Credit Weekly: A Utility or an Airline?

If the labs never earn their cost of capital, what happens to the bonds financing the buildings underneath them?

What happens if the AI labs don’t have any pricing power?

OpenAI put a version of that question on the table this week. It is reportedly weighing a steep cut to what it charges for tokens, to pull users from Anthropic and stay ahead of the cuts it expects Anthropic to make in return. Two companies whose businesses still depend on investors subsidizing enormous compute spend, lining up to cut price.

Price cuts do not prove weak demand. They can also reflect falling unit costs. But they do prove something important for credit: the model layer may be more competitive, more substitutable, and less able to hold price than the infrastructure bid assumes. That is what the start of a price war looks like, and a price war is how a market begins to find out whether a product has any pricing power at all. A product that has none, sold at a loss, is one that never earns back the capital behind it.

It matters far beyond the labs.

Roughly a fifth of this year’s high yield issuance has gone to fund AI data centers, sold as infrastructure: long-lived buildings, contracted cash flows, a long runway.

But a data center bond is only as good as the company leasing the building, and those tenants are not all the same animal. Some are hyperscalers with broad, diversified demand, cloud and enterprise and advertising and their own internal workloads, that will pay the rent whatever happens to the price of AI. Others exist mainly to resell compute, and their ability to pay traces straight back to whether the model layer can charge enough for tokens to survive.

If the models never earn their cost of capital, the first group might be fine. The second might not be. The question is whether the market is pricing that difference.

We Have Seen This Before

You know what other industry doesn’t have any pricing power?

Airlines. Or close enough. They have loyalty programs and premium cabins and consolidation, but set against their capital intensity and a fuel bill someone else controls, none of it has ever been enough to earn the cost of capital. Indispensable product, demand compounding for decades, and a balance sheet that turns all of that growth into creditor losses, over and over. One of the most reliable destroyers of invested capital in modern markets.

The record is almost unmatched. Nearly every major US carrier has been through bankruptcy, several of them more than once. Warren Buffett used to hold airlines up as the purest example of a business that grows forever and rewards no one who funds it, joking that investors would have been spared a fortune if someone had grounded the Wright brothers at Kitty Hawk. Passenger traffic rose almost every decade since then. The capital lit itself on fire anyway.

Why Airlines Break Their Lenders

Start with why the original was such a dependable way to lose money.

An airline carries every feature that makes a business hard to lend to, all at once. The product is a commodity; a seat is a seat, and the carrier that charges more loses the passenger. The assets are enormous, debt-financed, and constantly depreciating. The largest single cost, fuel, is set by someone else. Put those together and you get a business that can grow for fifty years and still not cover its cost of capital, with credit that gets impaired every cycle.

AI did not build one airline. The closest analogy splits that model across three layers, and they are not the same credit. The mapping is not clean, and it is worth saying so. A token is not quite a seat, a GPU is not quite a plane, and the building that holds the GPUs is barely an aviation asset at all. The point is not that the parallel is exact. It is that the same dangerous combination, heavy capital set against a product that may not command a price, can be assembled out of these parts.

The labs sell tokens to end users. A token is not a pure commodity the way a seat is; models differ on quality, ecosystem, and the cost of switching, and a dominant one could hold real pricing power that no airline ever had. But this week’s news is a sign that the pricing power may be thinner than the bull case assumes. If it is, the labs are the airlines.

The neoclouds own the GPUs and rent compute to the labs and the hyperscalers. They are the closest thing to aircraft lessors. But a lessor only ever worked because planes held their value and the customer base was diversified, and the neoclouds tend to have neither. The fleet loses value far faster than any airframe; a three-year-old GPU is already being written down by the next generation on the truck. And the book is often concentrated in a handful of customers. It is a lessor stripped of the two things that made lessors safe.

