Credit Weekly: Who Buys It Next?

The downgrade is not the event. The handoff is.

There are two questions every credit investor should ask before making a new investment: who owns this paper and who would buy it if they needed to sell?

The answer often matters more than leverage, price, or all-in yield, and almost nobody focuses on it.

Credit markets have always worked this way. Different cohorts hold paper under different rules. Different rules mean different prices when paper has to move between them. The handoff between buyer bases has always been where price discovery happens on stressed names.

What’s different right now is the degree. The buyer base is more fragmented than it used to be. Private credit and HY ETFs are both meaningfully larger than they were five years ago. Active managers are smaller. CLO reinvestment cohorts have shifted. The crossover IG bid has gotten more conditional. Several absorbers in the chain thinned at the same time, and the price gaps at each handoff have widened as a result.

The credit may have changed, but the degree to which that price discrimination gets expressed is much wider now. Dispersion grows the smaller and shallower the next buyer universe is.

Most market commentary works off the spread because that’s what’s visible. The headline gives you the index, the rating bucket, the sector. It doesn’t give you who actually owns the paper and what would happen if they had to sell. Spread levels are an output. The buyer base is the input.

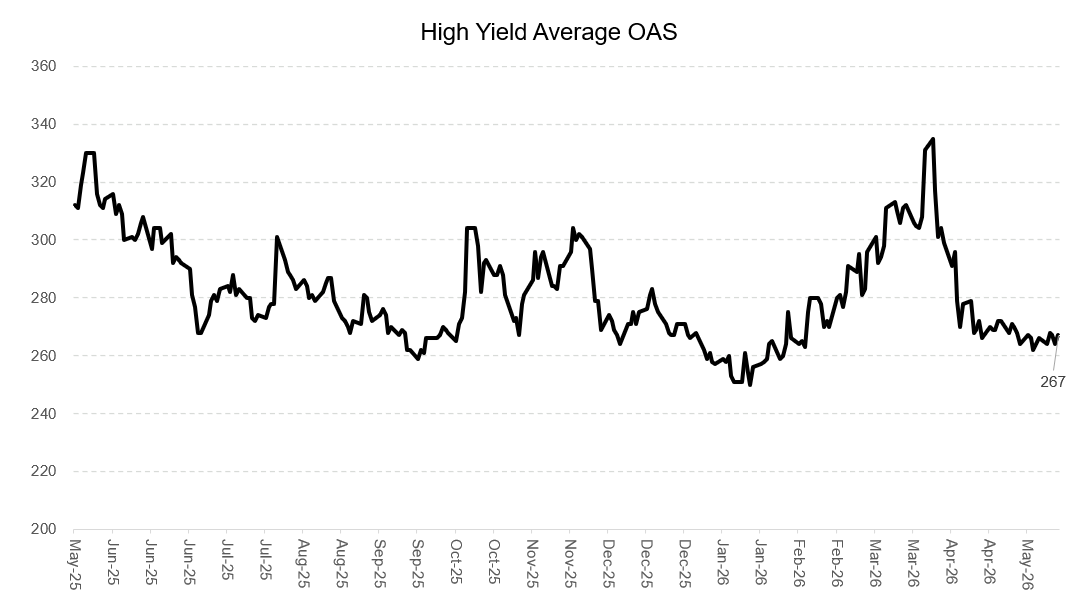

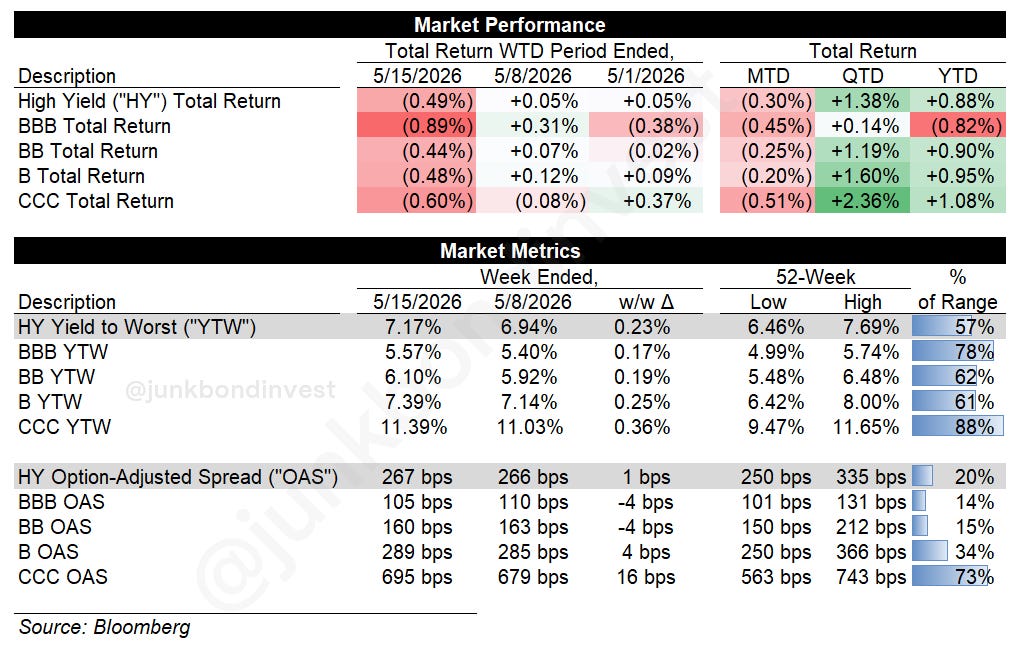

Today, HY spreads remain inside 300bps. The headline gives you nothing. What’s actually happening sits below it.

Where the price gap opens

Take a single-B loan trading in the mid-90s, owned mostly by CLOs in their reinvestment period. The CLO can hold it, add to it, reprice it. Spread reflects the underlying credit risk plus a modest liquidity premium. The buyer base is deep and sticky.

Downgrade it one notch. The company is still the business it was yesterday. Inside the CLO, the math changes. OC tests start mattering more. If the loan slips below par triggers or migrates closer to the CCC bucket, it begins to weigh on the structure rather than support it. Managers tight on their tests cannot easily add to it. Some need to trim. The largest natural buyer just got smaller.

The next bid is no longer the CLO at the same intensity. It is a credit hedge fund, a multi-strategy book, or a newer-vintage CLO with cushion to spare. Each requires a different price. The loan slips several points. The catalyst was the downgrade. The price gap was created by the owner base changing.

Downgrade it again. The CLO universe is largely out of the conversation. The natural buyers are distressed funds, opportunity funds, and the small set of credit hedge funds that specialize in this part of the market. The loan slips again. The business hasn’t always changed. The mandate that holds the paper has.

A handoff can produce significant price gaps that underlying fundamentals don’t dictate. The new owner base requires a different price to clear, and the gap between those prices is the dislocation. Sometimes that creates opportunity for buyers who can underwrite the next mandate before the old one fully exits. Sometimes it produces lumpy, choppy price action because there isn’t a natural buyer base at all.

Take broken converts for example. Once a convertible breaks, the equity option is too far out of the money for convert funds and the credit isn’t clean enough for HY managers. Neither side has a real reason to own it. Each fund type that might pick it up operates under its own restrictions, and many of the more flexible vehicles are too small to absorb size.

The depth of each buyer matters as much as whether one exists. A broken convert that nobody is forced to own and nobody is structurally set up to buy will trade where the most opportunistic capital wants it to trade, which is can be below where fundamentals would suggest. I wrote about this dynamic at DJT 0.00%↑ over the weekend:

The same logic runs in bonds. A BB owned by crossover IG buyers, total return funds, and indexed ETFs has a deep bid. Downgrade it and the crossover bid weakens. Total return funds may still hold it but the marginal buyer is a dedicated HY fund with different concentration limits. Another downgrade and dedicated HY funds become the only natural holders.

Each step is a handoff. Each handoff has a price.

Why the handoffs are harder now

The slack in the system has gotten thinner at every step.

CLOs in reinvestment used to absorb deteriorating paper as a matter of course. Active HY funds had inflows to deploy. Crossover IG could lean in when yields were attractive. Insurance had room. Private credit was growing fast enough to absorb risk the BSL market wasn’t pricing.

Most of that slack is gone.

The class of 2020 to 2022 CLOs has been rolling out of reinvestment. Once a CLO exits reinvestment, it stops being a buyer at the margin. It can sell discretionarily but it cannot grow into deteriorating risk the way it could before. The cohort that absorbed the last wave is no longer the cohort that can absorb the next one.

Active HY fund flows have been one-directional for months. The asset class has seen consecutive weekly inflows, but the composition matters. The incremental capital is heavily ETF-driven. Active loan funds continued the pattern of sustained outflows that has defined the year. ETFs buy the index in proportion to the index and don’t differentiate between credits that should be owned at current prices and credits that shouldn’t be. Active managers do, and active managers are losing capital. A growing share of the incremental HY bid is a passive vehicle that doesn’t care about handoffs.

The crossover IG bid is more conditional than it was a year ago. Conditional on rate cuts arriving, on the curve flattening, on IG yields staying low enough that reaching into BBs makes sense. With the curve now pricing more hike risk than cut risk, that condition is breaking.

Insurance demand for CLO senior tranches remains solid, but spread compression has limited how much new equity formation it can support. CLO equity returns have come down. New CLO issuance ex-refi has been running below last year’s pace. The supply of new CLO vehicles to absorb deteriorating loan paper has slowed.

Most large private credit platforms have hit their quarterly redemption caps this year. The platforms managing through it are doing so by selling their most liquid paper, often the BSL exposure held alongside the private loans. That selling lands back in the loan market as incremental supply at the wrong moment.

Every absorber in the chain has gotten thinner. The depth of each remaining buyer matters more in that setup, not less.

The rates story is the trigger

I’ve been saying for weeks that the macro setup is quietly building its own vulnerability and that the long duration universe is the wrong place to be sitting. Financial conditions easier than pre-conflict despite oil 50% higher. One year inflation swaps trading 75bps higher. The market pricing more growth and more inflation simultaneously and treating it as benign. Labor stabilizing into the same impulse. The Fed not pushing back. The reflation trade leaking into credit while most accounts hadn't repositioned for it.

This week the leak became visible.

CPI came in hot midweek. A global bond selloff hit Friday on UK gilt concerns and renewed inflation worries. OIS forwards now price 60% odds the Fed delivers a hike rather than a cut by December, a complete reversal from where the curve sat two months ago. Even with spreads flat, high yield returned -0.49% for the week driven by the move in base rates.

Crossover IG buyers are the most rate-sensitive cohort in the HY bid and have been a structural absorber for BBs through this cycle. Their willingness to reach into HY for yield depends on a forward curve that suggests rates are coming down. When the curve flips, the math changes. Crossover allocations get pulled back. The deep bid behind BBs gets thinner.

BBs at current spreads do not compensate for the crossover bid stepping back. The credit doesn’t have to deteriorate for BB spreads to widen. The owner base just has to change.

The same logic works down the stack. Higher base rates compress interest coverage on floating-rate borrowers. Loans that were comfortably in CLO portfolios start consuming OC test cushion. The structures that absorbed the original financing become marginal sellers. The handoff cascade starts at the top of the rating stack and works lower.

A higher-for-longer regime functions as a buyer base thesis. The cohorts that absorbed the last cycle were built around an assumption that rates would come down. They didn’t. They aren’t. The owner base will have to reorganize around that reality, and the price will reset at each step.

