The Credit Investor’s Guide to SpaceX

How Bond Investors Think About the Company

SpaceX just raised $25 billion in its first trip to the bond market, and on paper the credit looks too easy to bother analyzing.

The company’s market cap sits around $2 trillion. The bonds are under 2% of that. Cash alone covers the debt more than three times over.

You would have to wipe out something like 98% of the enterprise value before a bondholder lost a dollar. On the one question that usually decides a credit, whether you get paid back, the answer is obvious.

An equity analyst would’ve stopped there. Money-good, take the spread, move on.

That is the wrong question. With a cash pile this size almost everyone gets paid, so default is not what you are pricing. You are pricing what the bond does over the years you hold it, and that looks very different at the five-year than at the thirty. Same company, five bonds, and they do not trade as one.

The gap between how this deal got bought and how it should be priced is the reason for the write-up. I’ll walk through how a credit investor looks at and prices SpaceX, tranche by tranche. Everything presented here is based on public information.

What SpaceX Actually Is

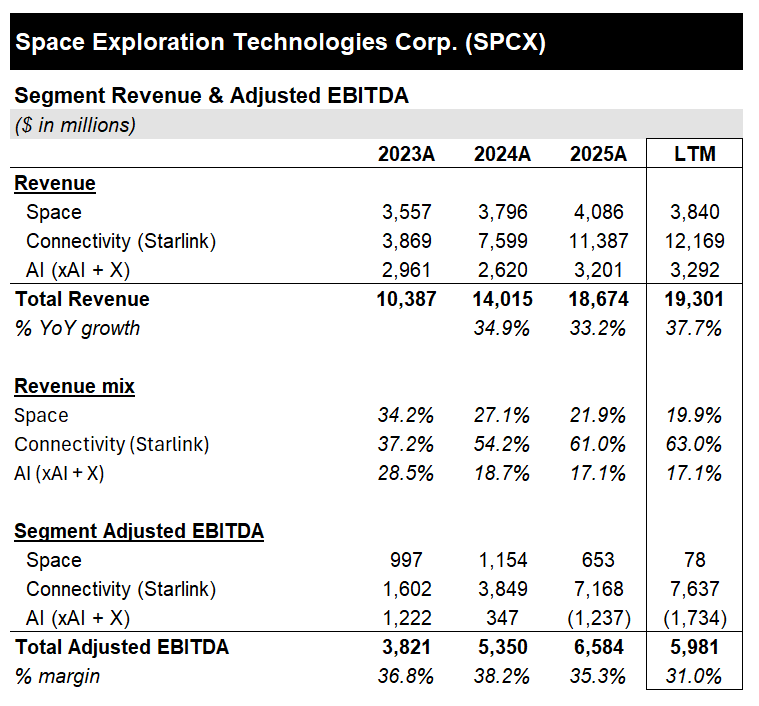

For a creditor, the relevant fact is that this is 3 businesses with different economics.

Space is the launch arm, Falcon 9 and Starship, with a near-lock on cheap access to orbit and the contracts to fly NASA and national-security payloads.

Connectivity is Starlink, around 12 million subscribers, recurring revenue, and the only part that reliably makes money.

AI is xAI, Grok, the Colossus data centers, and X; it brought in about $3.2 billion last year and lost roughly $6.4 billion doing it, per public filings, with the loss widening every year.

Revenue across all three ran about $18.7 billion in 2025. Starlink generates almost all the usable cash, AI burns it and reaches for more, and Space underneath supplies the launch capacity that makes the rest cheap. A lender is really backing the satellite business and betting the AI spend doesn’t drain the company before it pays off.

What This Deal Actually Is

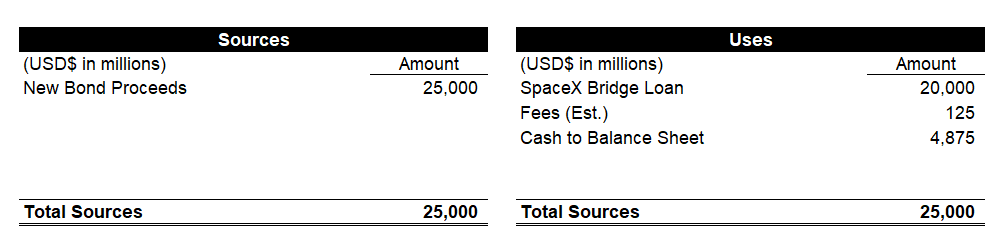

This is a refinancing first, and growth capital second. The main job is to term out a $20 billion bridge loan. The practical effect is to move Musk’s AI debt stack out of expensive short-term funding and into the IG market.

