Liberty Energy ($LBRT): The Fracker Who Wants to Power the AI Boom

What Are You Actually Buying with the LBRT 0% Converts?

By now you know the AI infrastructure trade.

The hyperscalers are spending $600 billion+ on data center CapEx this year. The picks-and-shovels trade is crowded and priced. You know the names. The easy money is gone.

Meanwhile, a fracking contractor just tripled in the last 6 months.

Liberty Energy. Completion services. Cyclical, capital-intensive work that trades at 3-4x EBITDA because that’s what the market thinks it’s worth, and usually the market is right.

Then someone at Liberty looked at what they actually do. Run massive high-horsepower equipment in demanding field environments. Manage power under pressure, literally. And they made a call: those same skills could power an AI data center. Not metaphorically. Actually power it, with dedicated natural gas generation built and operated by people who already know how to keep equipment running where utility contractors would fail.

The question now: is this a real infrastructure pivot? Or a frac contractor that got ahead of itself?

What This Company Does

The frac business

Liberty Energy is the 2nd-largest fracking company in North America, with ~20% market share and ~40 active fleets operating across every major U.S. shale basin. When an O&G producer wants to extract hydrocarbons from shale rock, it needs to pump fluid into the earth at extremely high pressure to crack the rock open. Liberty shows up with the equipment, the crews, and the expertise to do it. The oil company owns the land and the oil. Liberty provides the service.

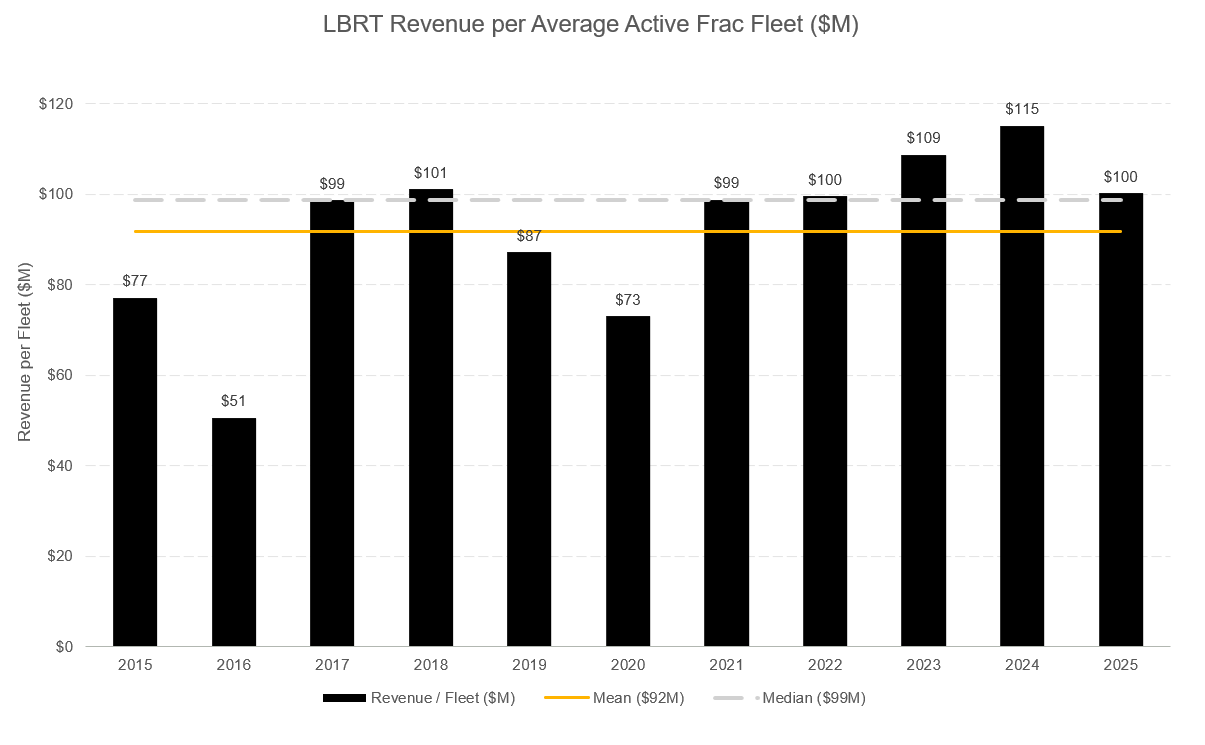

Revenue runs at roughly $100-120mm per active fleet annualized, implying a $4bn revenue base at peak activity levels. Costs are predominantly variable: natural gas or diesel fuel to run the pumping equipment, maintenance on a fleet of heavy machinery, labor for field crews, and proppant which is the sand pumped into the cracks to hold them open. Proppant largely passes through to the customer so it inflates the revenue line without contributing meaningfully to margin.