What this looks like in real names

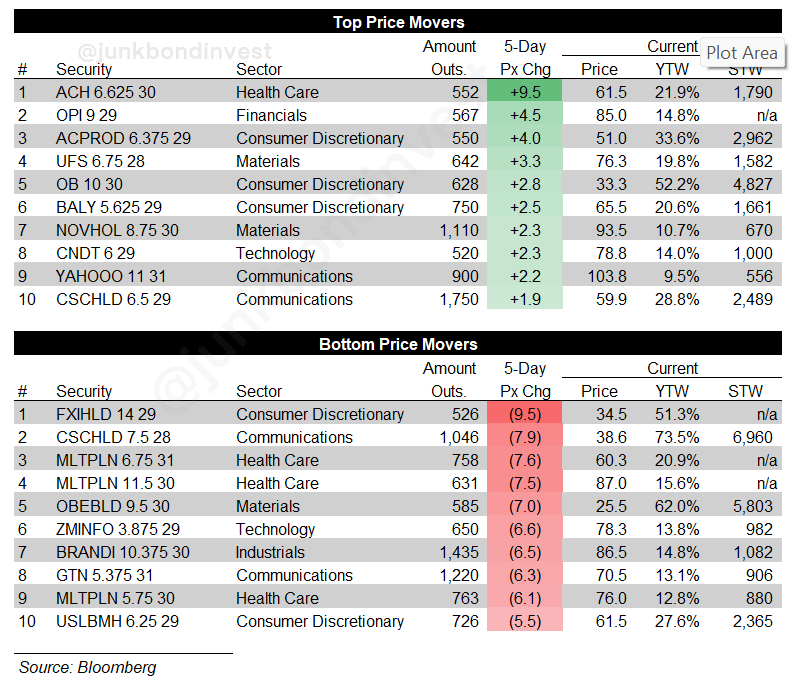

ZoomInfo is the cleanest example from last week. The company reported Q1, beat on both revenue and earnings, and cut full-year guidance. The bonds went from the mid-80s to a 78 context. Roughly 7 points lower on a quarter that beat. The existing holder base reassessed the terminal value and the next buyer required a different price. The handoff happened in one print. The 3.875% 2029s now yield close to 14%. The loans repriced to the mid-80s in parallel.

The same pattern shows up across building products, consumer cyclicals, business services, and the longer tail of sponsor-backed LBOs from the peak vintage. The single-B paper financed into the BSL market in 2020 to 2022 has been drifting lower for two years. Companies still current. Maturities still in the future. The loans trade where they trade because the buyer base that absorbed the original financing is no longer the buyer base that has to clear the secondary market.

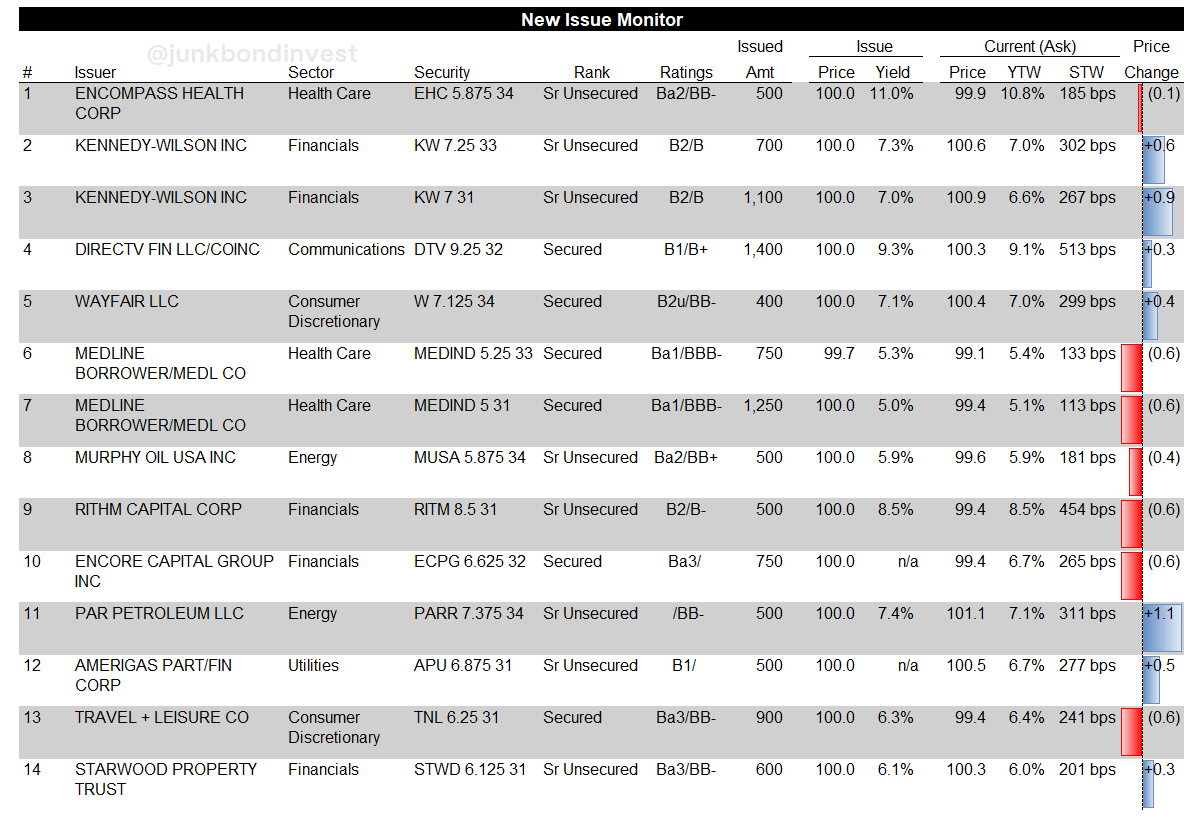

The primary market reinforces the divide. Clean deals for clean issuers cleared without trouble this week. DIRECTV priced $1.4 billion of secured notes at par to yield 9.25%. Wayfair priced $400 million of eight-year secured notes at 7.125%, tight to talk, and the deal triggered a Fitch upgrade on both the secured debt and corporate rating. Kennedy-Wilson placed $1.8 billion across two tranches to fund a take-private. Travel + Leisure cleared $900 million of secured notes at 6.25%.

Every one of those deals priced inside guidance or at the tight end. The natural buyer base for clean BB and strong single-B paper is intact. The handoff problem isn’t in primary. It’s in the names already outstanding where the existing holder base is being asked to keep holding through a setup it didn’t underwrite.

Things to be mindful of

A few questions worth running on the names you already own.

Who owns this paper today, and what are their constraints. What would have to happen for them to step back. Who is the next buyer if they do. What price does that buyer require to show up. How wide is the gap between the current holder and the next one. How deep is each successive buyer.

Work on the company itself still matters. Cash flow, leverage, maturity profile, business model, all of it. The marginal source of return increasingly sits in the handoffs between buyer bases. A credit priced for stability where the current holder is one bad print away from leaning back is the more dangerous setup than one already priced for a handoff.

The harder question is when the handoff happens without a rating change. A CLO manager looking at a weakening loan can choose to trim before the downgrade arrives. The buyer is another holder who hasn’t done the work yet. The price moves before the rating moves. By the time the agencies catch up, the loan has already changed hands and the price already reflects it.

The valuable work is spotting credits where the market will reorganize the ownership before the agencies do, where the current holder is fragile, and where the next mandate has different math than the current one.

A growing share of the incremental HY bid is ETF-driven, which means the bid in the index is firmer than the bid in any individual name. The index holds up while specific credits get punished. Dispersion keeps widening regardless of where the index trades.

The single-B handoff inside the loan market is where the largest price gaps live right now, and the post-reinvestment CLO cohort is worth watching as a driver of softer secondary bids in the back half of this year. The same credit can have a different secondary price depending on which CLOs own it.

JBI Bulletin Board

1) Now Hiring: Credit Analyst

I’m looking to bring on an experienced full-time credit analyst (ideally distressed background). At least a couple of years covering the space, buy-side experience strongly preferred. Software or building products coverage. You should know the names, know the docs, and the playbooks. If you’re interested or know someone who fits, reach out with a brief note on your background.