Credit Weekly: The $1.8 Trillion Credibility Crisis

Private credit's trust problem is becoming everyone's problem

🚨 Connect: Twitter | Instagram | Reddit | Job Board

You want to know what private credit really looks like right now?

Don’t read the quarterly reports. Go to the JPM LevFin conference this week and listen to what people say when they think nobody’s writing it down.

Everybody will be there. Every PM, every analyst, and absolutely every advisor.

And I guarantee the hallway conversations will be more valuable than anything said on stage. Because what people say on panels and what they say at the bar are two very different things right now.

Here are the questions that’ll be whispered over every drink at every dinner:

Are the BDC marks real?

How much software is actually hiding in these portfolios?

Is there money to be made in software credit or is it all uninvestable?

Is the AI buildout actually happening on schedule?

Start with the one everybody’s afraid to ask out loud.

The Trust Problem

Private credit doesn’t have a default problem. It has a trust problem. And trust problems are worse.

A default problem is straightforward. Loans go bad, losses get taken, the cycle plays out. We’ve seen that movie.

A trust problem means a $1.8 trillion asset class has been reporting values the market doesn’t believe. BDC stocks are trading at ~78% of net asset value. Dividend cuts of 25-35% across FS KKR, BlackRock TCP, and MidCap Financial last week. Blue Owl sold $1.4 billion of loans at 99.7 cents to fund redemptions and called it “validation” of portfolio quality, except one of the buyers was Kuvare, its own affiliated insurance entity. I broke down the full OBDC situation earlier this week:

The obvious pushback is that BDCs have traded at discounts before. Retail panics, stocks overshoot, dividends stabilize, discounts narrow. That’s the historical playbook and it’s usually been right.

But a few things about this cycle give me pause.

The dividend cuts aren’t just sentiment. They reflect a structural squeeze on the business model itself. Base rates declining means floating-rate loan income is falling. At the same time, funding costs are rising: BXSL 0.00%↑ priced a new bond at 50bps wider than comparable deals a year ago. New origination yields are compressing (TCPC 0.00%↑ reported new investments at 9.7% versus 11.1% on exits). The spread between what these funds earn and what they pay is narrowing from both sides simultaneously. That’s an earnings power problem.

Nonaccruals are also ticking up. Not dramatically. Not crisis levels. But the direction is clear and the drivers are broadening. Two weeks ago, I wrote about the sector classification problem in BDC portfolios, the software exposure hiding behind labels like “business services” and “specialty retail.” That opacity makes it harder to know exactly where the stress is concentrated. And in the public market, credit deterioration is already showing up beyond software: building products, consumer finance, specialty chemicals. If it’s happening in public credit, it’s happening in the private books too. The same sponsors, the same sectors, the same cycle.

And the redemption dynamic in unlisted vehicles is something this market hasn’t been tested on at scale. Retail funds roughly a quarter of total private credit. Unlisted BDCs offer quarterly liquidity against loans that take years to mature. Net inflows have halved over the past two years. They’re still positive. The question nobody can answer yet is what happens if they aren’t.

Does any of this mean private credit is heading for a crisis? Probably not. The macro backdrop is healthy. BDC leverage at around 1x provides real cushion. Nonaccrual rates, while rising, are still manageable.

But you don’t need a crisis in private credit for it to create problems in public markets. And that’s where this gets relevant for everyone else.

Your Problem Too

The software maturity wall is an extension risk problem. I’ve covered the A&E math, the coercive dynamics, the slow-motion impairment that never shows up in default statistics. That framing still holds. But the transmission from private credit to public markets goes beyond software.

As private credit scaled from $500 billion to $1.8 trillion, the wall between private and public markets came down. The same sponsors, the same borrower profiles, and increasingly the same institutional investors operate across both. When stress builds on one side, it doesn’t stay there.

Here’s how it works.

When BDCs are managing redemption pressure, cutting dividends, and watching their stocks trade at 23% discounts to NAV, they start to get selective about what they’re willing to hold and refinance. Credits that would have been seamlessly renewed through private channels six months ago are now getting pushed back on. Tighter terms. Lower advance rates. Requests for sponsor equity. The sponsor’s banker runs the math on a syndicated deal instead. The borrower moves from private to public not because private credit broke, but because the relationship got harder.

That adds supply to public HY and loans at exactly the moment appetite for lower-quality paper is weakest.

