13% Yield to Put: Trump Media & Technology's ($DJT) Busted Converts

Bitcoin collateral, a $1bn par put in November, and a potential negotiated outcome

What yields 13% in May 2026?

Usually, something broken. A building products loan to a company missing numbers. A software credit where the equity cushion disappeared years ago. A capital structure where everyone knows the next negotiation is going to be unpleasant.

Not usually a secured convertible note with a par put six months away where the current president is the largest shareholder.

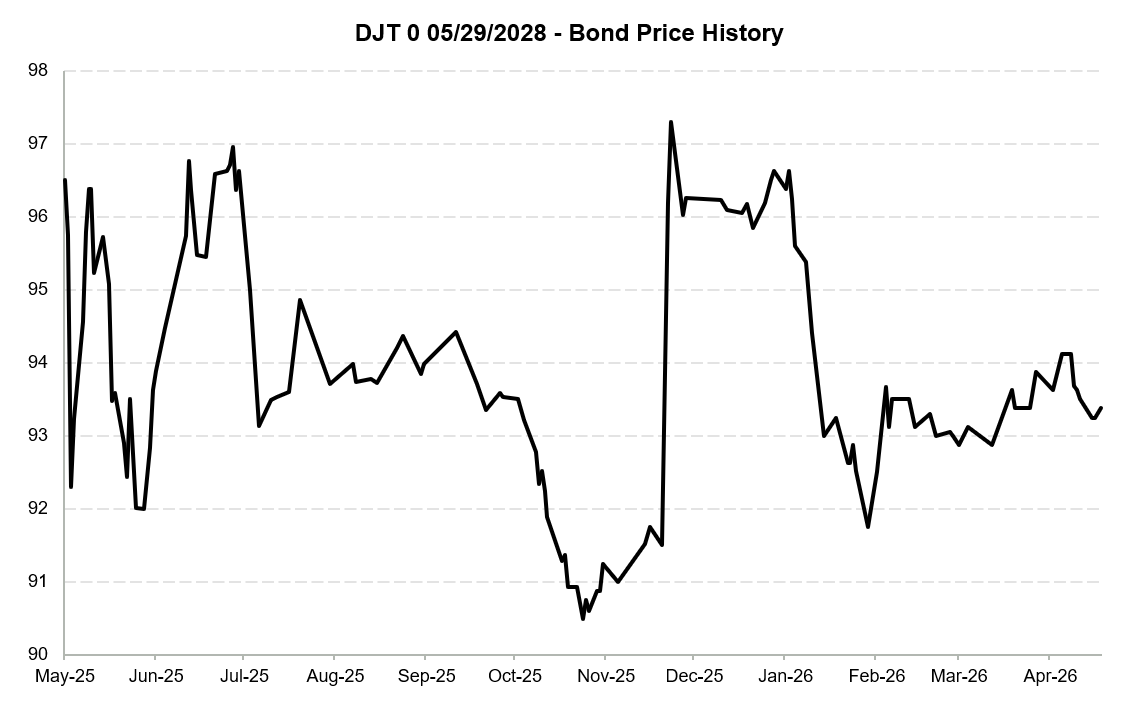

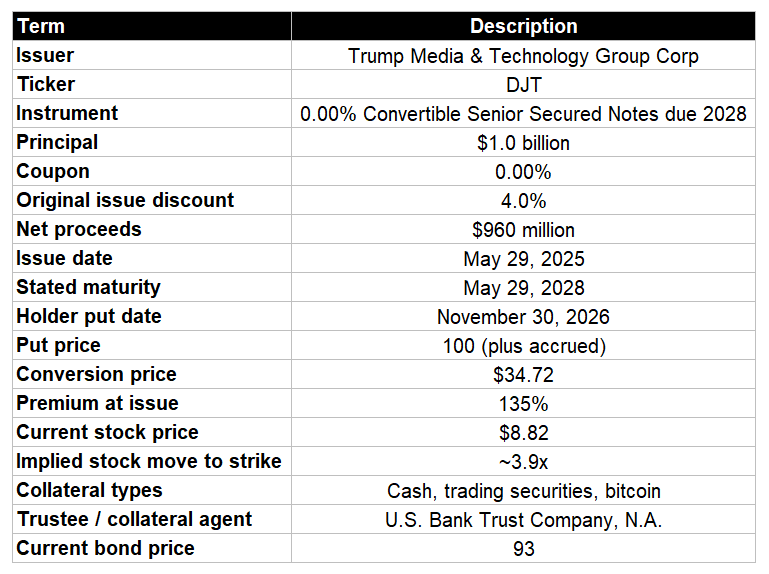

DJT 0.00%↑ has a $1bn zero-coupon convertible bond trading at 93, with roughly $2.4 billion of market cap beneath it. The stock is at $8.82, the conversion price is $34.72, so the equity option is dead. That part barely matters.

