Oddity Tech ($ODD): 9.5% YTM, Net Cash, Broken CAC

Oddity's stock is down 85% on a broken growth engine. Its zero-coupon notes at 69 are pricing a different question.

Here’s an odd one: Oddity Tech.

You’ve probably never heard of them. You’re not supposed to. You’re not the customer. Ask any woman in your life, at least one has scrolled past their Instagram ads. This:

For a couple of years, Oddity looked like it had solved the one thing nobody in consumer solves. Paid acquisition that actually pays for itself. Land the customer at breakeven, make it back when they reorder at 70%-plus gross margins, do it forever. Lifetime value over acquisition cost. The infinite money glitch.

Then the glitch closed.

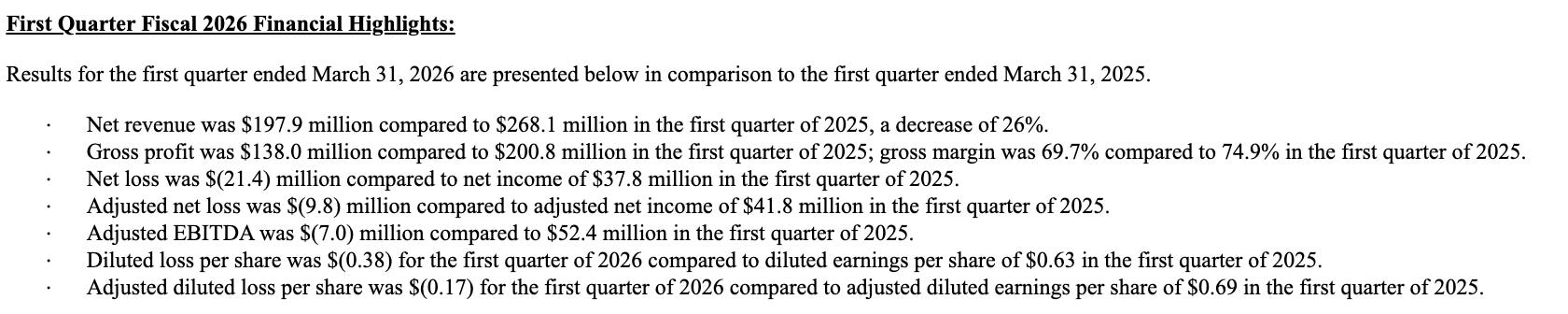

83% more to acquire a customer. Not in one geography. All of them, at the same time. Revenue down 26% in 1Q’26. EBITDA negative. The stock trades near $10, off almost 90% from the highs last year.

