Credit Weekly: The Building Is the Credit

The market prices the tenant. The risk sits in the residual.

A hyperscaler data center bond looks like one of the cleanest credits in the market. An IG tenant, a long lease, and a hard asset underneath. That profile is exactly why the risk in it goes unpriced.

Buy one and you are not buying Microsoft. You are buying Microsoft for the contracted years of the lease, and after that a building, its value resting on whether anyone still wants it once the contracted cash flows run out.

The market prices the lease and treats the building as a pass-through, handing you the residual for free on the assumption it is worth close to par. A growing share of the risk in this paper sits in exactly that residual, and most people are not pricing it.

Start with the cleanest version of the problem: what you actually own when you own one of these bonds.

The Tenant Is Not the Entire Asset

There is no Class A, Class B, Class C convention in data centers the way there is in office or industrial. No premium for a facility that can be re-densified cheaply, no discount for one that cannot. The credit curve is flat where it ought to be steep, because the tenant and the lease carry the entire analysis.

That holds only while the lease term and the debt term line up. A 20-year lease behind 10-year paper is not the same risk as a 10-year lease behind 10-year paper, and neither is the same as a structure where the contracted lease is shorter than the life being financed. The market treats all of them as one credit because the name on the lease is the same.

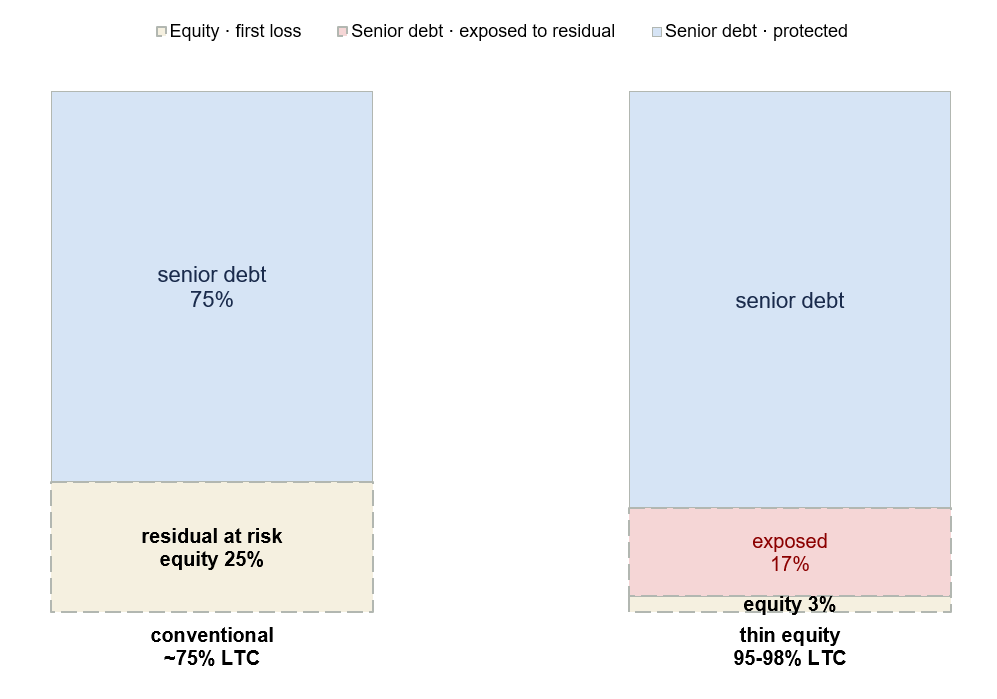

You can see the same indifference in leverage, with public deals now clearing at 95% to 98% LTC and the oversubscription used to pull equity back out of the project. That matters more than the thin cushion suggests. Residual value is an equity risk by design: the lender is meant to amortize out before the building’s worth is ever in question, leaving the bet on what the asset fetches in 10 years to the equity underneath. Strip the equity down and back-load the amortization, and that bet quietly migrates onto the bondholder, unpriced.

