Credit Weekly: The Co-Op Is The Trade

Inside the 3rd generation of LME warfare, where creditors fight each other and only the advisors get paid

Are you watching what’s happening at CDK Global?

Software for car dealerships. Brookfield bought it in 2022 for ~$8 billion. $5.5 billion of debt. The type of credit under AI crosshairs.

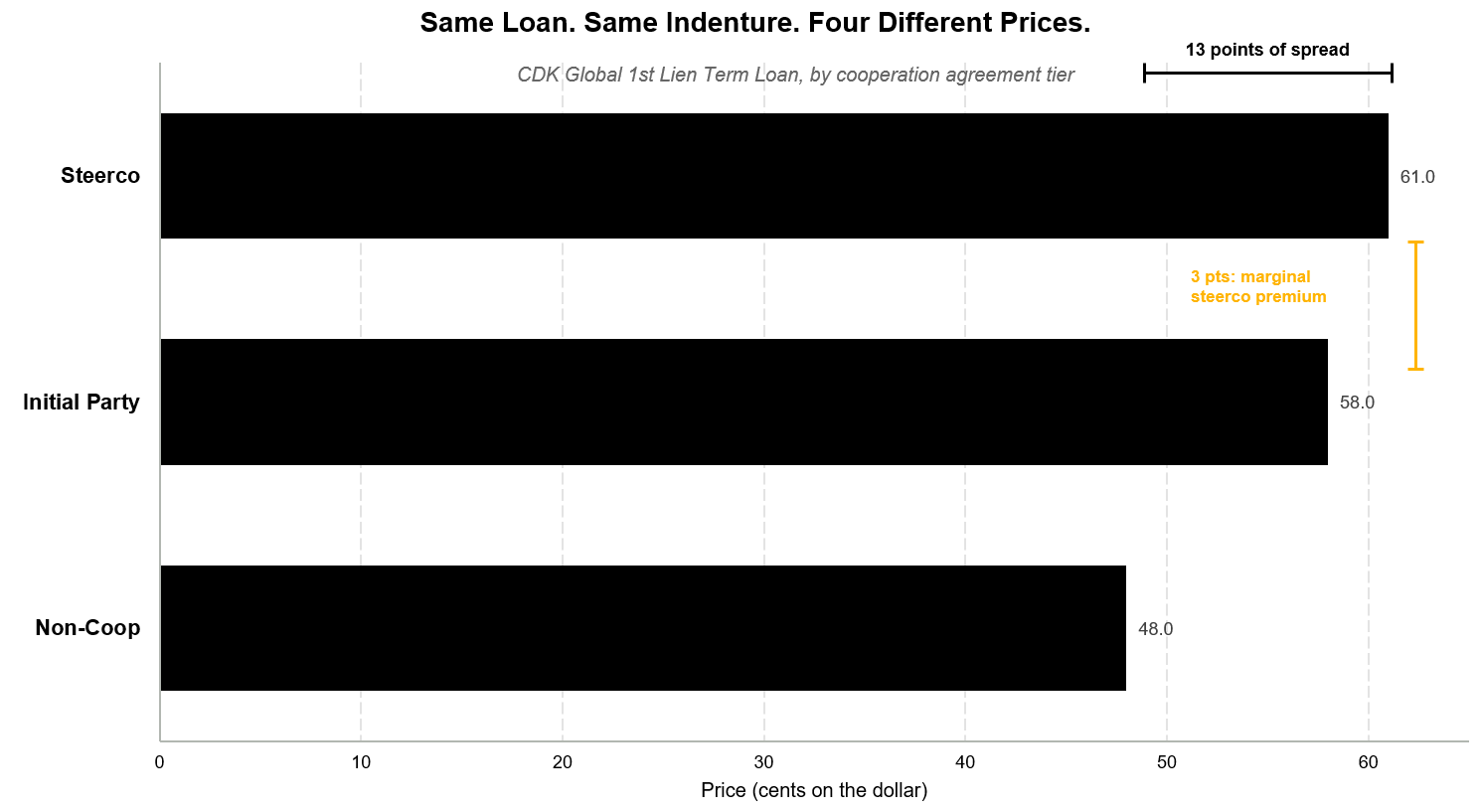

The 1st lien term loan trades at three different prices right now. SteerCo around 61. Initial party around 58. Non-coop paper around 48. Three tiers on identical paper, decided by which email you got and what time you signed it. Top to bottom, that’s roughly 13 points of spread on the same claim.