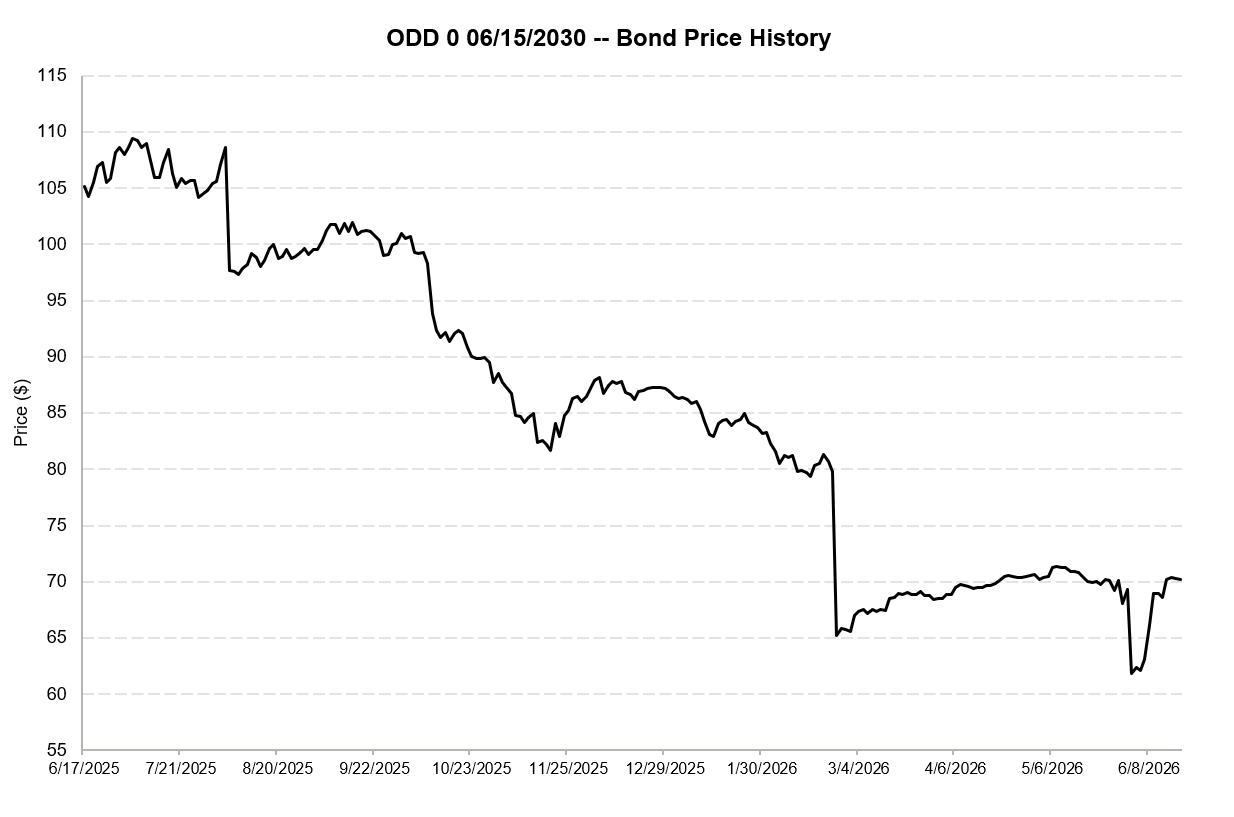

But back when this was all working, Oddity sold $600 million of zero-coupon exchangeable notes due 2030. They go for 69 today. 9.5% YTM. Busted convert sitting under a broken stock.

So who’s buying it at 69, and what do they think they know?

Situation Overview

Oddity is an Israeli company that sells beauty and wellness products online, and almost nowhere else. Two brands carry it: IL MAKIAGE in color cosmetics and SpoiledChild in anti-aging and hair. A third, METHODIQ, just launched.

It’s 97% direct to consumer. No real wholesale, department store counters, or shelf space worth mentioning. You take a quiz, the AI reads your answers and points you at product, and Oddity buys the traffic that feeds the quiz through paid social. Nearly all of that spend goes through one platform: Meta.

