Blue Owl Capital Corporation ($OBDC): The 24% Discount That Isn't

A fundamental analysis of the most controversial BDC

Two weeks ago, Blue Owl reversed course on OBDC II. No more quarterly redemptions. Capital gets returned through periodic distributions funded by asset sales and loan repayments.

In other words, your money comes back on their terms, not when you want out.

The market didn’t buy it. OWL shares dropped ~6%. Every major alternative asset manager got dragged down on contagion fears. Elizabeth Warren started talking about cockroaches. Mohamed El-Erian invoked August 2007. The SEC had already put private credit on its 2026 examination list. And then Boaz Weinstein showed up with tender offers at 20% to 35% discounts to NAV.

Which brings us to Blue Owl Capital Corporation. Ticker OBDC 0.00%↑. The flagship public BDC. The one every sell-side analyst says to buy.

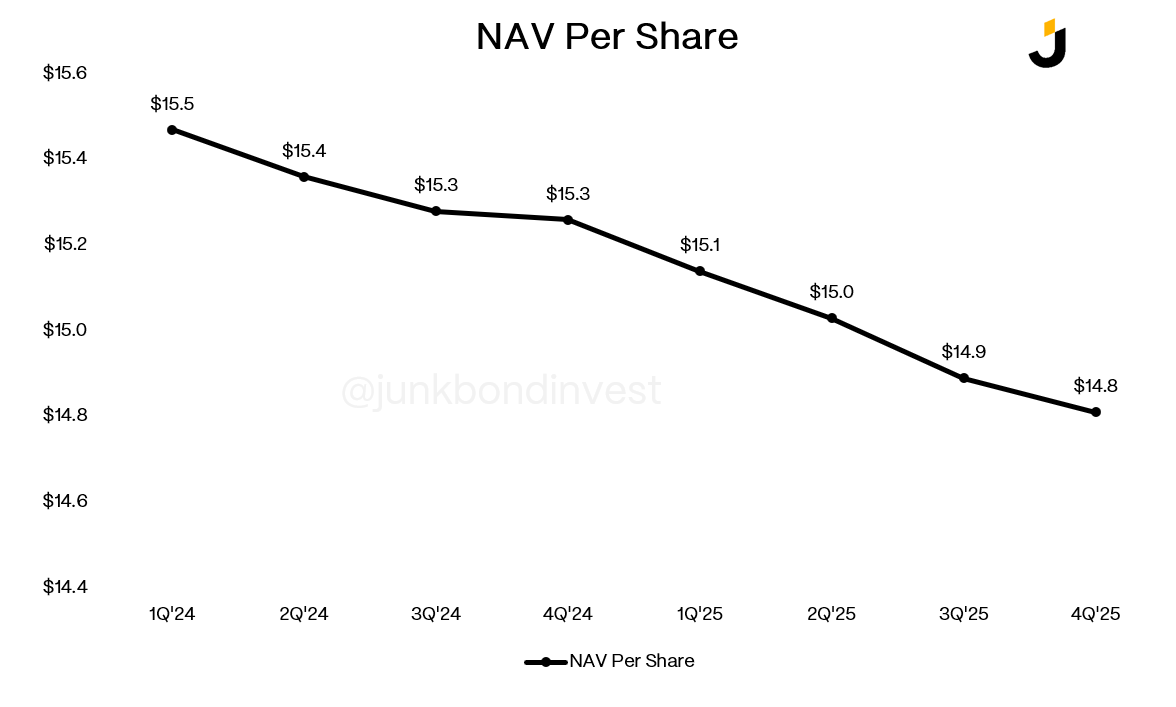

$11.29 a share. Reported book value of $14.81. A 24% discount. 12% yield. 234 companies across 30 industries. 79% senior secured. The average 12-month price target is $13.92. Basically every analyst covering this stock has a Buy or Outperform.

So why is the market price a significant discount to NAV?

Because the market knows something the analysts won’t say. That 24% discount to book value? It’s the market telling you something is wrong.

Let me show you what exactly.

The Reported NAV Is Stale

First, the marks everyone quotes are as of December 31, 2025.

OBDC’s portfolio comprises Level 3 assets, meaning there is no active market and the fair values come from models controlled by the manager. The marks are updated quarterly. The next update, as of March 31, won’t be published until May.

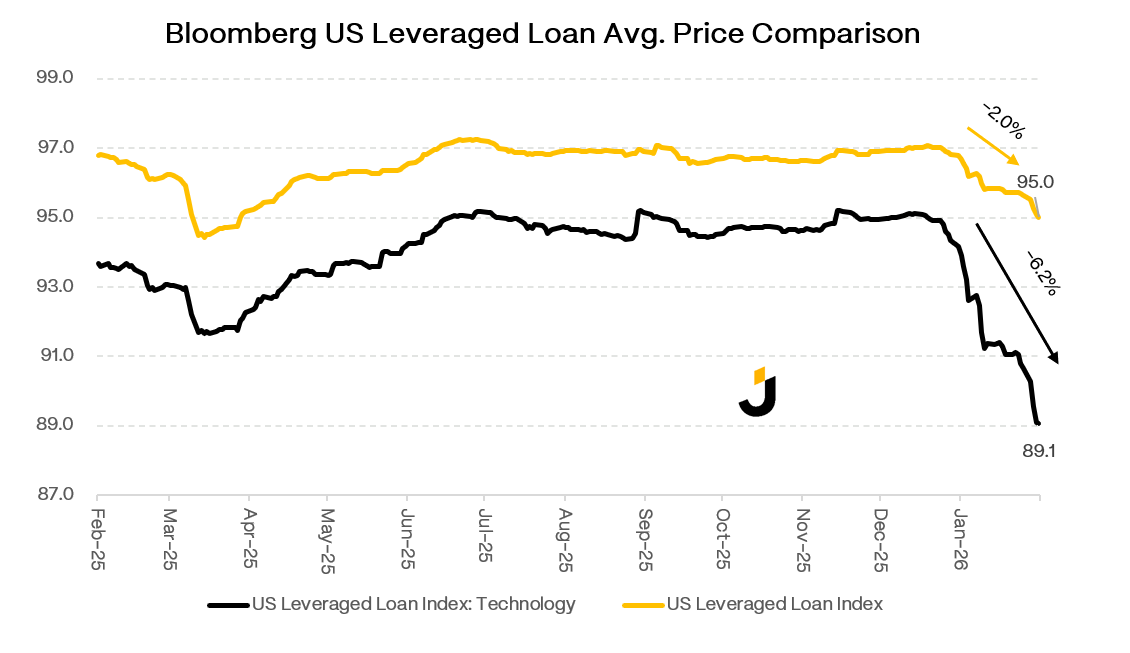

Since December, the leveraged loan market has sold off meaningfully. The average price for the Bloomberg US Leveraged Loan Index is down 2.0% YTD. The software sub-index average price is down 6.2%. These are syndicated loans, not private credit, and the two markets are not identical. Private credit was generally originated at wider spreads, and syndicated loans are subject to technical selling pressure from CLO formation slowdowns and retail fund outflows.

But the borrowers are structurally similar: PE-sponsored, leveraged buyouts of middle-market companies. $34 billion of direct loans refinanced into the BSL market in 2025 alone. The wall between these markets is thinner than it used to be.

Here is what this looks like at an issuer level: