Credit Weekly: The Capital Allocation Conflict

The same AI strategy can make the company more valuable and its existing bonds less attractive.

Amazon probably should spend another $100 billion on AI. If I was a shareholder, I might support it. If I owned the bonds, I would have a very different reaction.

That split is starting to show up across the market. Shareholders want the hyperscalers to move fast, defend their position, and spend before a competitor does. Bondholders are financing the same strategy, but their upside stops at the coupon while the funding burden keeps rising.

AI is creating different winners and losers inside the same capital structure: the company can become more valuable while the bonds get cheaper.

The Former Tech Credit Bargain

For most of the past decade, the largest technology companies were almost perfect bond issuers. They generated enormous FCF, held large cash balances and did not need much physical capital to grow. Debt came to market occasionally, usually for opportunistic reasons, and investors paid up for the scarcity.

The equity and credit stories moved together. Stronger growth produced more cash, the cash strengthened the balance sheet and the balance sheet supported tighter spreads. Management could invest heavily without forcing creditors to absorb a completely different funding profile.

AI is breaking that arrangement.

The buildouts need data centers, chips, networking equipment, power generation, etc. The companies that once sat at the asset-light end of the corporate credit universe are becoming some of its largest capital spenders. Current capex estimates at 3.2% of US GDP in 2027 and direction is clear. These businesses are becoming structurally capital intensive.

The financing has followed. AI infrastructure credit has grown into a roughly half-trillion-dollar market in less than 2 years across hyperscaler bonds, data-center financings, and leveraged credit (I mapped the market here). This issue is about a narrower question: who earns the return on all that capital, and who is simply providing it?

The Same Decision, Different Payoffs

Suppose Meta announces another $100 billion of AI spending. Equity investors may like the decision because it signals that management sees a large market and plans to move before competitors close the gap.

If the spending works, shareholders get the benefit. Revenue grows, the competitive position improves and the equity may re-rate. The bondholder receives the same coupon that was already promised.

If the returns take longer, the bondholder still financed the build. FCF falls, issuance rises and the existing curve has to absorb more paper. Meta can remain one of the safest companies in the market while its bonds widen anyway.

Traditional credit analysts are trained to ask whether the company can pay. With these issuers, the answer is usually obvious. Repayment does not settle whether the bond is attractive at its current price. A larger opportunity gives management a reason to spend faster, which pushes FCF lower and brings forward the next financing. The announcement that improves the equity story can weaken the bond technical on the same day.

Management may be doing exactly what it should do. A hyperscaler that protects near-term FCF by refusing to invest may lose its position. A hyperscaler that spends aggressively may build a much stronger company and still leave existing creditors worse off.

This is different from the traditional shareholder-creditor conflict. Historically, the transfer was easy to spot: a sponsor extracted a dividend, leverage rose and cash left the company. Here, the cash stays inside the business and may create real long-term value. Existing creditors can still underperform because most of that value belongs to the equity.

Good management is normally treated as an uncomplicated positive in credit analysis. This cycle makes that harder. The strongest management team may be the one most willing to tolerate years of lower FCF and repeated issuance to protect the franchise.

