B&G Foods ($BGS): Paying 11% to Stand Still

A 7x levered food roll-up, a fresh 11% print, and a deleveraging plan that doesn't delever. Where to sit in the stack.

The food business is supposed to be boring.

That’s the whole pitch. People have to eat. Recession comes, they trade down to canned vegetables, the cash keeps flowing, the bonds pay like clockwork. Boring is the point. Boring is why the money is cheap.

B&G Foods just borrowed money at 11%.

Not a lot of companies issue debt with double digit coupons. The ones that do tend to be in trouble, or close enough that the market wants to be paid for the ambiguity.

Either the market got this one wrong, or the boring food company isn’t boring at all. Which is it?

Situation Overview

B&G Foods is one of those companies nobody has heard of but everyone has bought from. Green Giant, Crisco, Ortega, plus roughly 50 other brands of shelf-stable and frozen food across the US, Canada, and Puerto Rico. All of it parked in the middle of the grocery store, which is exactly the problem.

For two decades, the model was a debt-funded roll-up of orphan brands. Big food companies wanted mature, slow-growth names off their books. B&G took them, plugged them into a shared distribution backbone, spent nothing on innovation, and milked the cash. The cash went to the next deal and to one of the fattest dividends in the food group.

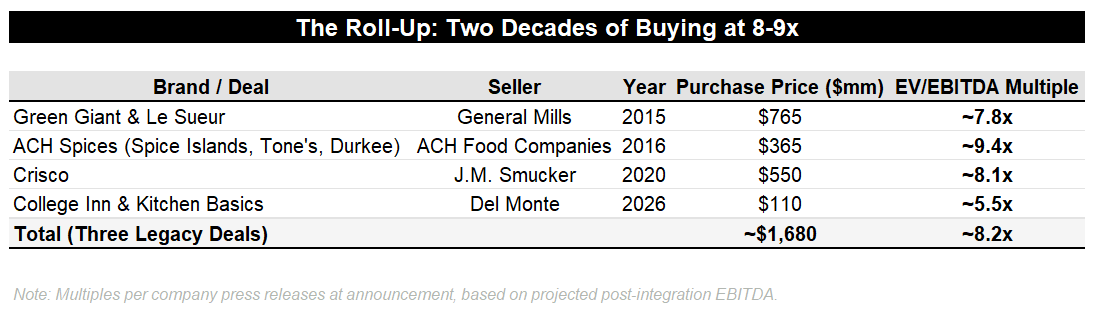

Green Giant came from General Mills in 2015 for $765mm at ~7.8x. Spice Islands and Tone’s came in 2016 for $365mm at ~9.4x. Crisco came from Smucker in 2020 for $550mm at ~8.1x. All of it levered.

The model needed flat categories and cheap debt. It got neither. Consumers drifted out of center-store and frozen toward fresh, private label, and better-for-you, and brands that had been starved of investment for years had nothing to fight back with. Then interest rates went up.

Now the roll-up runs in reverse. Green Giant US frozen went to Seneca in March for $63mm against roughly $200mm of revenue. Le Sueur US fetched $59mm from McCall Farms. Green Giant Canada closes this quarter. Brands bought at 8-9x EBITDA are walking out the door at a fraction of revenue.

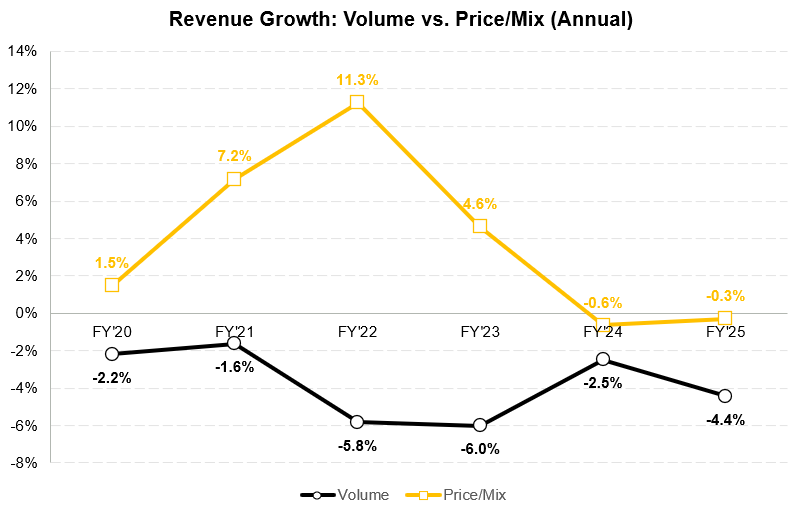

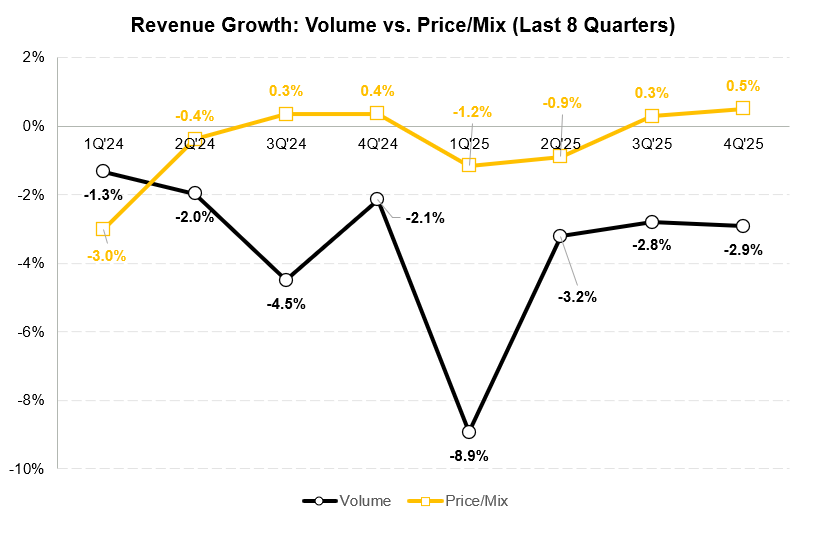

When inflation hit in 2022, B&G pushed price hard, +11% for the year, peaking at +17% in Q4. Volume fell 6%, the classic elasticity trade. Then the pricing rolled off through 2023 and the volumes never came back.

By 2024-25, both levers were dead: price flat to slightly negative, volume still eroding 3-5% a year. That’s the signature of a portfolio losing relevance rather than riding a cycle. Shoppers who traded down to private label didn’t trade back up, and brands with no marketing budget have no way to win them back.

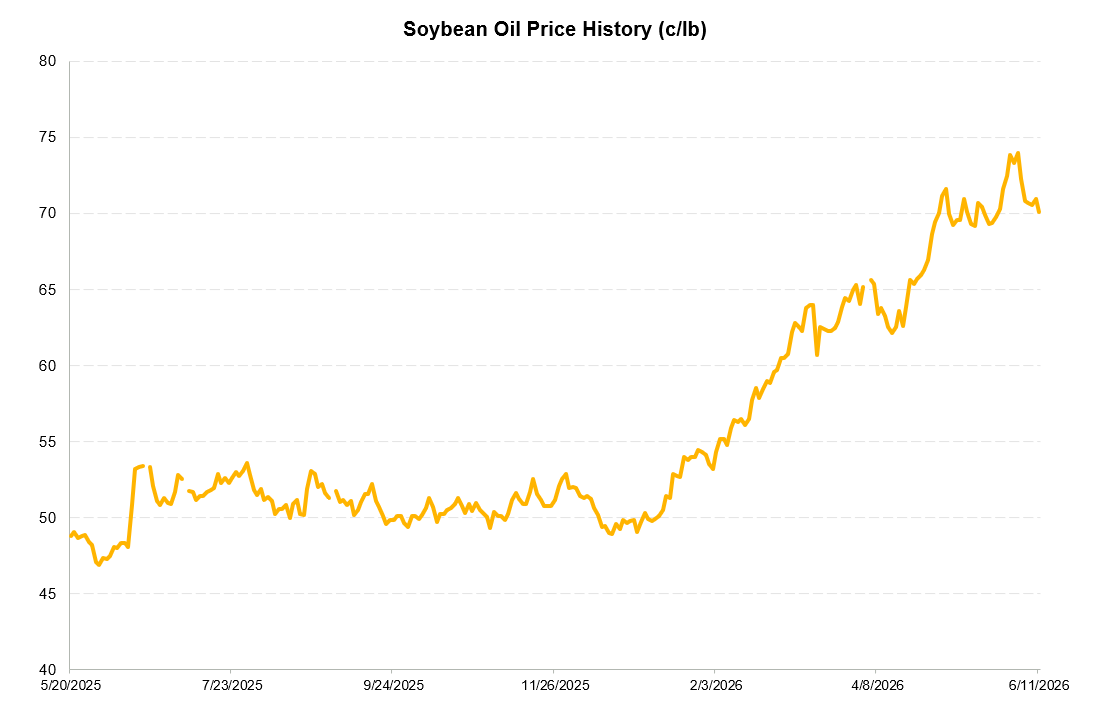

Meanwhile, GLP-1s are the newer risk factor. Roughly 1 in 8 US adults is now on the drug, and the data shows treated households cutting grocery spend MSD, with the cuts concentrated in calorie-dense categories. For BGS, the exposure is milder than for the snack and candy names, since most of the portfolio is cooking ingredients. But Crisco sits squarely in the crosshairs, fats and baking, the same SKU already carrying the soybean-oil problem.

What’s left splits four ways, and the segments have almost nothing in common.

Spices & Flavor Solutions is the crown jewel: ~30% EBITDA margins, +9% sales in Q1. The growth is real and it’s volume-led, which makes it the exception in this portfolio.

The rest of the portfolio is what it is. Meals (Ortega) is stable. Specialty, which holds Crisco, hot cereal, and baking staples, is mature and grinding lower. Frozen & Vegetables runs ~6% margins and is mostly sold. Blend it all and you get ~$1.75bn of revenue, ~$280mm of adjusted EBITDA, ~16% margins.

