Credit Weekly: The Residual May Be Obsolete

The market assumes the building stays useful. The hardware it was built for is moving faster than the building can.

A couple weeks ago, in The Building Is the Credit, I argued that once you get past construction risk, hyperscaler data center paper is primarily two bets: the contracted lease, which the market prices, and the residual building value, which it often does not.

The lease is the clean part. The tenant is IG, the rent is contracted, and the cash flows are visible. The residual is harder. It is the building and what that building is worth once the contracted rent runs out.

That first piece was about measuring how much of the bond depends on the residual. This one is about whether that residual is money-good when the bond actually needs it. A building can look valuable on day one, carry an appraisal, and sit behind a flawless tenant, but still fail the refinancing test if the next generation of compute needs a different physical asset.

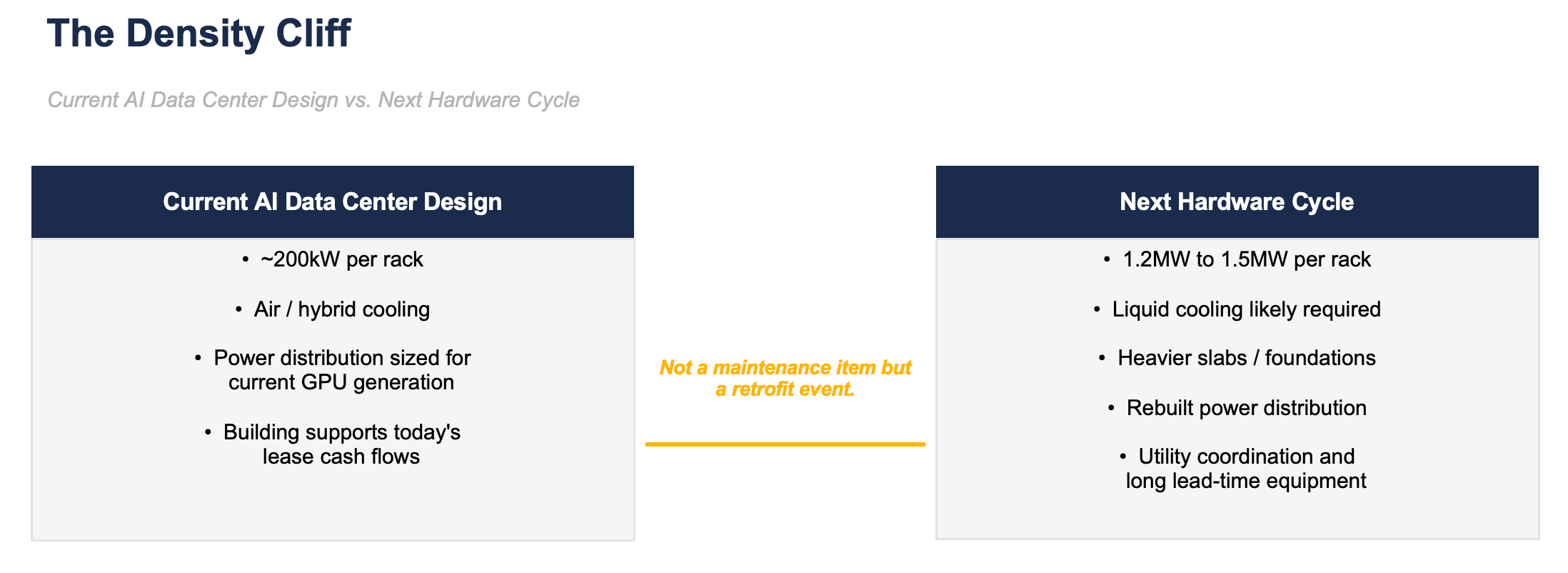

Density Requirements Are Increasing

Much of today’s AI data center capacity is being designed around the density requirements of the current generation. The rough underwriting case is a facility that can support something like 200kW per rack, which works for today’s hardware but may not work for the next refresh cycle. The next turn points much higher, with density moving toward 1.2MW to 1.5MW per rack, and the ceiling keeps moving.

