Credit Weekly: Warsh's Blind Spot.

A framework for the last cycle, installed at the start of the next one.

Kevin Warsh has spent the last several years calling the post-pandemic inflation episode the worst Fed policy error in half a century. Forty to fifty years. His phrase. Repeated everywhere.

The implication every time is the same. The Fed was slow. Read the signal late. Waited for the smooth middle of the distribution to confirm what the tails were already screaming.

Tuesday at the Senate hearing he asked for the job. Called for “regime change in the way the Fed conducts policy.”

Then he told you what regime change looked like to him.

Trimmed means. Look through tariffs. AI productivity to carry the disinflation forecast.

Every item bends the same direction. Smoother read. Slower reaction. Lower bar to cut.

What the Dallas Fed actually says

First, the setup.

Trimmed mean PCE is an inflation measure that ranks every item in the consumer basket each month, throws out a fixed percentage from the top and the bottom, and averages what is left. The idea is to filter outliers and reveal the underlying trend. Core PCE, on the other side, is the Fed’s main inflation gauge. It strips out food and energy because those bounce around. Both filters. Different numbers in different regimes.

The Dallas Fed published a paper on April 16 whose conclusion creates an immediate problem for Warsh’s preferred framework.

Trimmed mean PCE lagged core and headline in 1974. Lagged again in 2021. The trimmed mean cuts the top and bottom of the price change distribution. When that distribution skews positive, the measure strips more signal off the top than the bottom. What comes out is a downwardly biased read on the underlying trend.

The Dallas Fed says it in plain language. When skewness flips from negative to positive, the trimmed mean can mislead.

The distribution is skewing positive right now. Tariffs in core goods are doing the work. Non-housing core services have shown some acceleration in early 2026 and are becoming a larger source of upside outliers. The Dallas Fed flagged the combination explicitly. They added a second problem on top. Gradual price increases from tariffs may not register as outliers at all. The trimmed mean does not strip them out. It absorbs them slowly into the trend.

The institution that builds the index is warning that the index can understate inflation risk in this regime. Warsh is leaning on it anyway.

Look at the gap

Trimmed mean PCE is running at 2.3% through February. Core PCE is at 3.0%.

That is a 70 basis point gap that did not exist before September of last year. The two measures tracked each other tightly from 2023 through September 2025. Then they diverged. Core kept rising. Trimmed mean kept falling.

The gap is not noise. It is the asymmetric trimming the Dallas Fed warned about, showing up in real time. Tariff pass-through in core goods is creating positive skew. Abrupt moves get trimmed out. Gradual moves bleed in slowly. The measure is weak as an early-warning signal in this regime.

Bessent already moved

Scott Bessent was publicly calling for rate cuts not long ago. He recently acknowledged near-term cuts are inappropriate.

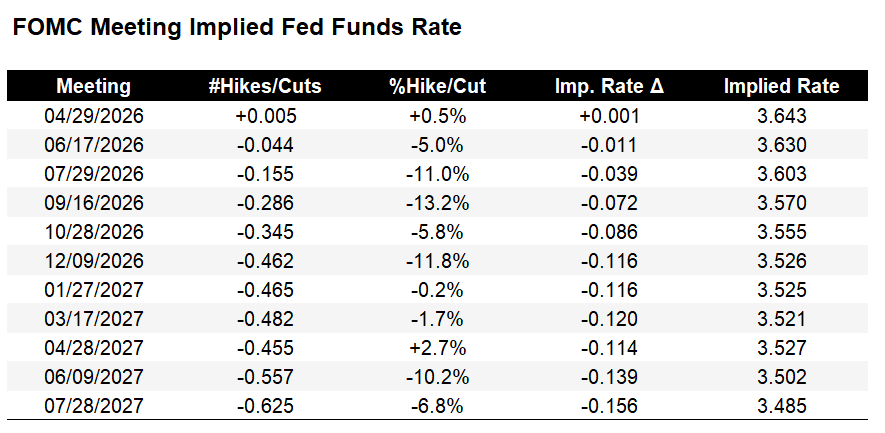

The question is whether Warsh pivots before or after he is confirmed. The Banking Committee votes April 29. Powell’s term ends May 15. That is the window.

The front end is not pricing this asymmetry. The base case for next week’s FOMC is hold, soften forward guidance, two 25 basis point cuts later this year. That same consensus also concedes core PCE is stuck at 3 percent.

The market is pricing both. That path requires energy fading, labor softening, and core rolling toward 2 percent on schedule. Without those, one side gives. Whichever way Warsh leans tells you which side gives.

The AI productivity argument is showing up in credit as inflation

Warsh has leaned on AI productivity as part of the case for a lower-rate path, even though he tempered the claim at the hearing.

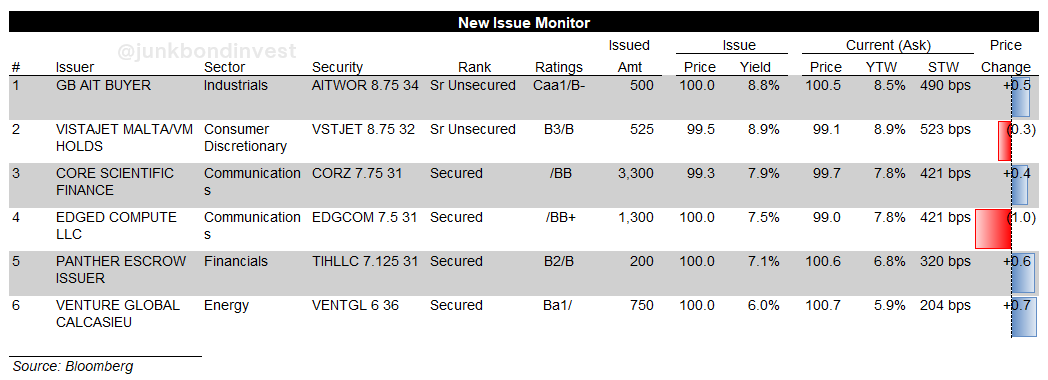

Look at the leveraged finance pipeline.

Roughly $13 billion of data center high yield issuance hit in April alone. That is around 40% of total April high yield supply. Core Scientific brought a $3.3 billion deal at 99.25 OID. Edged Compute brought $1.3 billion. The BB-quality HY bid and IG crossover demand absorbed all of it without a hiccup.

The capex that promises disinflation is inflationary on the way in. The capex is happening now. The power demand is here. The labor competition for the workers building the infrastructure is too. The productivity gains are years out.

Warsh is using a multi-year disinflation narrative to justify a near-term rate cut framework. That timing mismatch is the problem.

The case for dovish-Warsh, and why it fails

For the dovish Warsh trade to work, most of these have to break the right way within twelve months.

AI productivity hits in six to twelve months, not three to five years. Tariffs prove one-off rather than persistent. Energy normalizes by Q3 with the Strait reopening cleanly. Non-housing core services rolls over rather than accelerating further.

That is a parlay, not a base case. Several require resolutions that are not in motion. The front-end base case requires the parlay to hit. That is a favorable path through several unresolved shocks, not a clean base case. The market is pricing it as if it were.