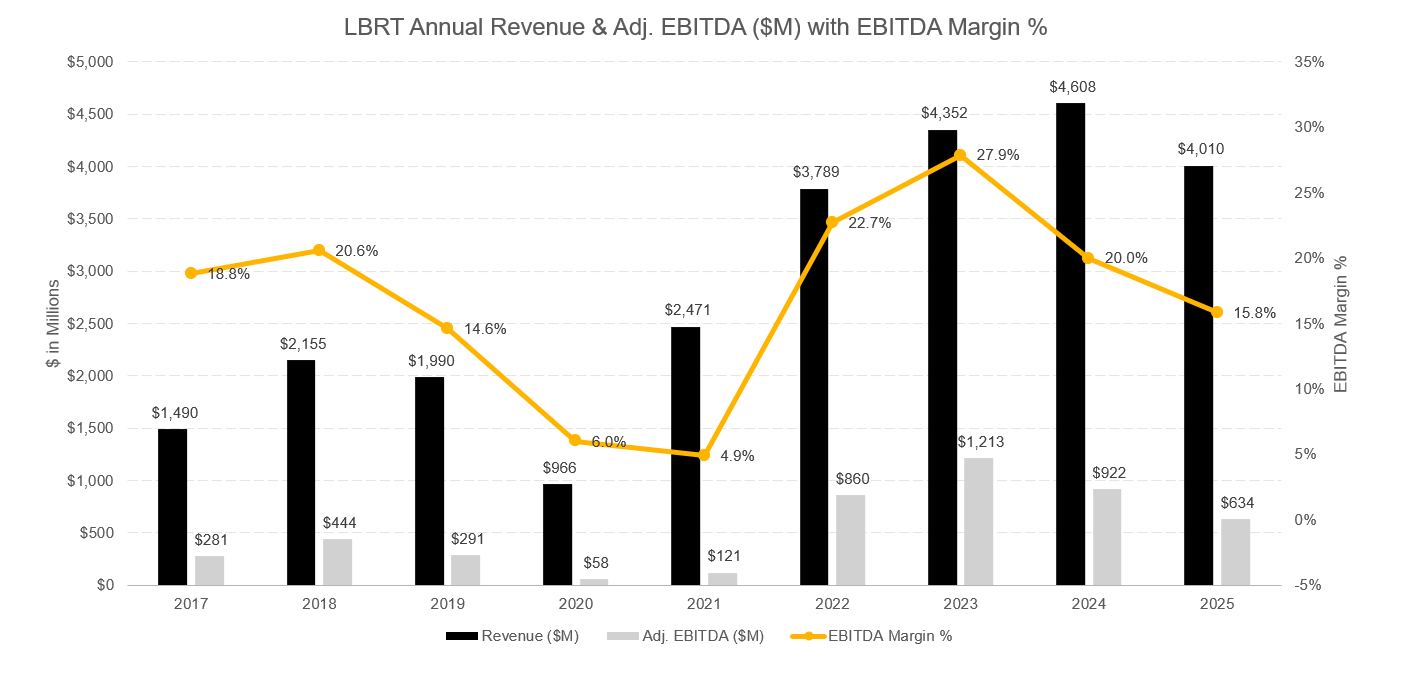

The margin profile is highly cyclical. At the 2023 peak, with WTI above $75 and frac supply tight, EBITDA margins ran 25-26%. At the current trough they are running 13-15%. Mid-cycle normalized is probably 18-20%.