The spillover isn’t dramatic yet. If private credit were truly hemorrhaging into public markets, you’d see far more damage. But the pressure is directional and building.

And then there’s the channel nobody can size. Insurance companies have been building private credit exposure not just through direct lending allocations but through structured vehicles that repackage PC loans into IG wrappers for favorable capital treatment.

If underlying loans deteriorate enough to impair those vehicles, insurers face capital charges they didn’t plan for and start selling liquid assets to rebalance. I’m not saying this is imminent. But the fact that nobody can confidently size this exposure is itself a risk the market hasn’t assigned a premium to.

None of these channels is overwhelming on its own. But they all push in the same direction. And they’re all active simultaneously.

The Rip Current

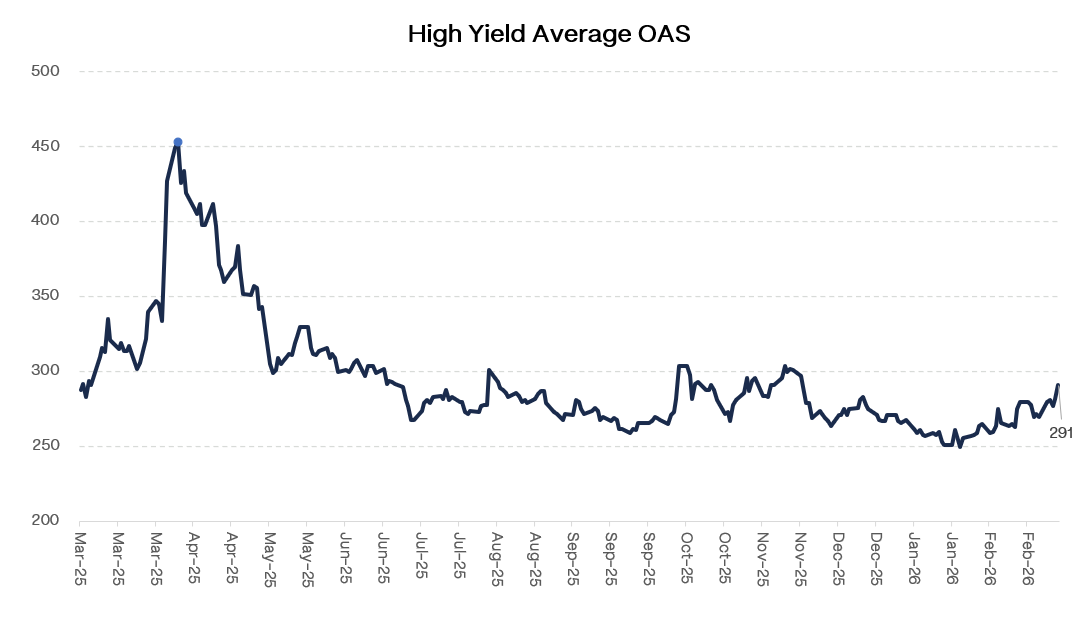

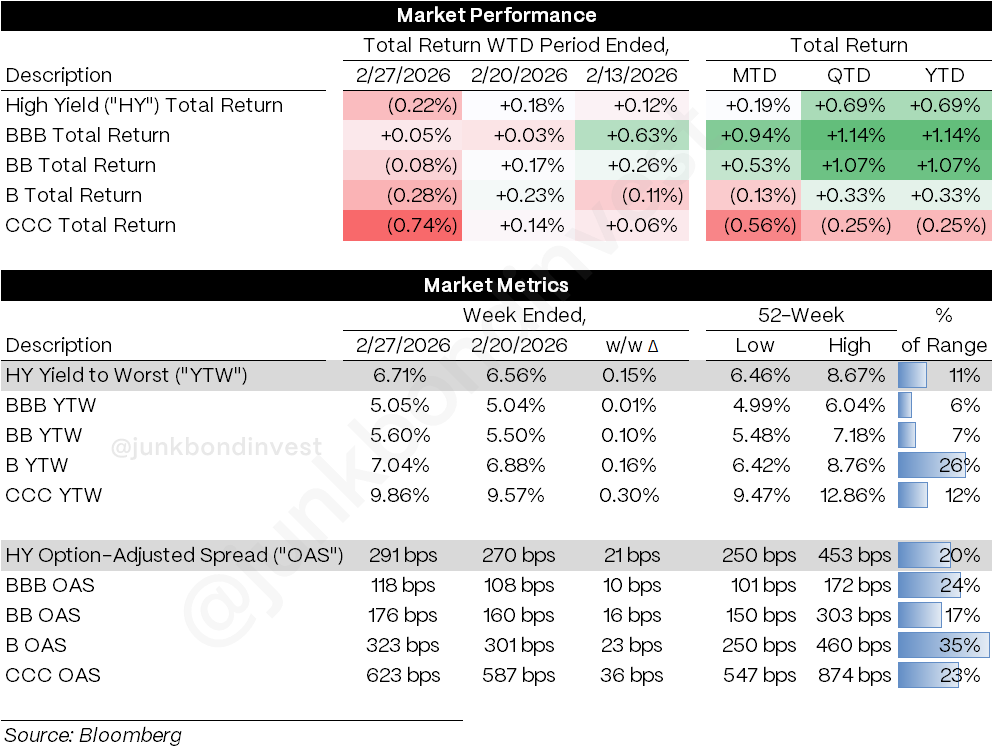

HY spreads widened 21 bps on the week to 291. The biggest weekly move in months. But it wasn’t even the real story.

CCC spreads blew out 36 bps on their seventh consecutive week of widening. CCC total return was -0.74% on the week, -0.56% on the month, and now -0.25% YTD.

I’ve been saying the index is lying to you. It’s gotten worse. The gap between BB and CCC spreads is now 447 bps and accelerating. HY is still positive YTD at +0.69%. But that number is carried almost entirely by BBs. The lower half of the quality stack has been bleeding for weeks. Loans were worse than bonds. CCC loans posted their seventh consecutive negative week. Default rates are rising and broadening beyond software into cyclical sectors.