Ten years ago an LME (liability management exercise) meant creditors vs. the company. Adversarial but symmetric. Both sides had counsel, both sides had leverage, everyone went home with something.

Five years ago the fight became creditor on creditor through document changes. Serta, Envision, PetSmart. The sponsor and a subset of creditors would amend the docs to subordinate everyone else. Drop down the IP. Issue super-priority new money that primes the existing first lien. The lenders who got cut out ended up holding paper that had been legally subordinated by document amendments they couldn’t stop.

Now the fight has moved one level deeper. No drop-downs or priming. Same instrument, same indenture, same claim. The differential recovery comes from a private cooperation agreement that the participating lenders sign with each other. The paper is identical. The economics are not.

The Friday Email

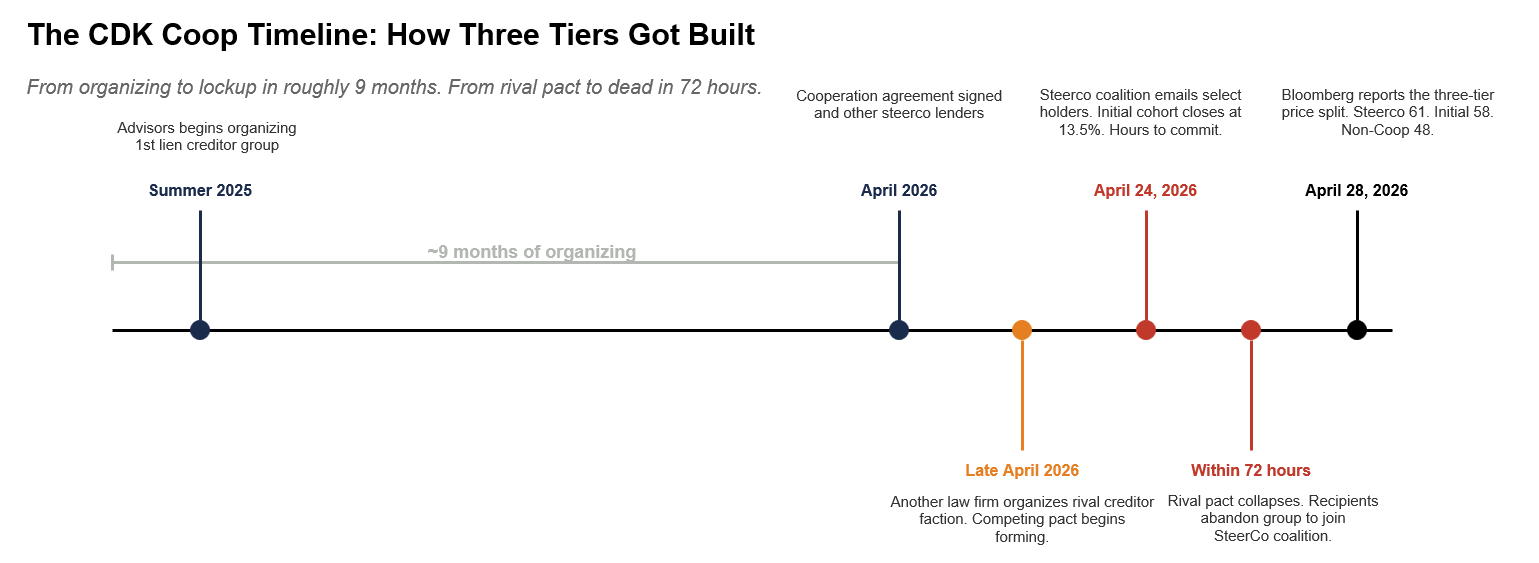

Here’s how the three tiers got built.

