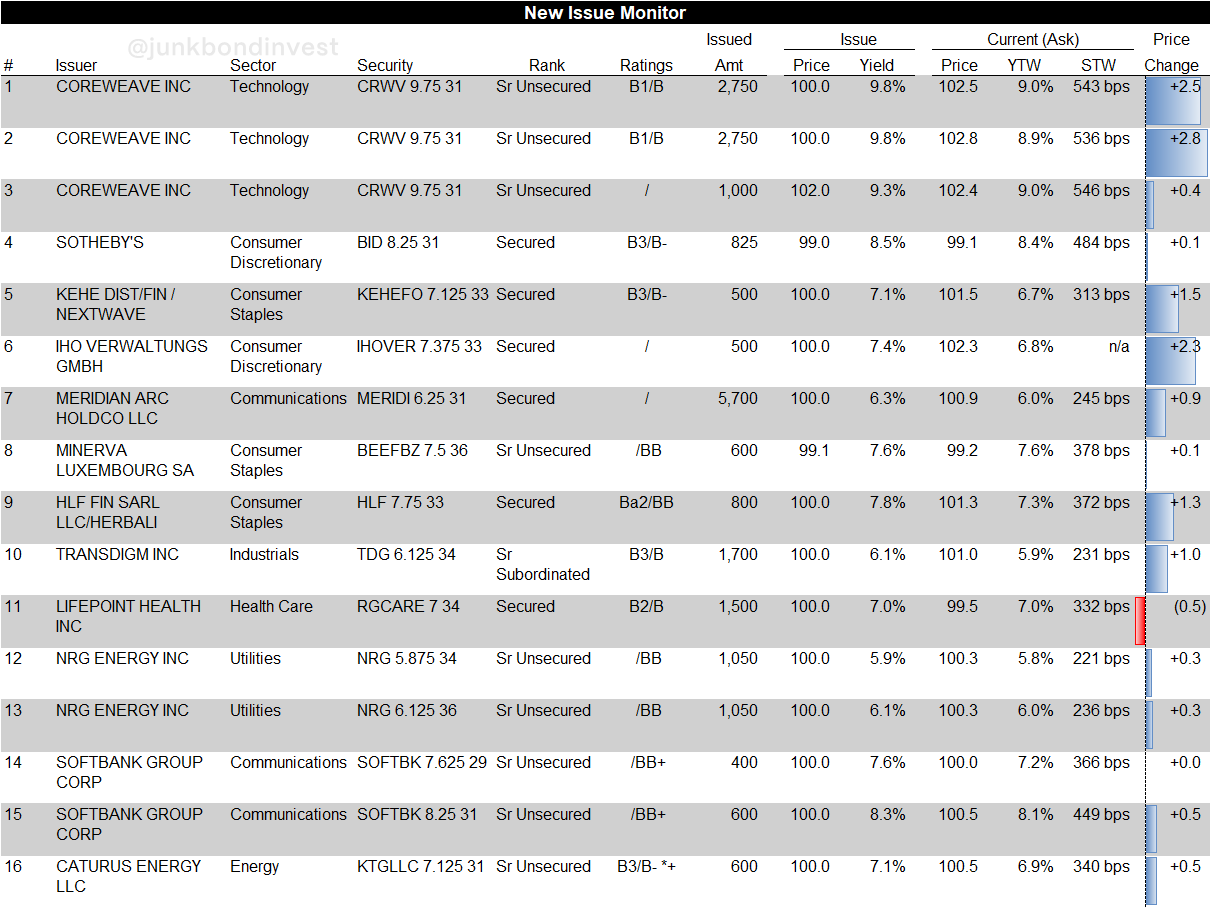

HY primary printed $16.5bn across 16 tranches. Biggest week in the last 2 years. Meridian Arc’s $5.7bn AI data center deal was the largest AI-driven HY print on record. CCCs led gains. 2026 supply on pace to be up 25% year-over-year. The Iran ceasefire opened a window and stressed paper got bid aggressively.

The primary pipe is telling you risk appetite is back. Meridian Arc clearing at 6.25% secured. CoreWeave printing a $1bn add-on on top of last week’s deal. SoftBank tapping for OpenAI funding. Sealed Air pricing $1.85bn in 8.25% ‘33s. LifePoint Health upsizing to $1.5bn at 7%. These are issuers accessing a market that was half-shut a month ago.