That is not a change you absorb with a maintenance budget. Carrying a building across that gap can mean heavier foundations to bear the load, a different cooling architecture, and a rebuilt power distribution system to push several times the power onto the same floor. The cost can approach a new build, and the timeline can run to years.

The cadence is as much of a problem as the magnitude. A bond financed over 10 or more years has to outlast not one hardware generation but several, each denser and hotter than the last. The chips turn over every few years, while the building that houses them is being asked to stay current across the entire life of the debt, on a capex budget that assumed it would not have to.

Some of what is being financed today may prove to be single-generation infrastructure. It can house the hardware it was designed for, but the hardware after that may not fit without a rebuild. The lease covers the first generation, while the residual quietly assumes a second.

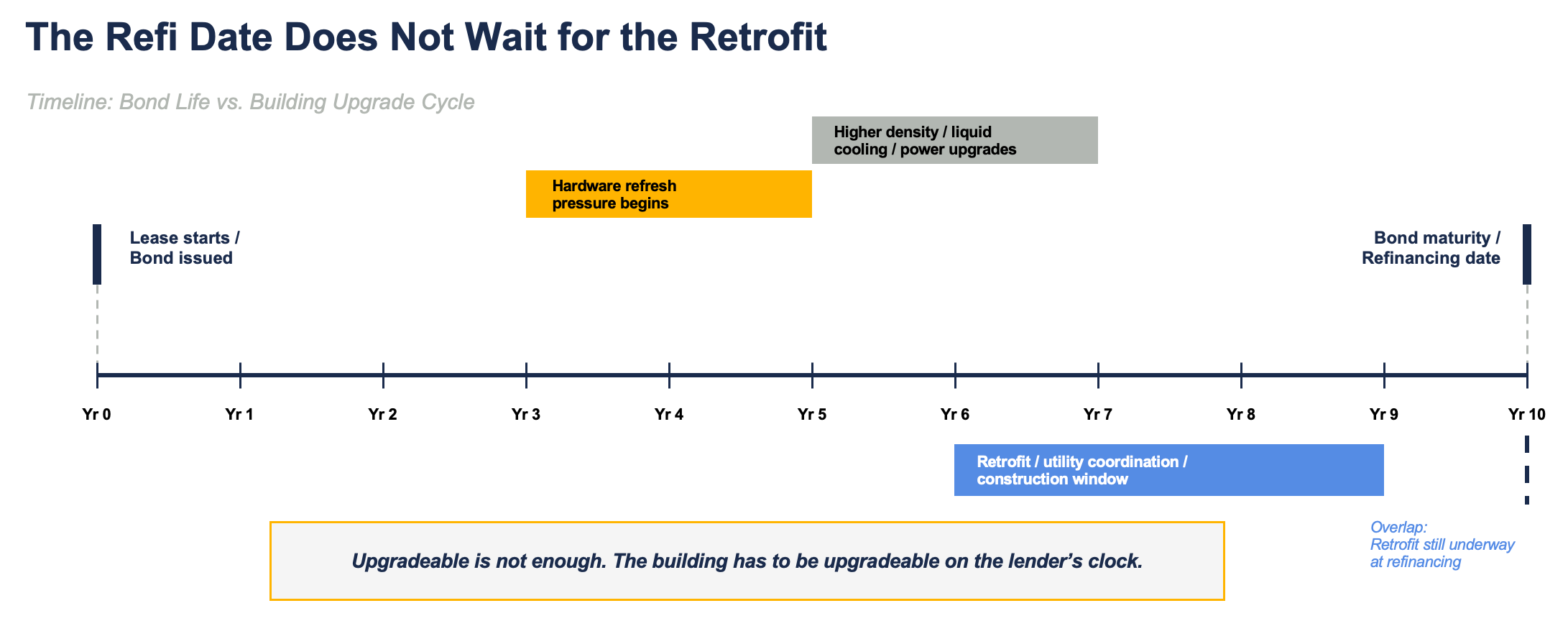

The Retrofit Is A Timeline Risk

Obsolescence does not always mean the building is worthless. Sometimes it means the building needs a second construction project before it can be leased or financed again. That distinction matters for credit, because a retrofit may be technically possible and still fail the bondholder if it takes too long, costs too much, or requires inputs that are not available when the refinancing has to happen.