A group of CDK’s largest 1st lien lenders signed a cooperation agreement earlier this year. The pact bound them to negotiate as a bloc against any sponsor-led restructuring. Standard playbook for the early stage of an LME setup. That group became the SteerCo.

A few days later, a separate group of holders who hadn’t been included in the original coalition started organizing their own pact. Different economics. Different terms. A genuine attempt to fragment the lockup before the sponsor showed up to negotiate.

That’s when the Friday email arrived. That afternoon, the existing creditor coalition emailed a select list of holders. The initial cohort would close at 13.5%. The offering would close shortly. Hours, not days.

A competing creditor faction had been organizing a rival pact. The Friday email killed it inside 72 hours.

The coop itself is a legitimate legal contract. What’s changed is how it gets built. Advisors aren’t waiting for creditors to find each other and coordinate. They’re running the formation as an outreach process, identifying preferred participants, and using time pressure to drive lockup before anyone else has a chance to organize.

There is no statute that produces 13.5%. The artificial cap was set high enough to give the SteerCo the lockup they needed and low enough to leave a meaningful slug of creditors outside, where the second tier could be sold to them on worse terms. Manufactured scarcity creates the bloc.

The Friday timing did the rest. Advisors had spent days knowing the cap was coming. The recipients had hours. Nobody had time to coordinate with anyone else before the offering closed.

This wasn’t sloppy. The advisors knew exactly what they were doing.

The Advisor Tax

A large, heavily negotiated coop can run through multiple advisor seats. Company counsel. Company financial advisor. SteerCo counsel. SteerCo financial advisor. Sometimes separate counsel for excluded or late-joining creditor groups. That can mean $10+ million of professional fees before the company has solved anything. In the ugliest situations, with litigation, multiple creditor factions, and serial amendments, the number runs higher.

The exact number matters less than the structure. The advisors are the only constituency with guaranteed recovery.