For context, the debt dates back to Twitter. Musk funded the buyout in 2022 with about $13 billion the banks couldn’t offload, so they held it for two years. Twitter became X, X merged into xAI, and xAI borrowed another $5 billion along the way. SpaceX bought xAI this February and inherited the pile.

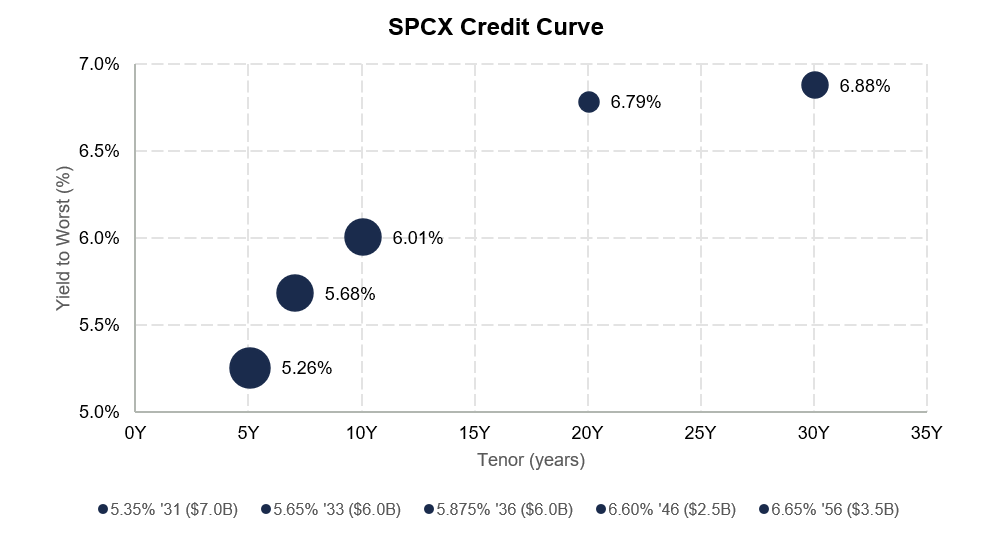

SpaceX took it out with the $20 billion bridge and these bonds repay the bridge at coupons of 5.35% to 6.65%, about $1.5 billion a year. The IG rating also buys access to the high-grade market, roughly $8 trillion deep.

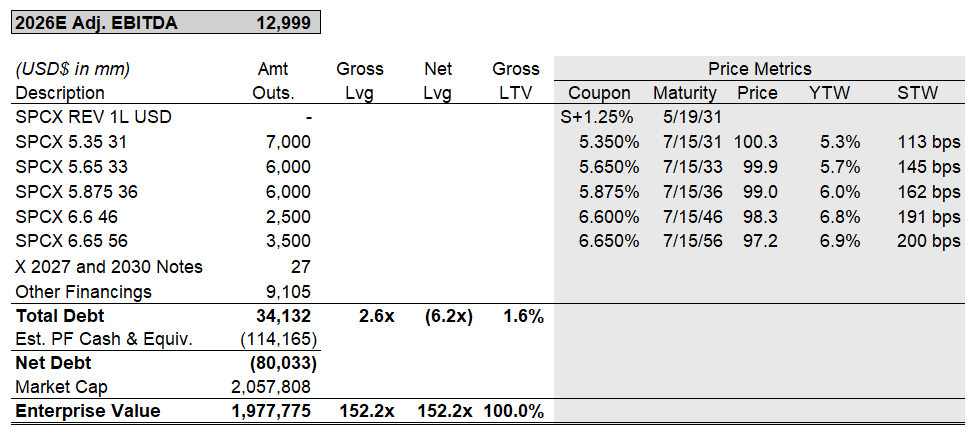

Current Capitalization

What’s Good About the Credit

Tiny loan-to-value. $25 billion of bonds under a company worth around $2 trillion, so gross LTV of about 1.6%. Even after the $600 billion drop, even haircutting the equity hard, the cushion is enormous; the bonds don’t take a loss unless the whole enterprise falls something like 98% first. That is the main reason this clears as IG.

Starlink makes money. Most of the $18.7 billion of 2025 revenue runs through connectivity, and it’s profitable and growing, with 12 million subscribers, recurring billing, and margins that widen as the network fills in. You’re lending against a real broadband franchise with runway left in enterprise, government, and direct-to-cell.