The powered shells, the buildings and the power and the interconnect, are the one piece that is not really airline-shaped at all. If they map to anything in aviation, it is the scarce, location-bound infrastructure no operator can do without, the gate or the takeoff slot rather than the carrier or the plane. And the asset that actually matters is not the concrete. It is the power connection, which is genuinely scarce and, where it is scarce, genuinely valuable. That is what the AI infrastructure bonds being raised right now are mostly secured against, and it is the most durable thing in the stack.

Here is the chain that matters, and it only applies to the second kind of tenant. A shell bond leased to a neocloud is a claim on real estate, leased to a lessor whose collateral is melting and whose customers may be airlines. The rent comes from the neocloud. The neocloud’s revenue comes from the labs. The labs are funded, for now, by investors willing to subsidize a business that does not yet cover its costs. That bond is not infrastructure. It is a bet on how long that patience lasts.

The Market This Week

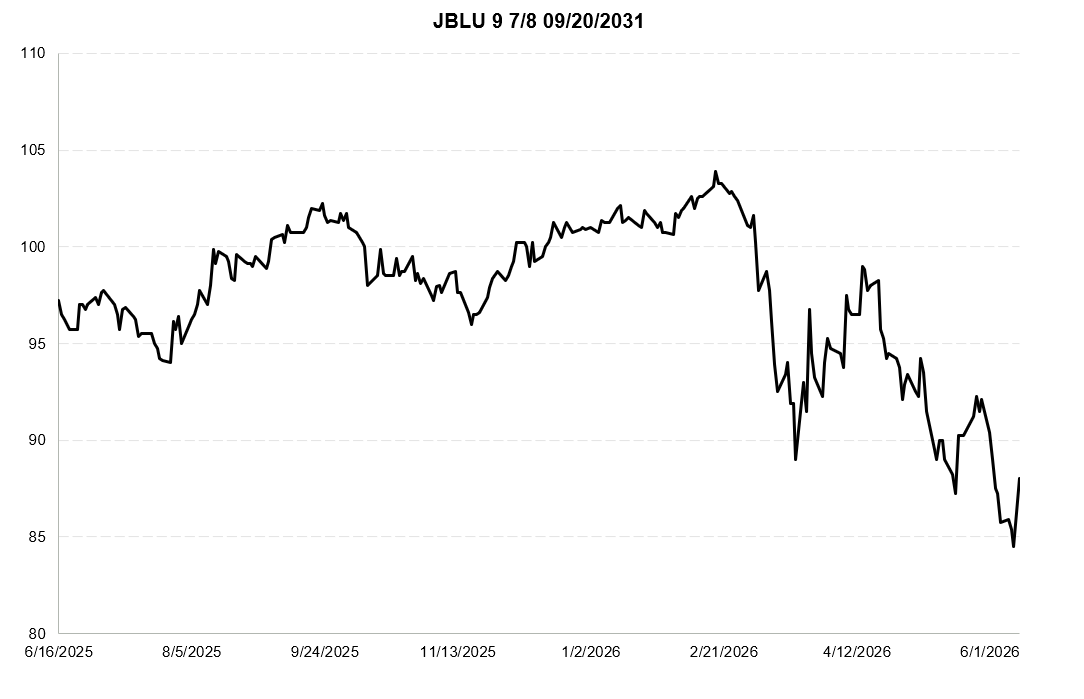

Take a look at JetBlue, whose bonds now yield north of 13%.

S&P just cut the company to CCC+ on a billion-dollar FCF deficit this year and another expected next. Spirit is in bankruptcy. Allegiant priced a secured deal wide, broke it to a 100 handle, and watched it slip to 99.25 within days.

Record numbers of people are flying, and the credit still looks like that. The sector has produced bankruptcy after bankruptcy across fifty years of rising demand. That is the warning the analogy carries, and it is not theoretical.

Now look at how AI infrastructure priced into the same week.

Cipher’s Stingray deal, $810 million at a 6% yield, is secured against a data center in Andrews, Texas leased to Amazon for fifteen years.

Meanwhile, Applied Digital priced $1.59 billion at 7% against a campus in Ellendale, North Dakota leased to CoreWeave.