The tenant is not even fixed for the term the analysis assumes. Some leases permit assignment, and unless equivalent credit support remains in place, the IG name underwritten at closing may not be the credit support investors think they own for the full term. Even the credit doing the work in the spread is contingent on terms most buyers never read.

Residual Basis Is the Real Credit Line

Last week I argued the market was not differentiating hyperscaler-leased paper from neocloud-leased paper, applying one spread across a real gap in tenant quality. Hold the tenant constant and a second, more important gap appears.

The number that decides it is residual basis: how much of your principal comes back from contracted rent you can model, and how much rides on re-leasing or refinancing the asset later. The first is a real estate loan with a defined exit. The second is a bet on a building, or on a tenant who does not yet exist.

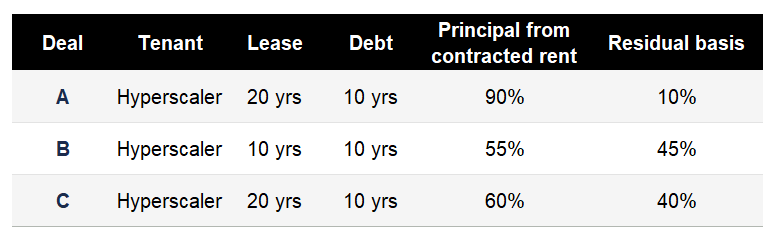

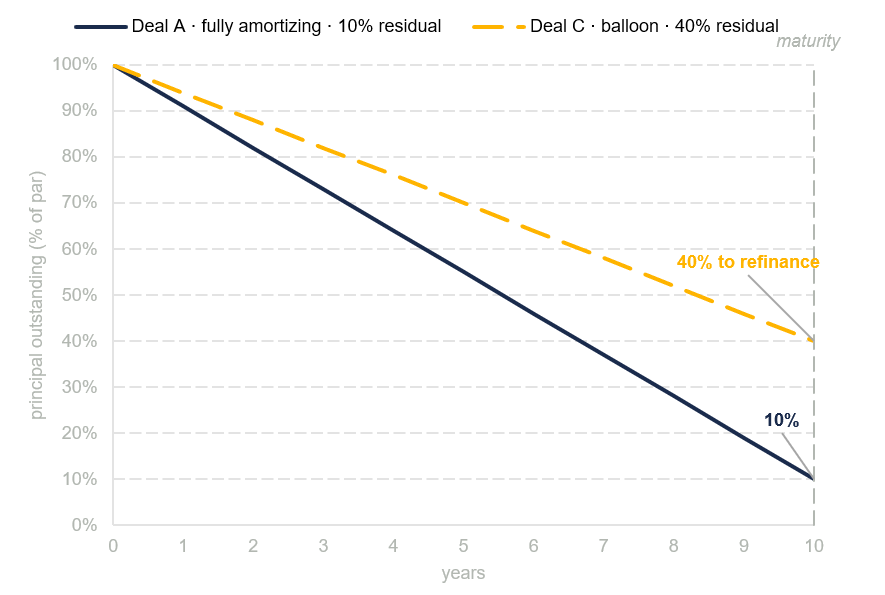

Same tenant, same rating and coupon. Deal A amortizes almost all of its principal from rent under contract. Deal B runs out of lease the day the bond matures. Deal C looks identical to A on the page, the same tenant and the same 20-year lease behind 10-year paper, but it is sized as a partial amortizer with a large balloon, so 40% of recovery depends on refinancing against the back half of the lease and the building underneath it.

Three bonds the market prices within a few basis points of each other. Three different credits. The headline terms, the ones that set the spread, are the ones that hide the difference.

Estimating residual basis is not complicated, which is part of what makes the omission strange. Take the bond’s amortization schedule and ask how much principal retires from contracted rent over the life of the paper. Whatever is left at maturity is the balloon, and the balloon is the residual basis. A bond that pays down steadily over a 10-year term against a 20-year lease is mostly contracted. A bond that IOs for 9 years and bullets in year 10 is almost entirely residual, however IG the tenant looks on the front page.