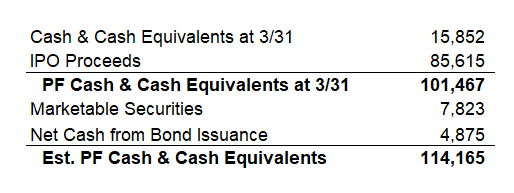

A mountain of cash. Around $114 billion against $25 billion of bonds and about $9 billion of asset financings, so roughly $80 billion net. Near-term liquidity is not the worry.

A launch near-monopoly the government needs. SpaceX puts more mass into orbit than everyone else combined, at costs nobody has matched, and flies NASA and national-security payloads. Not cash flow today, but a moat under the structure and a reason it doesn’t get competed away.

Management pulls the right levers, so far. Roughly half the capex is discretionary, so it can slow the AI buildout if cash tightens. It just raised $86 billion of equity in the IPO and pays no dividend. The agencies credit it with conservative financial policy, balance sheet ahead of payouts, which isn’t something you assume with this management.

What Worries Bondholders

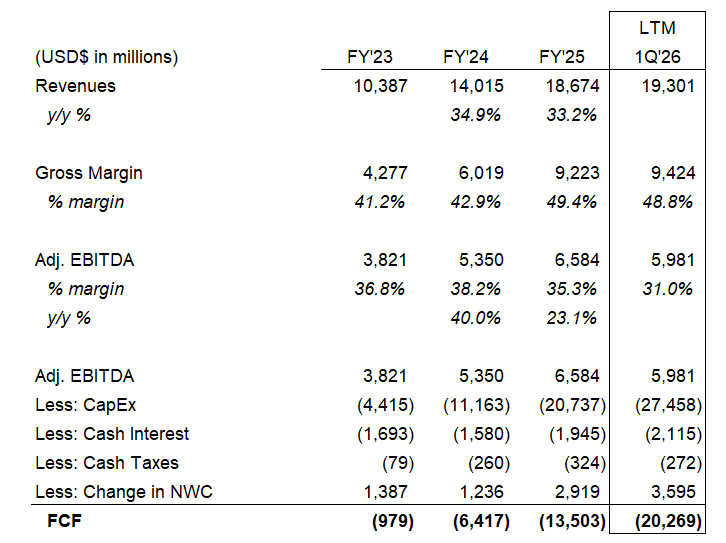

It burns cash, and will for years. No positive FCF until 2030 on S&P’s view, with the burn worsening next year and again in 2028. The cushion covers the early going. After that the company needs revenue to ramp fast and the debt market to stay open, and it needs both.

A wall of supply is coming, and the long bonds wear it. S&P’s base case takes debt to about $132 billion by 2028, and this deal landed in a record month for high-grade issuance, more than $175 billion as AI borrowers flood the market at once. Every future deal reprices existing paper wider. The long bonds are also not underwriting today’s balance sheet but the balance sheet SpaceX is trying to become, roughly five times the debt it carries now, with the AI plan still unproven.

The AI business loses billions with no proven payoff. The IG case assumes monetization arrives, through compute deals and enterprise and consumer revenue, before it drains too much cushion. You fund it the whole way and don’t get the upside if it works.

Starship has to deliver. The economics that make Starlink cheap to scale depend on Starship reaching full reusability roughly on schedule. Slip badly and the connectivity growth story, which the credit rests on, weakens.

The equity owns the upside, and the cushion moves. Your best case is getting paid back; the Mars and AI and space-data-center optionality goes to the stock. And the cushion under you is a market price that fell $600 billion in three days and bounced. It can shrink fast, right when you’d want it.

One person runs everything. Governance is weak across the board: controlled company, concentrated voting, thin oversight. Fitch was blunt about it, calling the Musk dependence a “key rating constraint.” This is someone running a $60 billion all-stock acquisition of a coding startup while the AI arm bleeds. The IG case assumes he keeps choosing the balance sheet. So far he has.

The long end has an ESG problem. Moody’s flagged emissions and on-site power around the data centers, MSCI scores the company at the bottom of its ESG scale, and desks tied some of the weak long-end demand to mandates that can’t hold the name for thirty years. Fewer natural buyers for the bonds already under the most pressure.

And it’s hard to model. Three businesses with different economics, almost no segment guidance, and agency capex and debt forecasts that span huge ranges because even they are guessing.

The credit setup is unusual: a fortress balance sheet attached to a business that still needs years of external funding. The real question is where the market is paying you for that risk, and where it is not. Across the five bonds, the answer is not the same, and that is the whole trade.