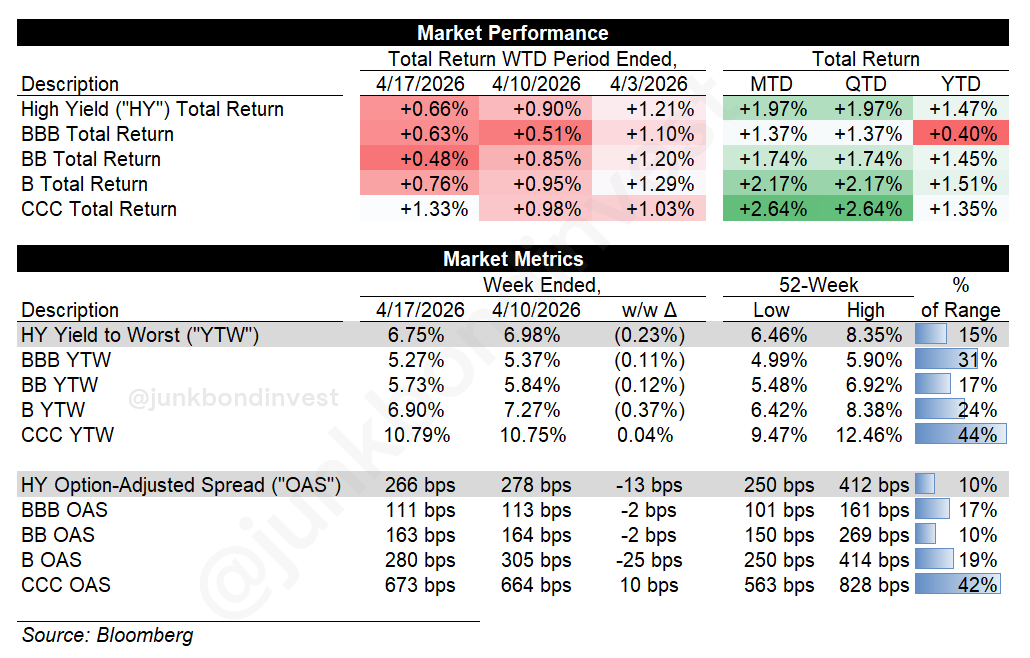

Meanwhile, high yield rallied 66bps last week with B spreads tightening through the week. At 266bps, HY spreads are at their 10th percentile over the last year. Inflows also totaled ~$3bn into HY funds, the largest since June.

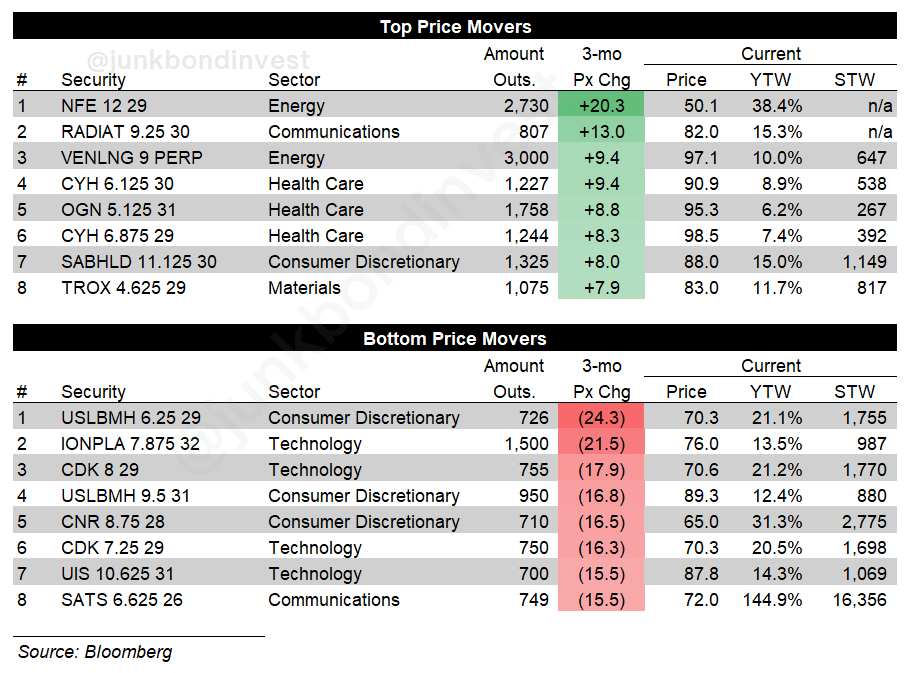

Underneath the rally, the 3-month bifurcation shows the entire picture. The top movers are stressed names getting repriced higher on technical or strategic catalysts. NFE up 20 points. Radiate up 13. Community Health up 9. Organon up almost 9 on the Sun Pharma bid.

The bottom movers are different stories entirely. US LBM down 24 on housing-market stress. CNR down 16. ION down 21 on AI displacement fears. CDK down 18 on the same. Software and housing, two sectors with the most distressed paper. See below for a few articles I’ve written on these topics.

What to do with this

You don’t need a dedicated right-tail strategy. Most of you running liquid credit books already have exposure to these types of situations, whether you’ve thought about them this way or not. The point is narrower.

When you’re looking at liquid bonds in a stressed public name, stop systematically underweighting the right tail, especially when the bonds are still closer to par than to distressed. That’s where the framework defaults to downside-only and the right tail quietly falls out.

And if it wasn’t obvious by now, equity-price moves can be a real driver of bond volatility regardless of fundamentals, both on the way up and the way down.

On the way up, that looks like what’s happening at Avis. A squeeze, an ATM, a recap that wasn’t in anyone’s model. On the way down, it’s the mirror: an equity narrative cracking before the credit metrics do, bonds repricing lower because the story changed rather than because the business did.

The AI datacenter names running on hyperscaler momentum are exposed to the same dynamic in reverse if the AI capex narrative shifts. Same mechanism, just a different direction. The credit analyst modeling Avis’s DPU and leverage going into the 4Q print was doing the right work. The analysis wasn’t wrong. It just wasn’t complete for a name where the equity-market variables were going to decide the outcome.

Being confidently short on the back of it was the mistake. The same kind of mistake is available on the long side in names where the equity is doing the lifting and the credit is along for the ride.

Weekly Bulletin Board

1) Wharton Online partnership

I recently partnered with Wharton Online and Wall Street Prep on their Restructuring and Distressed Investing Certificate Program. Relevant timing given the current market backdrop in software and building products. The program covers capital structure, bankruptcy mechanics, and distressed investing, led by practitioners at firms like Silver Point and Ropes & Gray. Code JUNKBOND gets you $300 off, with another $200 off if you enroll by May 11. Starts June 8.

Avis is just the latest reminder that equity‑market microstructure can rewrite the outcome faster than fundamentals can deteriorate