The lease term remaining at the refinancing date is the other half of the calculation. A balloon that comes due with 15 years of contracted hyperscaler rent behind it is a financeable asset. The same balloon coming due with 3 years of lease left is a building looking for a tenant, in a market that may by then have repriced the whole sector. Residual basis tells you how much you are exposed. The remaining lease at the refinancing point tells you how dangerous the exposure is.

Run the screen this way and the sector reorders around the only number that matters: what fraction of par is contracted, and what fraction is a balloon. One is a credit you can underwrite. The other is a forecast about a building and a market a decade out.

The rating agencies understand this and notch hard when debt does not amortize inside the first lease term, and they notch faster when repayment leans on an extension or a re-lease. The structured market reflects it in the gap between fully amortizing deals and those built around an anticipated repayment date, with calls stacked at years 8, 12, and 16 to manage exactly this exposure. The $29bn Meta-risk project financing that cleared last year was built on that logic, the call schedule doing work the lease alone could not.

This is the normal case, not the edge case. Most of these structures do not fully amortize from contracted rent, because the cash flows are not long enough, so a slug of principal is always left to refinance. The paper is not the clean credit pass-through it is sold as. Bullet structures, single-asset deals, and thinner amortization are pushing the residual share higher, not lower. The part of the credit nobody prices is the part that keeps growing.

Hiring in Credit?

The Refinancing Leg

The residual is not a vague unknown. It is a specific event: a refinancing, on a date you can read off the structure, into conditions you cannot.

When a balloon comes due, three things have to hold at once.

The lease has to have enough term left to support new debt.

The market has to still want data center paper at a price that clears.

The asset has to still support a loan.

The structures pricing today are underwritten as if those 3 are independent and all 3 hold. They are not independent, and they tend to fail together.

The structures do push back on this. A master trust pools many assets and blends their maturities, so a single balloon refinances against a longer weighted-average stream rather than one expiring lease, which genuinely softens the timing risk. What it does not do is change what sits underneath. A pool of single-tenant hyperscaler buildings refinanced into a cooler market is still a hyperscaler real estate bet, just a diversified-looking one. Pooling the residual is not the same as pricing it.

The refinancing window is also the moment the holder has the least leverage. A fully amortizing bond never faces it, because there is nothing left to refinance. A balloon hands the borrower an option and the lender a deadline. If the sector has cooled, if rates have moved, if the tenant has signaled it will not renew, the refinancing the residual basis quietly assumed becomes the hardest financing in the structure to execute, at exactly the moment it has to happen.

One bond is repaid by a lease. The other has to find a new lender, a willing market, and a usable building, all on one date years from now.

Format Can Hide the Residual

The corporate market makes none of these distinctions, and that is where the residual disappears most completely.

Earlier this year a large single-tenant data center, leased long term to a hyperscaler, was financed in the IG corporate market rather than as an ABS. In corporate form it read as clean IG paper, and within days other developers were asking their bankers to put the same trade in corporate clothing, because the format quietly lowers the apparent cost of the residual by hiding it. Comparable assets in the securitized market were clearing at better ratings, shorter maturities, and wider spreads, and once investors put the two side by side the corporate bond repriced wider.

Some of this paper now clears in a day or two with little diligence done, because demand is deep enough that the format prices regardless. Speed is not scrutiny.

A long lease wrapped as shorter corporate paper presents as a tenant credit, and the residual exposure an ABS structure would isolate and amortize against vanishes into the format. That gap corrected quickly because it was visible the moment someone compared the two. The residual mispricing inside a single bond does not correct that way, because nothing forces the comparison.

The Case for the Other Side

There is a real bull case here, and the relative-value argument is stronger for stating it.