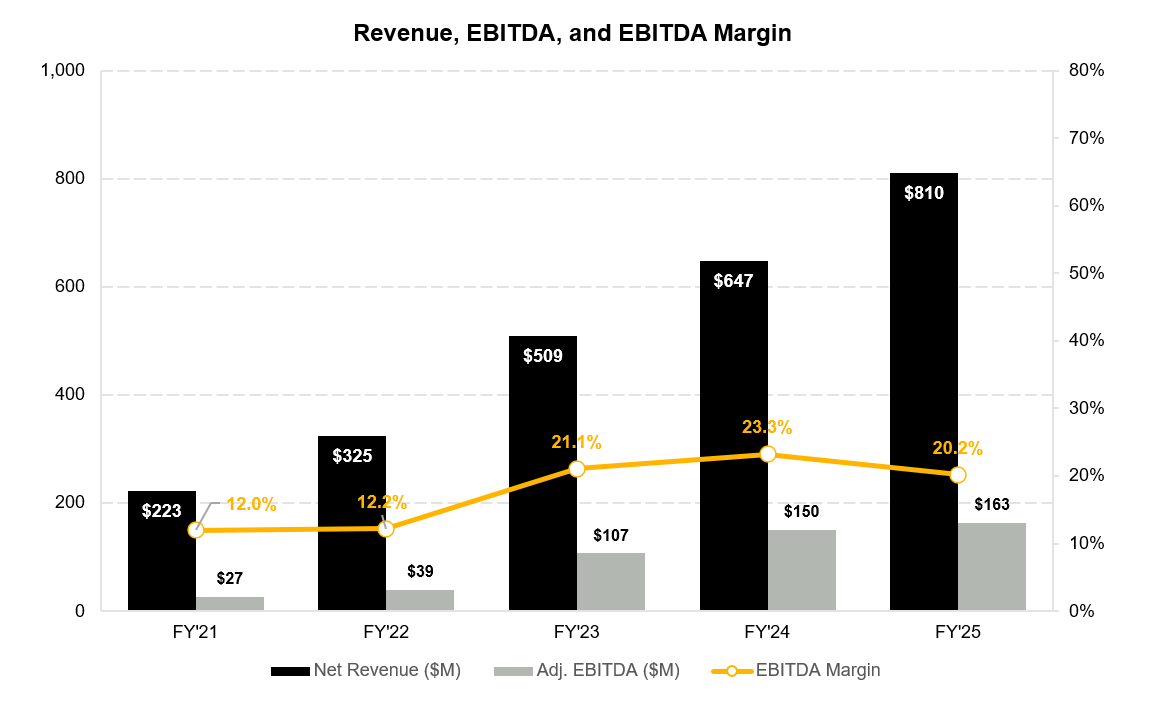

The company went public in July 2023 at $35 on a simple premise. Acquire a customer at roughly first-order breakeven, then earn it back on repeat purchases at gross margins above 70%. For two years, it ran the way it was drawn up. Revenue compounded above 25% a year, first orders and repeats came in about even, and management guided to a long-run 20% growth at 20% EBITDA margins. People bought the algorithm because the results kept showing up.

Then in late February 2026, management got on a call and described a “dislocation” with its largest advertising partner.

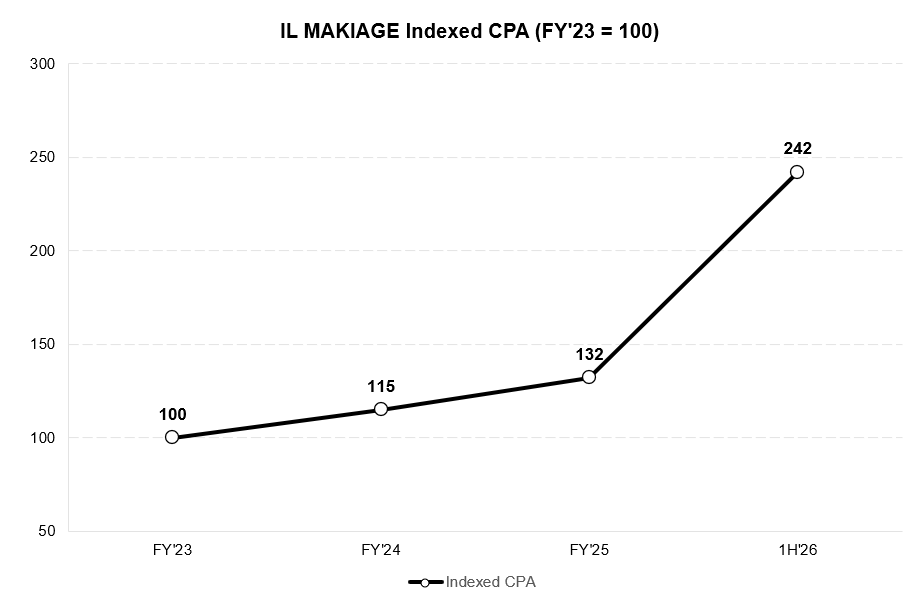

The cost of that word was specific. Customer acquisition at IL MAKIAGE rose 83% year over year in the first half of 2026, after three straight years of mid-teens CPA inflation, the boring kind you can budget around. And it hit the US, Canada, the UK, Australia and Israel at the same time, which is not how failing brands behave. Management’s read is that the problem is technical, an algorithm and signal issue on Meta’s end, not fading demand for the product.

For a business that acquires at breakeven, the math flips the moment a new customer costs more than the first order brings in. Then every acquisition burns cash. The first quarter is what that looks like.

Net sales fell 26%. First orders were halved. Repeats, the customers already through the door, fell only 15%, the one number that held. The mix did the rest: gross margin gave up 520bps to 69.7% on lower order value, and Adj. EBITDA swung from positive $52 million a year earlier to negative $7 million. Management guided Q2 to sales down 25 to 30%.

A quarter in, the engine still isn’t fixed, but the signals are turning. The ad partner thinks 40 to 60% of the inflation is recoverable through its own adjustments. IL MAKIAGE’s acquisition costs fell 28% from April to May, the first sequential relief since the break. SpoiledChild is running a milder version of the same problem, and METHODIQ is tracking toward roughly $25 million in its first year. None of it has restarted the core yet.

Through the collapse, the company repurchased its stock even as EBITDA turned negative. At ~$10/share, the stock is priced as if the engine is broken rather than stalled. But the equity is the obvious security to fixate on, and the obvious one is rarely where the trade is. The better question sits a rung up the capital structure: what Oddity owes, and what it owns against it.

Current Capitalization:

In mid-2025, with the stock in the $60s and $70s and the model still working, Oddity sold $600 million of 0% exchangeable notes due 2030. The conversion price was set far above where the shares trade now, so the equity option attached to the notes is deep out of the money and what changes hands today is essentially unsecured credit. The notes trade around 69 implying a 9.5% YTM.