Then the cost problem. Soybean oil, Crisco’s main input, is up more than 50% year over year and sitting near 2022 highs on biofuel demand. Crisco runs a quarterly pass-through that protects gross profit dollars, but management has already said that if oil stays here, pricing goes portfolio-wide.

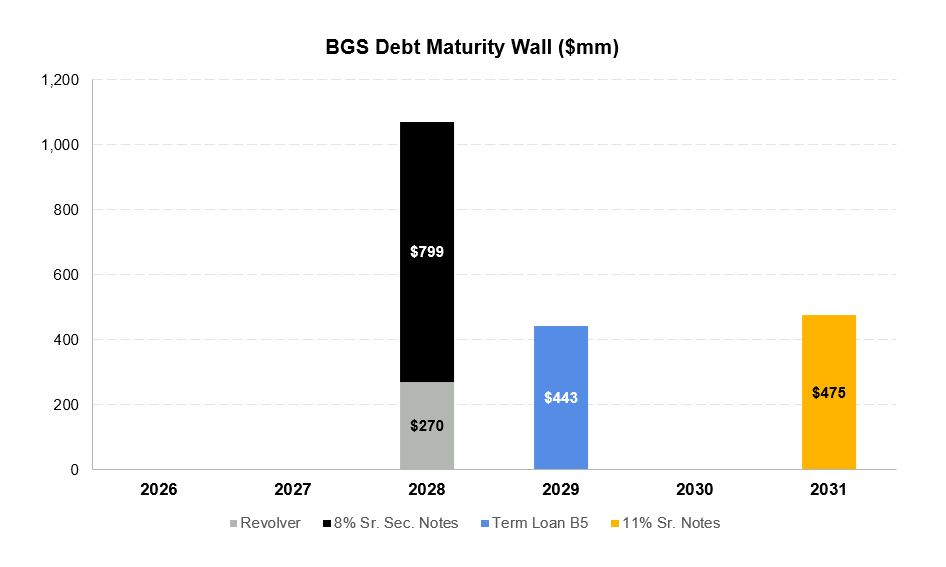

Which brings us to the balance sheet. Net debt is about $2.0bn, a touch over 7x, under an equity stub worth around $330mm. Cash interest runs ~$163mm. Capex is $30-35mm. After taxes and what’s left of the dividend, FCF for actual debt paydown is maybe $30-50mm a year. On $2bn of debt, that barely registers.

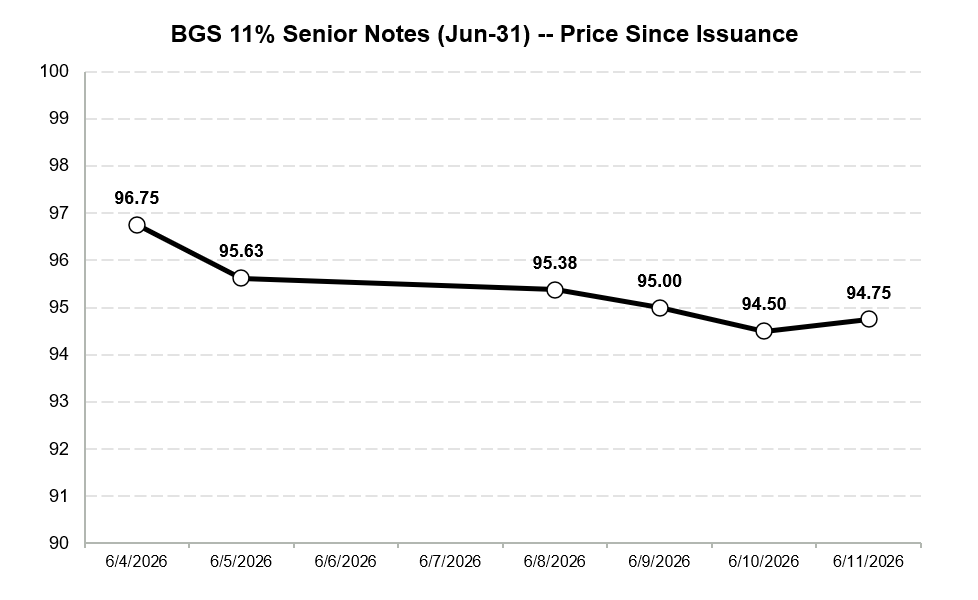

The company also just showed everyone its real cost of capital. Two weeks ago B&G priced $475mm of senior unsecured notes at 11%, issued at ~97, to retire the $509mm of 5.25% notes going current in September. The deal cleared and the 2027 wall is now gone.

The price was steep though. Cash interest on that tranche roughly doubled, from ~$27mm to ~$52mm a year, which consumed almost everything the dividend cut had freed up. The new notes broke below issue and sit in the mid-90s.

So the near-term cliff is handled, but the structure left behind is unforgiving. Three quarters of the debt is first lien, and the next maturity wall is bigger than the one they just paid 11% to clear.

The question now is what a perpetually levered, slowly declining roll-up is worth, with one genuinely good asset buried inside it and a commodity problem bolted to the side.

Here’s what it means for the existing capital structure.