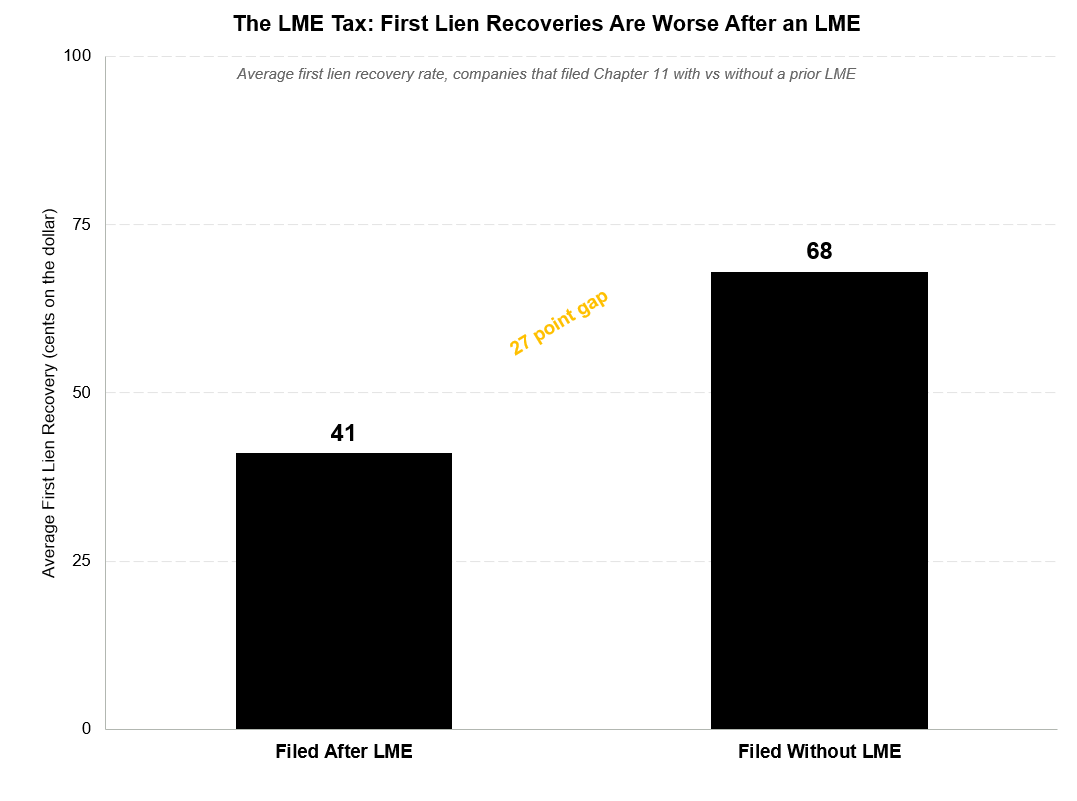

The creditor economics are less certain. The 13 point spread between SteerCo and non-coop paper is the full waterfall. What the SteerCo actually captures vs. the next tier down is closer to 3 points, the marginal economics of being in the top group rather than the second. Add a coop fee, potential backstop economics, and whatever priority or exchange consideration the participating group receives, and the headline can look like high-single-digit points. But that value is paper value until the structure survives the next fight. And on the empirical track record, 75%+ of these deals end up filing anyway within 24 months. The LME is just a toll road to the eventual filing.

This Is Not Lending Anymore

Think about what’s happening. Some of the brightest people are spending months game-theorizing how to extract a few points of recovery from each other on a software company that runs car dealership paperwork. That’s the activity.

Lending used to mean something. You looked at a business. Decided whether it could service the debt. Priced the risk. Bought the bond. The borrower paid you back or they didn’t. If they didn’t, you took the keys and ran the workout.

That isn’t what is happening at CDK. The credit decision was made years ago, by people who in many cases don’t even work at the funds that hold the paper anymore. The activity now is structural extraction. Analysts at the largest credit shops are spending weekends on calls about which 13.5% of which sub-tier gets which fee on which tranche. Law firm partners are billing hundreds of thousands a month to design the structure they’re extracting from. Junior bankers and associates are pulling all-nighters on cap tables and inter-creditor agreements that exist solely to determine who gets better economics on the same loan.

None of this makes CDK better. The company still has the same software, the same dealer customers, the same competitive pressures, the same management team. Not a dollar of the advisor activity flows into the operating business. Not a single car gets sold faster because of these activities.

We’ve built an entire industry that produces no goods, generates no growth, and exists to redistribute existing claims among professional creditors after netting out an enormous advisor tax.

You can call that a lot of things. Lending is not one of them.

People on the buyside don’t openly publicize this because every fund reading this either paid those fees last quarter or wants to be in the SteerCo next quarter. Saying any of this in public means burning a relationship with whoever runs your next deal. The other dynamic is uglier. Credit analysts are on the phone with advisors every week. Advisors are the source of deal flow, color, and process information. A fund that publicly criticizes the model loses access to the flow. The flow is worth more to the fund than the criticism is to the asset class.

The Trap Captures You Twice

Once a SteerCo exists, every other creditor has to choose between joining a tier with worse economics or staying out and accepting worse subordination. Bad versus worse. Advisors built the room. Creditors get to pick a corner.

The CDK price split makes it visible. Importantly, the 48 cent paper isn’t just subordinated economically. It’s illiquid. Price discovery has fractured across three tiers. A holder trying to sell at 48 finds a thin bid because nobody knows how to value paper whose recovery depends on which tier the next buyer would land in. Captured twice. Once on recovery. Again on the exit.

In a world without coops, every creditor has the same legal entitlement under the indenture, and the sponsor has to negotiate with the class as a whole. With coops, the sponsor negotiates with the SteerCo. The indenture gets bypassed by a private contract that the non-signers never agreed to but are bound by economically.