The notes are senior secured. The collateral package includes cash, bitcoin, and equity securities. Holders can put the notes back to the company at par on November 30, 2026. The trade is seven points to par in six months, roughly 13% annualized, on paper that looks secured and short-dated.

So why is it not trading at 98 or 99?

Because the pledged collateral does not cover the claim. The liquid balance sheet can cover the put, but only if management chooses to monetize it. The indenture leaves room for a negotiated refinancing. And the largest economic owner on the other side of the table is the sitting President of the United States.

The Setup

Trump Media and Technology Group is the parent of Truth Social and Truth+. It came public through a SPAC merger in March 2024. The operating business is barely a business: 1Q’26 revenue of $871,200, FY’25 revenue under $4mm, segment EBITDA negative. The operating business is irrelevant to the recovery analysis.

DJT is better understood as a capital markets vehicle wrapped around a brand. In May 2025, the company raised $2.4bn in a single private placement: $1.4bn of common at $25.72 and $1bn of 0.00% convertible senior secured notes due 2028. Proceeds went into a bitcoin treasury, a digital-asset-linked equity securities book, and strategic bets including a $200mm convertible note to TAE ahead of the pending fusion merger.

The indenture uses a loan-to-collateral ratio to govern how much collateral has to remain in the box and when releases occur: cash gets full credit, bitcoin gets only 52.6% credit, and collateral releases mechanically as principal pays down (first at $500mm outstanding, then at $250mm, then at payoff).

This is not normal convert paper. It is zero-coupon, secured paper with no current income, a dead equity option, and a first-priority claim on a volatile but real pile of liquid assets. The closest analog is not other converts. It is short-dated secured paper trading on collateral coverage, liquidity, and event timing.

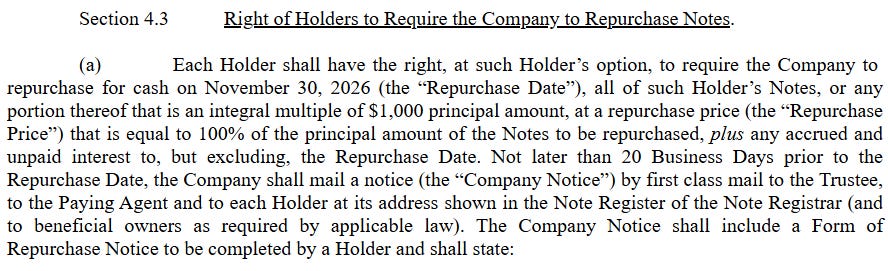

The put is what makes it interesting. Stated maturity is May 29, 2028, but every holder has a one-time individual right to require DJT to repurchase its notes for cash on November 30, 2026, at par plus accrued. No consent threshold. No majority vote. Each holder decides on its own. If a holder validly puts, the company owes par in cash.

That put should cap the bond near par into November, absent a revived equity option or technical dislocation. The only question is whether DJT pays in cash, refinances the notes, or pushes holders into a negotiated exchange due to doc flexibility.

What Assets Does the Company Own?