Amazon pays the rent off cloud, retail, advertising, and its own workloads, whatever happens to compute prices. CoreWeave is a levered single-B neocloud whose ability to pay depends on its own customers continuing to pay it. One landlord rents to a blue chip. The other rents to a lessor that rents to airlines.

The market priced both as infrastructure, and the tenant distinction did not show up with nearly enough force. The bid is discriminating at the margin, but not nearly enough for how different the tenant risk is. It is mostly buying the theme, and the theme is infrastructure.

What It Would Mean for the Credit

So suppose it does not get there. Credit has owned something like this shape before, and learned the rules the expensive way. The asset was rarely the problem. The tenant was. Three lessons to learn from the airline experience.

Structure is most of the outcome. The investors who came through aviation whole owned the secured claim on the asset, not the airline’s unsecured promise. That is the split sitting in this week’s supply. The shell-backed secured paper is the senior secured claim. CoreWeave’s corporate notes are the unsecured lessor bond, a direct claim on the operator. Its existing 9.25% notes gave back a point on the supply while the lease-backed paper held. The market may already be sorting these, even if the spread between them says it has not gone far.

The collateral question starts after the tenant is gone, and the powered shell is better than the bears claim and trickier than the bulls assume. It is not a box of melting silicon; the silicon belongs to the lessor. It is a building, a power connection, and an interconnect, and where power is scarce it can re-lease well. But a shell built to one tenant’s spec in a remote location is not a fungible 737 with a deep global lease market behind it. Recovery turns on whether the next tenant wants that capacity at that site.

The lease is only as good as the tenant’s decision to honor it. Airline creditors lived inside Section 1110 of the bankruptcy code, a short window in which the airline affirmed and cured or handed the asset back. There is no Section 1110 for a data center. If CoreWeave ever restructured, would it affirm the Ellendale lease at that rent, or reject and renegotiate? The bondholders would be downstream of that decision, and the decision would turn on whether its own customers were still paying.

One pattern worth noting, not as an alarm. CoreWeave took a $1 billion equity check and a $6 billion compute commitment from Jane Street, which now reportedly wants to build a data center of its own. Customers funding suppliers so those suppliers can build more capacity for the same customers is not automatically bad. But it is a late-cycle shape credit investors have seen before, in the late-1990s telecom buildout, with vendors financing the carriers that bought their gear.

The Question Is the Tenant

Demand was never the question for airlines. They flew more passengers in 2025 than in any year in history, and the sector had already buried multiple flag carriers. Compute demand can be every bit as real and still leave the credit question open, because what strains an airline is not weak demand but an indispensable product it cannot monetize above its cost of capital.

None of this is a short, which is where the reflexive bears get it wrong. The shell may hold its value, and the Amazon-leased paper may be exactly the utility it is priced as. The point is not to avoid the sector. It is that a landlord renting to a blue chip and a landlord renting to a weak lessor are wearing the same lease at spreads far closer than the gap in tenant risk justifies, and only one of them is a utility.

If there is a discipline here, it is to underwrite the tenant, and the tenant’s tenant, at least as hard as the building. Three questions, which you can ask on any of this week’s prints.

Is the company paying this lease a hyperscaler that pays regardless, or a neocloud whose survival depends on customers holding compute prices that may be commoditizing?

Do you own the asset, or just a claim on that tenant?

And if the lessor failed, would the powered shell re-lease to someone else, or is it stranded at that site for that spec?

The analogy may break exactly where it should. Compute may stay scarce, the labs may find their pricing power, and the economics may close. That is a real possibility, and this is not a call that they won’t. But the question worth keeping in front of you is the one the price war just raised. If the model layer has no pricing power, the pain does not stay with the models. It runs down the lease, through the lessor that can no longer collect, and into the debt that financed the building they all run on.

JBI Bulletin Board

1) Something New is Coming

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. If that’s you, or someone you’d vouch for, reply with a short note on your background.