These are not ordinary commercial leases. Many are long-dated and structured hell-or-high-water, so the tenant pays through almost anything, and the tenant is among the best credits in the world, funding capex measured in the hundreds of billions out of net cash. The asset underneath is scarce in a way that matters: an energized site with interconnection that would take years to replicate does not sit empty for long, so if one hyperscaler walks, replacement demand for the power and the shell can be robust. This is why project finance lenders like the paper. Long lease, elite tenant, hard asset behind a queue no one else can jump.

Grant all of it. None of it touches the residual. A hell-or-high-water lease is bulletproof for exactly as long as it runs and silent on the day after, and the residual is the part beyond the lease. The strongest form of the bull case, that scarcity makes the re-lease easy, is itself a bet on the residual rather than the lease, placed years out into a market no one can price today. It may well pay. The point is that it is a different bet from the contracted rent beside it, carrying different risk, and the spread charges the same for both. Taken seriously, the bull case is an argument for pricing the residual, not ignoring it.

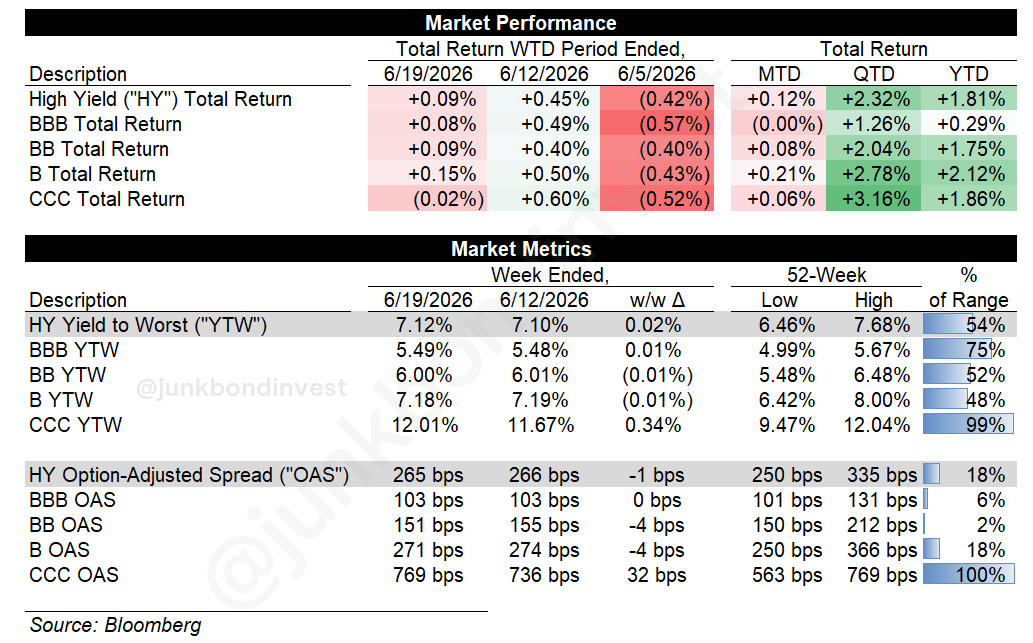

High Yield Market Performance

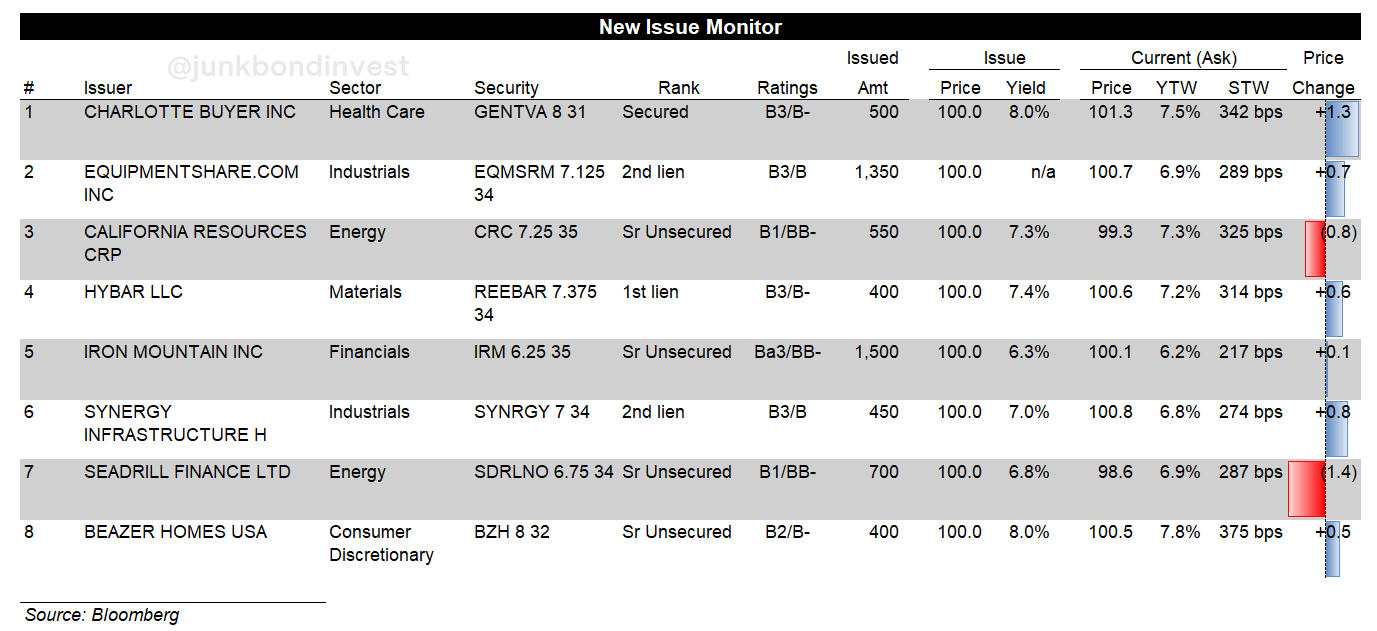

Primary Market

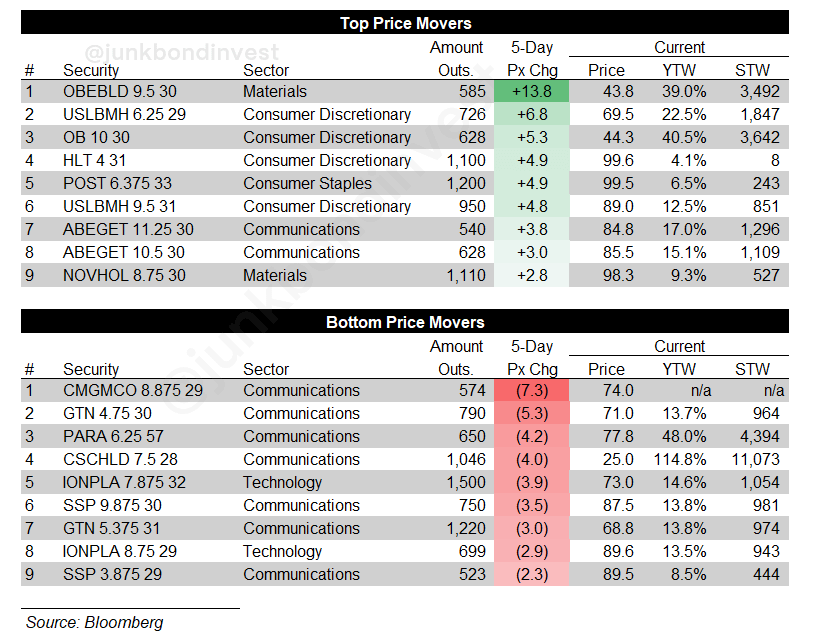

Secondary Market

JBI Bulletin Board

1) Something New is Coming

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. If that’s you, or someone you’d vouch for, reply with a short note on your background.