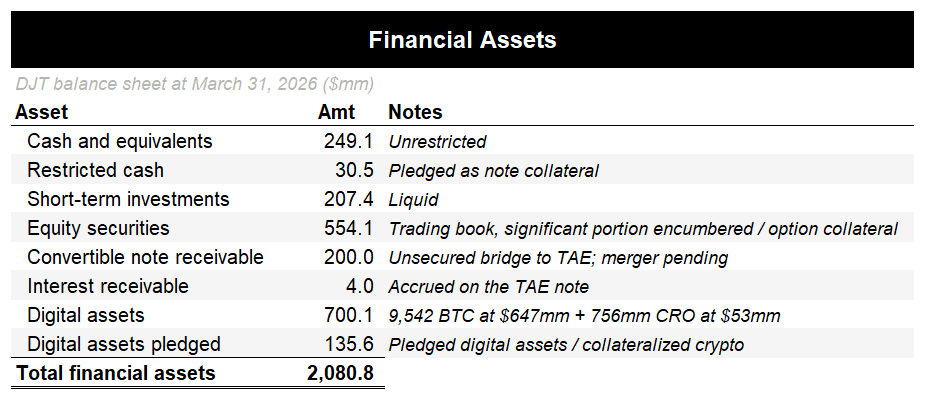

DJT closed 1Q’26 with ~$2.1bn of financial assets. Headline coverage looks comfortable but there are important nuances.

Cash and short-term investments together are $487mm. That is what DJT can write a check from on November 30 without selling anything illiquid or waiting on a transaction. Less than half the amount.

The $554mm equity securities book is the next piece, but it is not clean cash. DJT discloses $269mm of equity securities serving as collateral for the converts, and separately discloses $439mm of equity securities held as collateral for outstanding call options at 3/31/26. The overlap between those two figures is not entirely clear from the filing, but the conclusion is straightforward: the equity book is marketable, but not freely available dollar-for-dollar. Monetizing it ahead of the put may require unwinding, substituting, or restructuring collateral tied to the derivative overlay and the note collateral package.

The $200mm TAE convertible note receivable (and corresponding interest receivable) is unsecured paper on a private fusion company tied to a merger that has not closed. This may not be a source of cash on November 30 even though the merger is supposed to close mid-26.

Bitcoin is where it gets interesting. DJT held 9,542 BTC at quarter-end against a $1.13bn cost basis, so the digital asset book is sitting on ~$480mm of unrealized losses. Of those coins, 4,261 are pledged to the converts. Another 2,000 are posted with the covered call counterparty to hedge 4,000 BTC of exposure. The covered call piece is not permanent: those options expire in June 2026, well before the put. Unless rolled, 2,000 BTC frees up before November and becomes available.

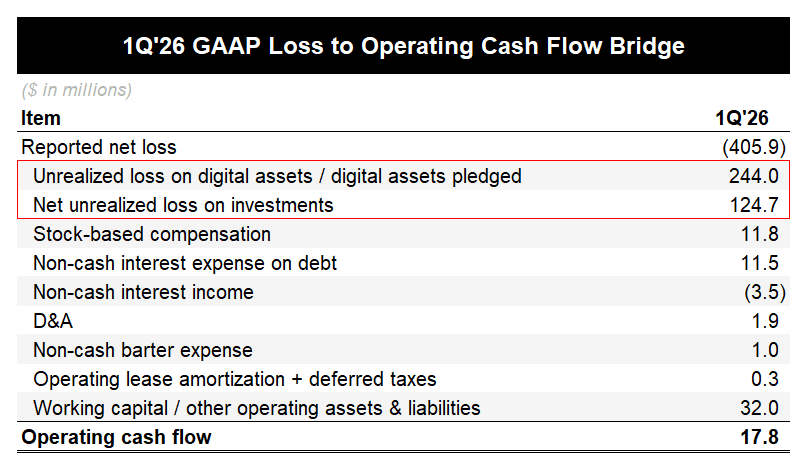

In terms of cash burn, the reported 1Q’26 net loss of $406mm sounds alarming until you back out non-cash items. $369mm was unrealized marks on digital assets and equity securities. Underlying operating burn is small. Operating cash flow was actually positive at $18mm for the quarter, mainly due to working capital.

Assuming there is no refinancing event, to cover the full $1bn in cash, DJT would need some combination of liquidating the equity book (after unwinding the option overlay), selling BTC and crystallizing the loss, monetizing the TAE note, or refinancing into new debt or equity.

What Does The Bond Indenture Allow?

The bond is at 93 for two reasons working together. The collateral securing the claim is bitcoin, equity securities, and a slice of cash, which is to say roughly 3/4ths of the pledged package marks to market on a single risk factor.

The market is pricing some non-trivial chance the company tries to push holders into a deal rather than write the $1bn check. Whichever piece is weighted more heavily, both run through what the indenture allows.

Three pieces matter: what the document protects, what’s actually behind the secured claim today, and what the company can do with majority consent.

Let’s run through each one by one.