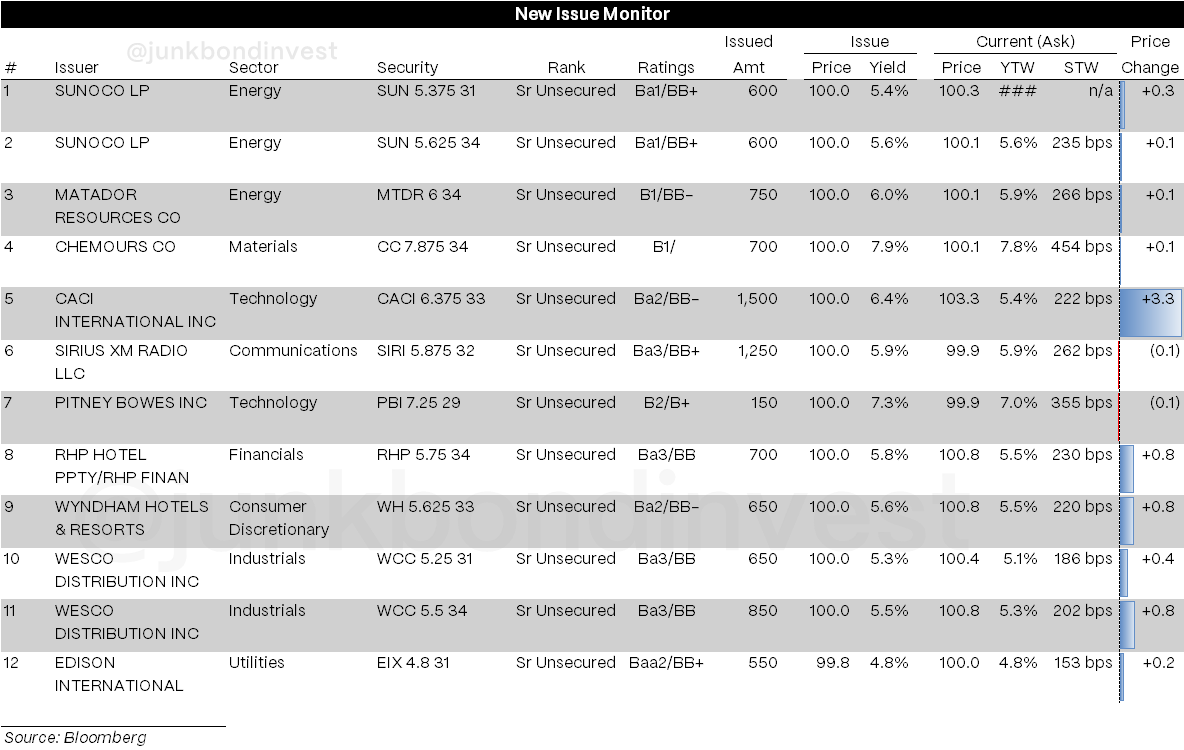

The new issue market is telling the same story. Look at what priced this week: Sunoco. Matador. Chemours. Sirius XM. Wesco. Edison. Almost entirely BB and strong single-B. Energy, industrials, defense. Refinancings. Pitney Bowes was the only deal that showed friction, pricing its 7.25% notes at 99.9 after trimming the deal. Every other issuer came, priced clean, and traded up.

Two primary markets. Still running in parallel.

Tangible vs. Terminal

Step back from the mechanics and a larger rotation comes into focus.

The market is differentiating hard between businesses with tangible assets or defensible positions and businesses leveraged on the assumption their competitive moat was permanent.

I covered the software dynamics in detail last week: The terminal value problem, the capability curve, the maturity wall. All of it accelerated this week. IGV dropped 5% Monday. Rallied 7% off the lows by Friday. Bonds in the same names swung 3-5 points. Several private issuers reported earnings ahead of schedule to calm lender nerves.

One thing worth sitting with: tech sector P/E multiples have converged to consumer staples levels. That convergence historically only happens during broad risk-off events. It’s happening now with indices near highs. The equity market is making a statement about the terminal value of these business models that goes beyond a cyclical earnings dip. Whether credit has fully absorbed the implications of that statement is a question every PM holding leveraged software should be asking themselves.

Worth remembering that only 1% of S&P companies have actually quantified AI’s impact on current earnings, which means both the selloff and the rally are trading on narrative.

Building products is the sector that deserves more attention than it’s getting. One of the largest distributors in the space saw its bonds drop 8+ points this week. No AI angle. Just cyclical deterioration. Soft housing. No policy support. PE-backed structures leveraged for a rate environment that never materialized.

The fact that old-fashioned credit stress is emerging alongside the AI disruption narrative tells you the cycle is broadening. That should matter more to you than another software headline.

Energy is the mirror image. Cleanest balance sheets in leveraged credit. Under-owned according to sellside positioning surveys. New issue activity this week confirms it. Sunoco and Matador both priced clean and traded up. Iran adds a geopolitical premium to a sector that was already fundamentally sound.