Where This Goes

The structure repeats. Some version of what happened at CDK is going to play out at every distressed software credit hitting its maturity wall over the next 18 months. The advisors are running the playbook. The buyside knows it and signs anyway, because the alternative is being the holdout in a fragmented class with no leverage.

But the holdout case is real in the right setup. Where coop participation is concentrated in a small SteerCo and the maturity is near-term, holding out can produce a better outcome than signing. CDK probably isn’t that setup. Others will be. I wrote about the holdout trade last month.

This is the game now. The structure didn’t exist five years ago. It exists now. Every distressed software credit is going to be priced through it. Pricing it correctly is the work.

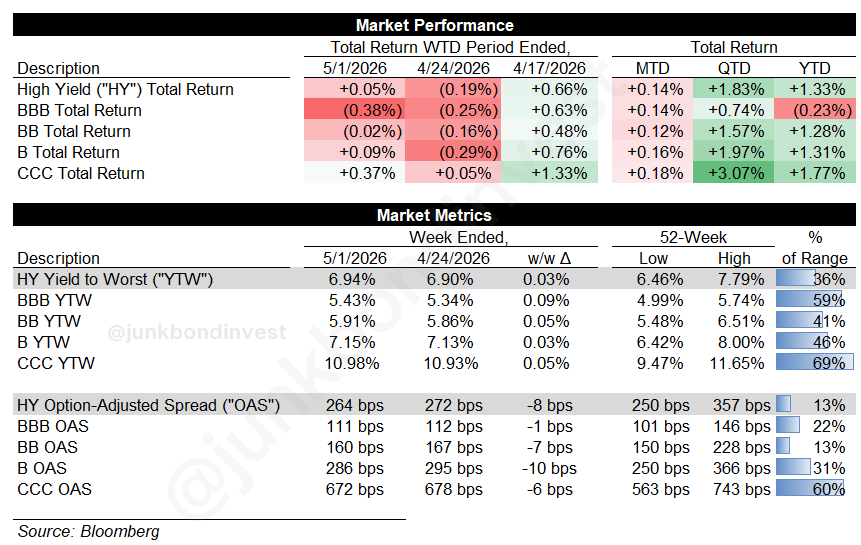

Market Performance

HY total return finished flat on the week at +0.05%. CCC led at +0.37% and are outperforming YTD at +1.77%. HY spreads tightened to 264bps. Index yield at 6.94%, sitting in the 36th percentile of the 52-week range. CCC spreads at 672bps, at the 60th percentile of the range. The dispersion is real even as the headline tightens.

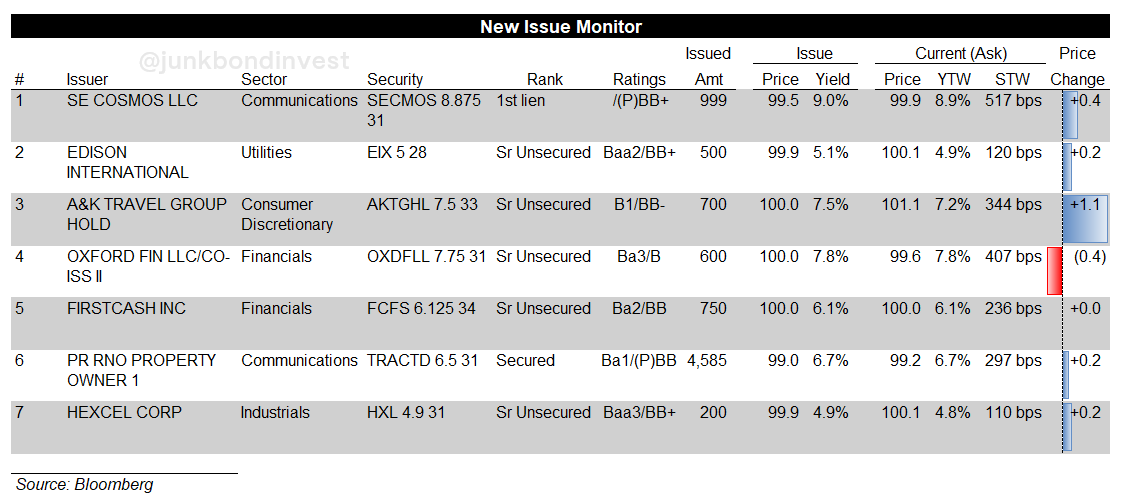

Primary Market

HY printed $7.6 billion this week bringing YTD issuance over 50% vs. last year. A&K Travel debuted at 7.50%. FirstCash and Oxford Finance both upsized. The bid for paper outside the AI blast radius is intact.