A facility that needs new cooling, new power distribution, heavier floors, tenant downtime, utility coordination, and scarce contractors is not simply an old building with a capex item. It is a construction project with a maturity date. If the balloon comes due in year 10 and the building needs years of work to support the next density profile, the fact that the asset is “upgradeable” does not solve the credit problem. It becomes the credit problem.

The density cliff reads like an engineering problem until you put a maturity date next to it. Then it becomes a refinancing problem. The building may have a path to relevance, but the debt may not have the time to wait for it. The market underwrites the residual as if it is already there, while the creditor should ask whether the residual has to be built again.

Buildings Designed for One Job

Not every building is equally exposed, and that is where the absence of a clear quality convention bites. There is no broadly traded Class A, B, or C shorthand for data centers the way there is in office or industrial. A facility engineered to be re-densified, or de-densified, at modest cost is a genuinely different asset from one packed into the tightest footprint its economics allowed, and the market often charges roughly the same for both.

The people who design these buildings know the difference. The spread often does not, because the spread is set by the tenant and the lease, and the lease says nothing about whether the shell survives the technology cycle. A long-term lease can make two buildings look identical on a screen while one has flexibility and the other is a single-purpose machine.

Workload cuts the same way. A building running training has different requirements from one running inference, and a site optimized for one is not automatically useful for the other. Training can tolerate lower redundancy and a more bare-bones envelope, while inference often wants to sit close to the data and the users. That makes location part of the asset rather than incidental to it.

A campus chosen purely for cheap power, far from anywhere, can be fine for the workload it was built for and stranded if that workload moves. The building does not become impaired because demand for compute disappears. It becomes impaired because the demand that remains needs a different building.