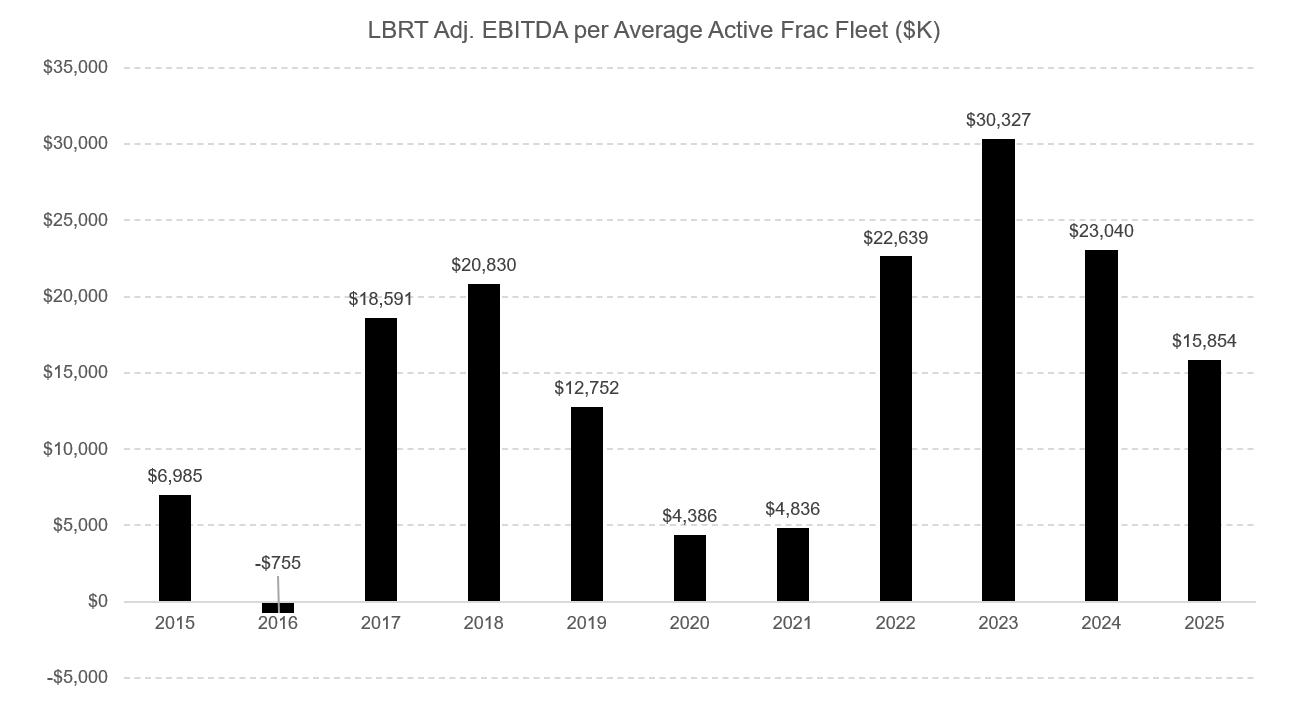

When activity recovers and fleets reactivate, fixed costs get absorbed across a larger revenue base and incremental EBITDA margins can run 40-60% on the way up. EBITDA per active fleet went from $4mm annualized in 2020 to $31mm in 2023 on a relatively modest increase in fleet count.

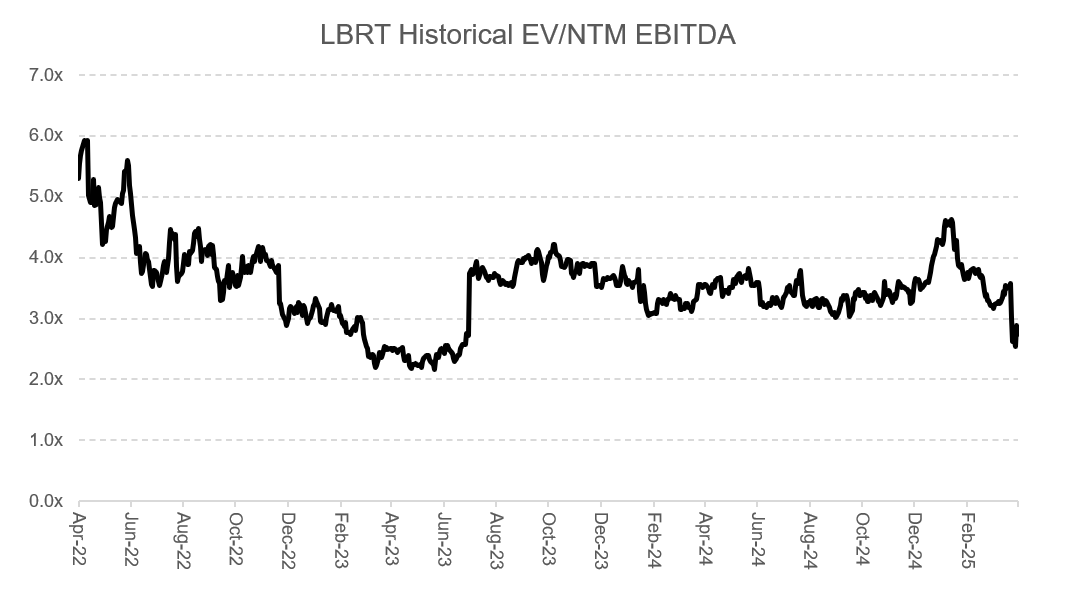

Over 8 years as a public company, LBRT 0.00%↑’s median EV/EBITDA has been roughly 3-4x regardless of execution quality. The ceiling is structural, tied to the cyclicality of the underlying business, and it is the core strategic problem the second business is trying to solve.

The power business

Fracking is the old business. The new business is power.

If you’re unfamiliar with the current industry setup, the current AI buildout is increasingly creating a power crisis. A single large AI data center can require 100-500MW of continuous power and the U.S. grid was not built for this. Interconnection queues now stretch more than 4 years in most major markets. Traditional utility-scale power development takes 7 to 10 years from conception.

Hyperscalers cannot wait.