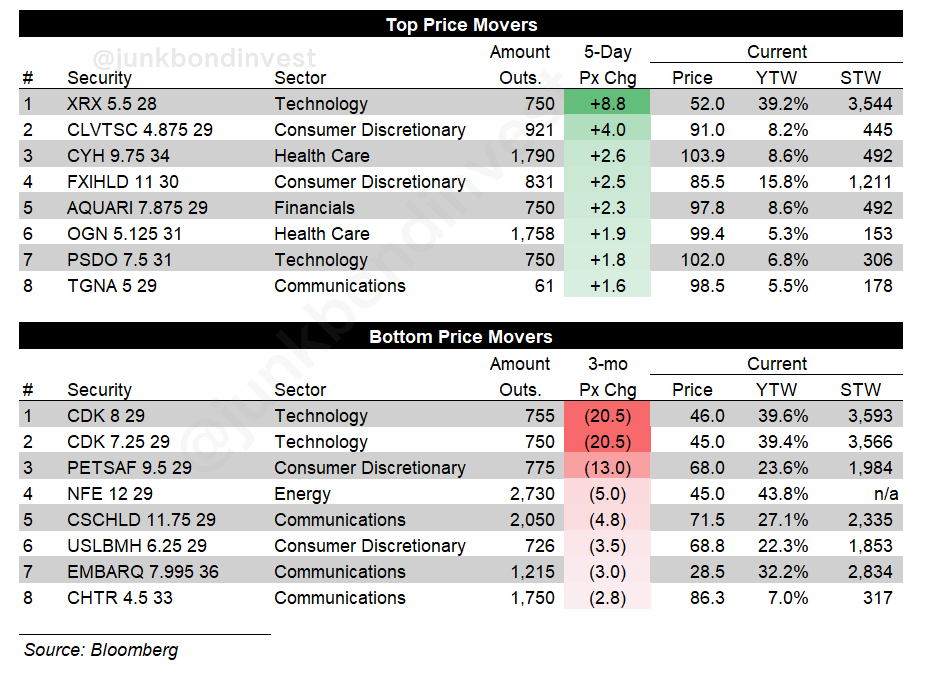

Secondary Market

JBI Bulletin Board

1) Octus

Octus recently published a whitepaper, The Matured Private Credit Mandate, that gets into the private credit maturity wall I’ve been talking about, what restructurings actually look like when they get resolved, secondary market growth, and the $800 billion AI infrastructure gap keeping deployment alive.

Definitely worth a download if you cover the space.

2) Endex Partnership

I’ve been using Endex for a few months now. It’s an AI agent tool built specifically for excel. It’s my go-to tool for putting together charts and spreading financials (with sourceable citations). Worth checking out.

3) Wharton Online Partnership

Wharton Online and Wall Street Prep have an upcoming Restructuring and Distressed Investing Certificate Program. Starts June 8th. The program covers capital structure, bankruptcy mechanics, and distressed investing, led by practitioners at firms like Silver Point and Ropes & Gray. Code JUNKBOND gets you $300 off, with another $200 off if you enroll by May 11.

4) Now Hiring: Technology/Software Credit Analyst

I’m looking to bring on a dedicated technology/software credit analyst. At least a couple of years covering the sector, buy-side experience strongly preferred. You should know the names, know the docs, and the playbooks. If you’re interested or know someone who fits, reach out with a brief note on your background.

a brilliant, and foreboding, article

thank you