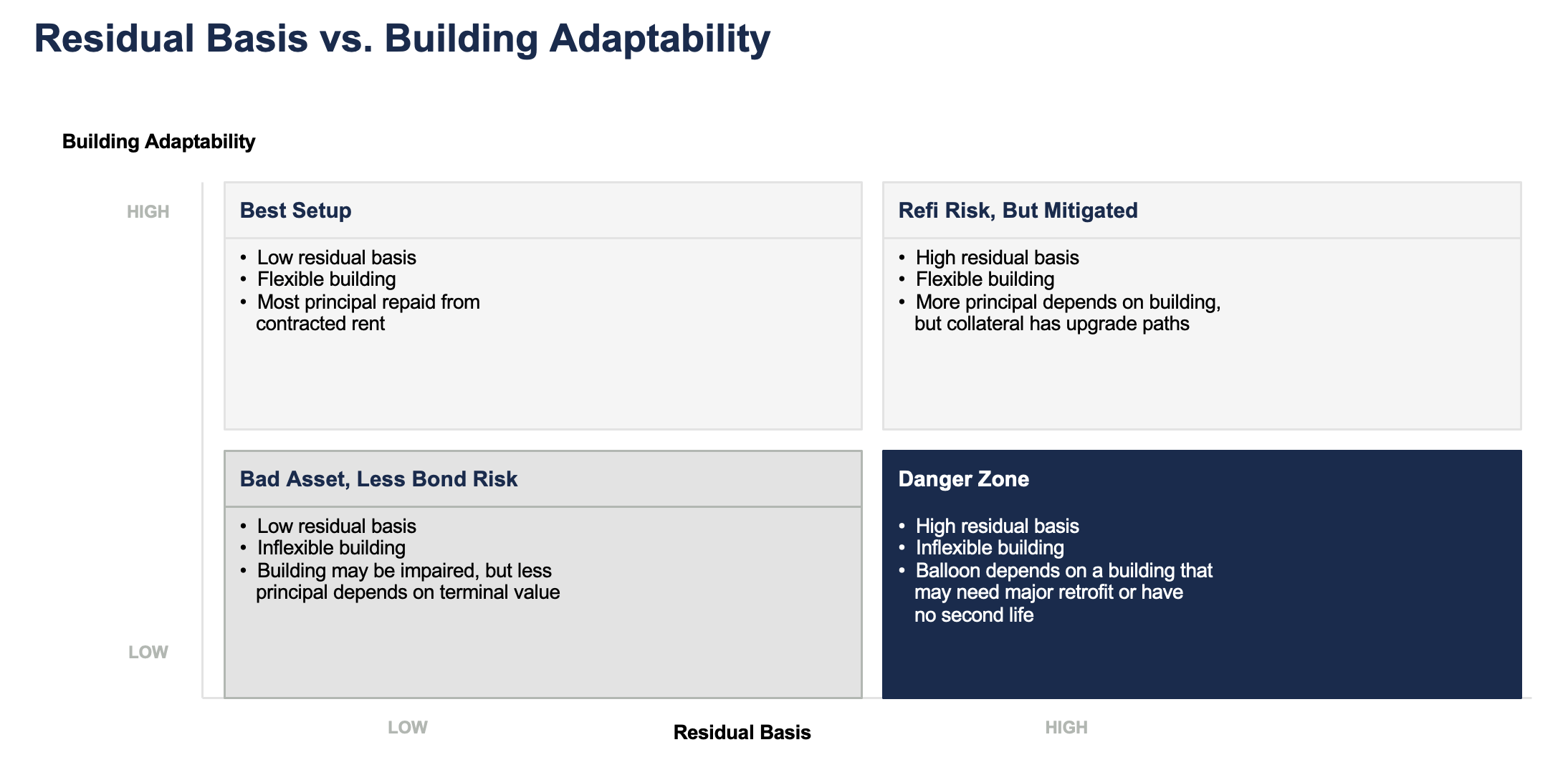

Put the two frameworks together and the sector starts to sort itself. The riskiest credit is not just the highest residual basis. It is high residual basis attached to a building with low adaptability.

Power Is Part of the Residual

The same problem shows up in power. Capital is not the binding constraint in digital infrastructure anymore, capacity is. Power, interconnection, substations, transmission upgrades, turbines, permitting, electricians, utility approvals, and local politics now decide when a site can become useful.

That turns residual risk into timeline risk, because the building cannot be refinanced on theoretical power. It needs delivered power. A building that needs more density also needs more power, and more power means more utility coordination on a schedule the lender does not control.

If the upgrade depends on interconnection, grid upgrades, switchyards, or generation capacity, then the refinancing case depends on institutions and equipment queues outside the credit agreement. Every month spent waiting on power is a month in which the maturity date gets closer. That is a very different risk from a rent roll, and it is much harder to solve with spread.

Behind-the-meter (BTM) generation is often presented as the fix, but it is better understood as a bridge with its own cost and execution risk. If a site needs a gigawatt, the sponsor may need to overbuild generation, absorb massive upfront capex, and pay for power as if the plant runs at full utilization even when the data center does not. What used to be 6 or 7 cent power can become 12 cent power before utilization, and something much higher once actual utilization is reflected.

The same is true of utility upgrades. A developer may have to fund substations, switchyards, transmission upgrades, generation interconnections, or system improvements before a site can receive the capacity it needs. What used to be a manageable contribution can become hundreds of millions of dollars, or more, paid upfront before the building produces the cash flow the financing assumes.

This is the part spreads struggle to price. You cannot price a power delay like carry, and a local moratorium is not something 25bps of spread absorbs. These outcomes are binary. Either the site gets delivered, the power shows up, and the tenant can refresh into the building, or the whole refinancing case is waiting on something outside the credit agreement.

Is the Appraisal Worth Anything?