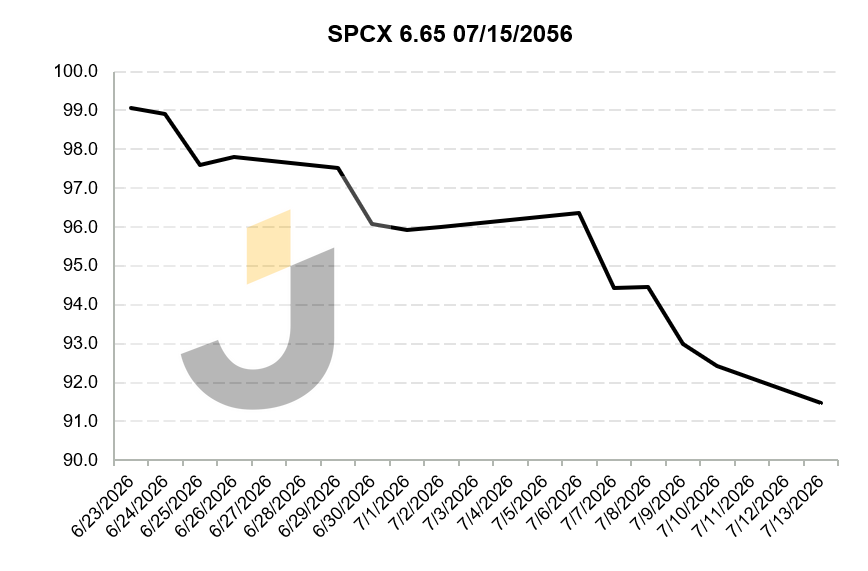

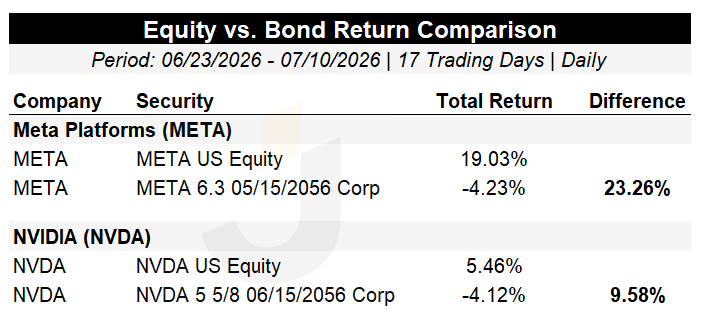

We can see that in recent performance. Meta and Nvidia equities rallied while their bonds widened. SpaceX’s long bonds fell roughly ~8 points shortly after issuance despite a massive equity cushion and IG ratings.

Amazon completed a $25 billion bond package while investors reassessed the rest of the hyperscaler complex around it. Those moves fit the capital structure: equity owns the payoff if AI works, while credit funds the route to get there.

The Capital Allocation Arms Race

Credit investors now have to underwrite several years of capital allocation, not only the current business. Revenue, margins, leverage and coverage still matter, but they can be overtaken by a spending plan that changes quarter by quarter.

The next few years of capex need to be treated almost like a separate business line.

How much spending is required to stay competitive?

How long before it produces cash?

How much debt comes first?

The current leverage ratio tells you very little if the ratio is about to change.

And the competitive dynamic makes the analysis harder. Amazon does not set its datacenter budget in isolation. Microsoft, Alphabet, Meta and Oracle are all reacting to one another, and no management team wants to be the first to decide it has enough capacity.

Each company may be making a sensible decision, while the group spends and borrows more than any one participant would have chosen in a calmer market. No management team wants to learn 3 years from now that the competitor who overspent was right. Rational behavior at the company level can still produce a poor outcome for the sector’s existing creditors.

Credit has seen this pattern before. Telecom demand in the late 1990s was real, and the internet became more important than even the bulls expected. Plenty of bonds financing the buildout still performed badly because capital arrived faster than the economics. AI does not need to fail for creditors to lose money; they may simply be funding several years of expansion at spreads that assumed the cash returns would show up sooner.

The Frequent-Issuer Discount

Large banks provide the familiar precedent. JPMorgan or Bank of America can be excellent credits and still trade wider than similarly rated industrial companies because investors know another bank deal is coming after earnings, followed by another one later in the year.

Recurring supply removes scarcity value. Buyers do not need to chase today’s bond when a newer, more liquid issue may arrive with a concession a few months later.

Hyperscalers are beginning to develop the same problem. They do not need to issue continuously to survive, but they may need to issue continuously to compete.

Take an Amazon bond trading at T+65. Amazon announces another large financing, and the new bond needs to clear at T+80. The old bond is immediately expensive against the new one and reprices even if Amazon’s earnings, ratings and leverage are unchanged.

The next deal then hangs over the curve. Investors know another concession may be coming, so the outstanding bonds do not tighten back to the prior level. Future issuance creates a higher spread floor.

This is no longer a hypothetical future calendar. 7 companies are already responsible for a remarkable share of the market’s new supply, and the spending estimates imply they are only getting started. Scarcity was part of the old technology-credit bargain. Recurring benchmark issuance is replacing it.

An exceptional balance sheet protects repayment, but it also gives management the capacity to borrow far more than a weaker company could. That capacity can become a technical problem for existing creditors.

Each new transaction makes the old bonds less scarce, and default risk is only one source of loss. If Treasury yields rise by 30bps and the credit spread widens another 50, a bond with 14 years of duration can lose more than 11 points. The analyst can be right about the company and wrong about the investment, while the issuer remains overwhelmingly money-good.

The Relative-Value Reset

This supply wave is changing the high-yield hurdle too. Amazon recently borrowed at an all-in yield of 5.3% for 10-year. This compares to BBs which yield at ~6% at the index level.

A long-duration BB issuer may offer only a modest pickup over Amazon while introducing real downgrade, default and recovery risk. Buying the hyperscaler looks obvious until the supply overhang is included.

Moving up in quality does not solve the trade automatically. High yield looks expensive vs. the all-in yield available in IG. Hyperscaler debt has stronger fundamentals, but the bonds may remain cheap because another large deal is always coming.