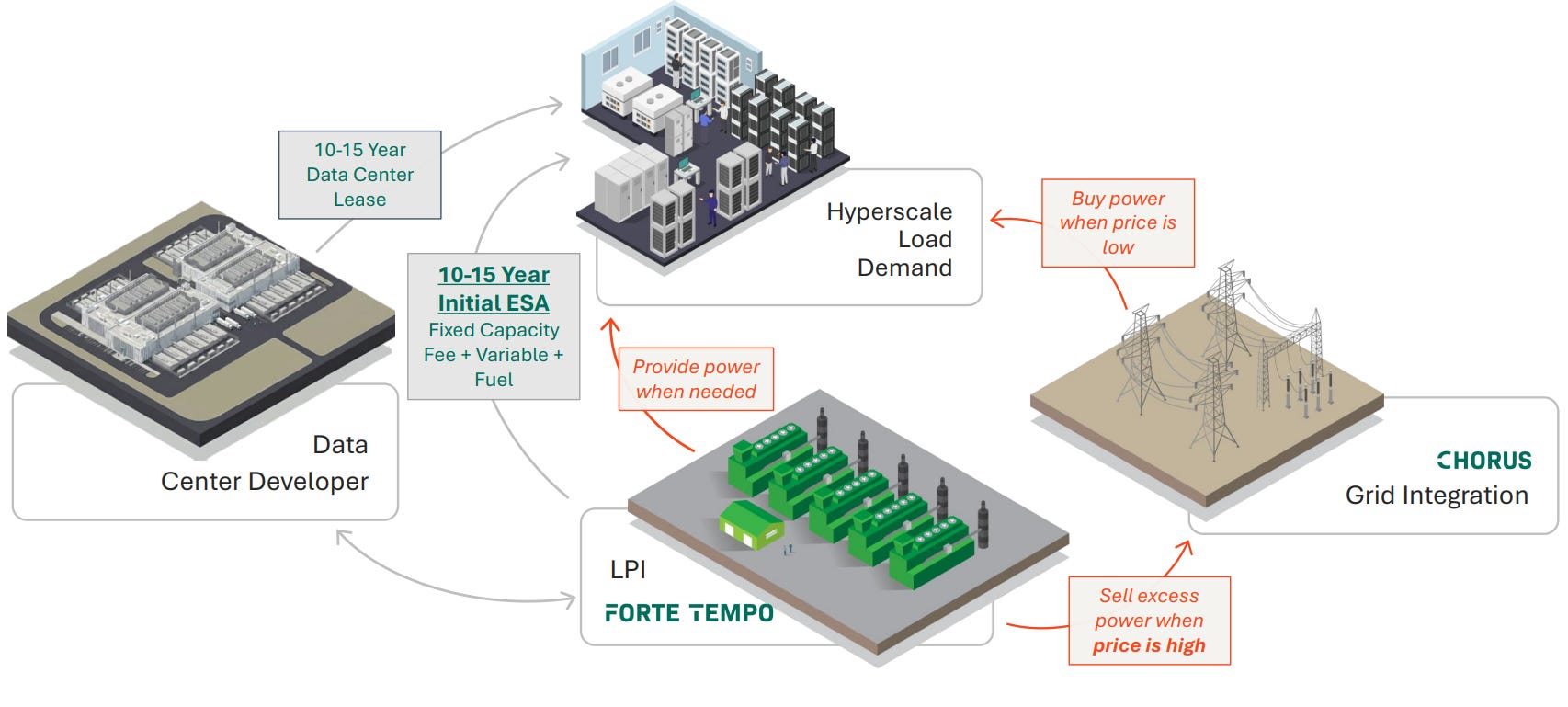

The solution many are turning to is behind-the-meter (BTM) power. Rather than connecting to the public grid, a data center installs its own dedicated generation on-site. The generator sits physically behind the utility meter, supplying power directly to the facility without touching the grid. No interconnection queue. No transmission constraints. Power available in months rather than years.

The economics are ~$300k of EBITDA per MW per year on $1.5mm per MW of all-in capex, implying roughly a 5-year cash payback and high-teens unlevered returns. At 1 GW fully deployed, that is $300mm of annual EBITDA. At the 3 GW, management is targeting by 2029, it is $900mm.

Margins at steady state run somewhere around 40-50% EBITDA. Once an asset is built and contracted, revenue is predictable and the primary variable cost is fuel, which in many contract structures passes through to the customer.

In early 2026, the commercial proof points arrived. A 1 GW power development agreement with Vantage Data Centers, including a firm reservation for 400MW of 2027 capacity. Then a 330MW preliminary ESA with an unnamed Texas developer (although this was recently cancelled). Management raised its capacity target to 3 GW deployed by 2029, up from 1 GW six months prior.

Why BTM Has More Duration Than It Looks

The bull case on BTM power rests on two arguments that are related but distinct, and it matters which one you believe because they have different shelf lives.