In a normal real estate credit, the appraisal at least has a transaction history behind it. Office, industrial, multifamily, hotels, and retail all have flawed but visible comps, while data centers have much less history, especially for assets that are technologically stale.

In rated CMBS, at least one agency effectively answers that question before assigning recovery. In stress, it marks certain data center assets 30% to 50% below current appraised values, and it is careful about how much value it will credit above the rating of the tenant. That is not a universal market price, but it is a useful admission from the structured-credit process: the appraisal is not the same thing as realizable value, especially when the value rests on the building rather than the lease.

In a securitized deal you can at least see the discount. Investors can see the property value, the debt, the amortization, the residual exposure, and the rating agency stress. In corporate format, the appraisal disappears into the issuer’s balance sheet and the haircut is never struck. The same building carries the same obsolescence risk in both, but in one wrapper the markdown is explicit, while in the other it is easier for the market to ignore.

The residual is most overstated exactly where it is least visible. Plenty of corporate-format deals are priced fine, and plenty of securitized ones are not safe just because the haircut is printed. The point is narrower. The wrapper decides whether the market sees the building risk clearly or lets it disappear behind the tenant name.

Scarcity Buys Time, Not Adaptability

There is a serious argument that obsolescence is overstated, and it deserves a hearing. Power is the binding constraint in this sector, and it is choking new supply. A site that already exists, already energized, with interconnection that would take years to replicate, carries scarcity value. If you cannot build the new building, the old building keeps earning, and on that logic today’s stabilized assets may grow more valuable as the queue for new capacity lengthens.

That argument is real, but it only protects assets the market can still use. Scarcity does not turn an inflexible shell into a flexible one. It does not make an air-cooled facility liquid-cooling ready, or a low-density floor plate able to support the next rack profile, or a remote training campus useful for inference workloads that want to sit closer to users and data.

The tenant is making the same calculation. If the technology improves far enough, the hyperscaler on the lease may find itself holding more capacity than it needs, in buildings that no longer match the workload. If the lease permits assignment, the tenant may be able to hand the weakest sites to someone else. Scarcity can make the residual valuable. It cannot make every residual equal.

When There Is No Second Life

The deepest version of the problem is that these buildings often have limited alternative use. When an office tower empties, there is a conversion market, however painful, into residential or mixed use or something. A purpose-built data center campus on cheap land far from population, designed around one kind of compute, has far fewer paths. If the workload it was built for moves or shrinks, the asset does not step down in value the way a flexible building does. It can gap lower, because the only natural buyer is another operator who wants precisely what it already is.

Location decides where on that spectrum an asset sits. A facility inside a major metro, near the data and the users, has paths to a second tenant and a second use. A gigawatt campus chosen purely for cheap power, an hour from anything, has the residual of a specialized industrial site whose industry may not need it in 10 years.

The lease does not tell you which one you own. Residual basis tells you how much it matters. This is why the market needs a better vocabulary than tenant, lease term, and appraised value. Two facilities can have the same tenant and the same lease and still be radically different collateral. One is a flexible shell with power, location, and upgrade paths. The other is a purpose-built machine whose second life depends on the first workload still mattering.

When the Rent Runs Out

Residual basis told you how much of the bond depends on the building. The debate this week is whether the building will be there to depend on, in any economically useful sense, by the time the contracted rent runs out. The harder version is whether the building is still useful as-is, or whether the residual the bondholder is counting on is really another construction project waiting for funding.

No one underwriting this paper can tell you what compute looks like in five years, let alone the 10 or 15 the residual reaches for. None of that uncertainty means you should avoid the sector. It means you should know how much of your principal is riding on it, because the spread certainly is not paying you to find out.

The lease can pay perfectly and the credit can still disappoint. That is the problem with residual basis. Nobody tests it at signing. The test comes years later, when the rent runs out, the refinancing has to happen, and the building has to prove it still matters.

JBI Bulletin Board

1) Something New is Coming

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. If that’s you, or someone you’d vouch for, reply with a short note on your background.