The comparison also affects unrelated borrowers. A portfolio manager offered Amazon, Meta, bank paper and data-center project finance at yields above 5% has less reason to stretch into a marginal BB credit.

That BB company does not need to deteriorate for its refinancing cost to rise. The alternative simply became more competitive. AI financing can tighten conditions elsewhere in credit by consuming the same portfolio capacity.

Hiring in Credit?

What the Week Said

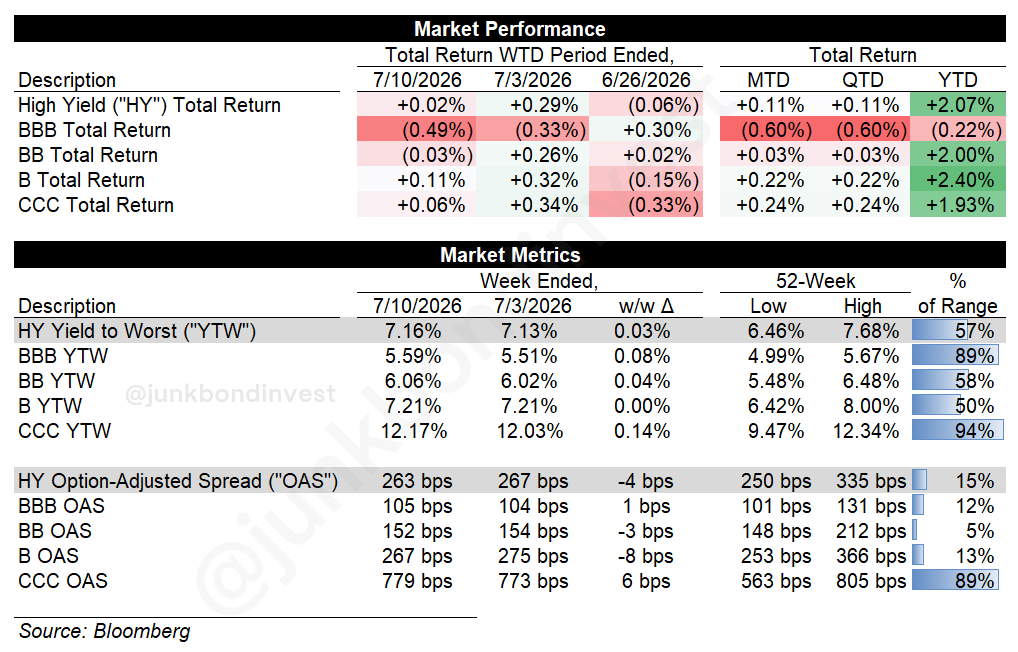

HY tightened 4bps to 263bps last week. Meta and Nvidia shares rallied as their bonds weakened, and long-duration paper from SpaceX, Meta and Oracle continued to reprice wider. The pressure was concentrated in issuers asking the market to finance the AI buildout rather than reflecting a broad flight from corporate credit.

8 of the 12 largest drags on the IG index this year are companies financing the AI buildout. Meta alone has detracted more from index returns than any other issuer. The sector financing the most exciting trade in markets is the sector losing the most money in credit.

According to PitchBook LCD, AI-related IG issuance reached $218 billion through July 8, vs. $80.5 billion during all of 2025. AI-related HY issuance added another $31.9 billion.

Amazon’s $25 billion deal cleared, but its size became part of the valuation problem for the rest of the sector. The buildout remains intact, but the market is charging more to finance it.

What to Watch

The next phase depends on whether cash returns begin catching up with capital deployed. Upcoming earnings calls at the end of this month should be read for incremental AI revenue, margins,and FCF rather than another increase in capex alone.

New-issue concessions will be equally important. If each large transaction needs wider pricing than the previous one, the market is building a structural frequent-issuer discount rather than working through a temporary supply glut. If concessions compress over the next two quarters and the curves grind back toward their old levels, this was digestion and the thesis was early.

Concentration may become the harder constraint. An investor can like Amazon, Meta, Microsoft and a portfolio of data-center bonds individually, then discover that all of them depend on the same capex cycle, power buildout and demand assumptions.

The real ratio worth tracking is incremental AI cash flow against incremental AI financing. Until the first number starts catching the second, every increase in strategic confidence gives equity another catalyst and credit another supply estimate. Hyperscalers can afford the buildout; the open question is whether their existing bondholders are being paid enough to finance it.

JBI Bulletin Board

1) Something New is Coming

The institutional version of JunkBondInvestor is coming. The list gets in first and locks the founding rate before it closes. Add your name here.

2) Now Hiring: Credit Analysts

I’m hiring credit analysts to add capacity. If that’s you, or someone you’d vouch for, reply with a short note on your background.