War, Inflation, and the Circular Chain

On Friday night the US and Israel launched Operation Epic Fury, a major air campaign targeting Iranian missile forces, naval assets, nuclear infrastructure, and leadership network. Khamenei was later confirmed dead.

No strikes on energy infrastructure so far, which is the key detail limiting near-term disruption to physical oil flows. But tankers are slowing through the Strait of Hormuz and even without a physical outage, operational disruptions could temporarily remove the equivalent of millions of barrels per day from effective supply. Higher oil prices are reasonable if operations are sustained. Escalation to energy infrastructure is a different world entirely.

The credit relevance isn’t the oil price itself. It’s the chain reaction. Energy tightening feeds producer prices (PPI just printed the hottest since September). Sticky inflation keeps the Fed on hold. Higher-for-longer rates mean continued pressure on floating-rate borrowers, which feeds right back into the private credit stress we started this letter with. The chain is circular.

I’ve been arguing that the pain trade for 2026 is reacceleration, not recession. Iran makes that thesis stronger. The US is effectively running two economies:

One is the AI/infrastructure complex, investing $650 billion this year with expected returns so high that interest rates are irrelevant.

The other is everyone else: hiring stalled, housing frozen, consumer sentiment scraping. The Fed has one rate for both. Too low for the first. Too high for the second. The quality gap in HY is the credit market pricing this divergence.

The forward curve is pricing rate cuts that would require a disinflation impulse nobody can identify in the current data. Core inflation has been stuck above target for over two years. The 10-year broke below 4% this week on a flight-to-quality move. That looks like a fear trade to me.

AI workloads are consuming an increasing share of global electricity and the infrastructure to support them is behind schedule: only a third of planned 2026 data center capacity is actually under construction. That demand is tightening energy markets at the margin, feeding the same inflationary pressure that Iran is compounding from a different direction.

Private credit stress, AI disruption, geopolitical risk, sticky inflation. Four forces that look unrelated but feed into each other in ways the market is only beginning to price.