Weekend Minutes: HY Market Recap (September 27, 2024)

A Brief Recap of Last Week's High Yield Market Performance

🚨 Connect with me on Twitter / Instagram / Threads | Estimated Read Time: 5 Minutes

The high yield market experienced a surge in activity last week, as issuers capitalized on the recent Fed cut. Last week saw high yield bond issuance exceed $8 billion, pushing September’s total to a remarkable $34 billion—the highest monthly volume since September 2021 (we’re SO back). This flurry of activity comes as borrowers rush to secure funding ahead of potential volatility surrounding the upcoming US election. Let’s dive into the details of this eventful week.

Weekly Performance Recap: Issuance Surge Amid Rate Cut Aftermath

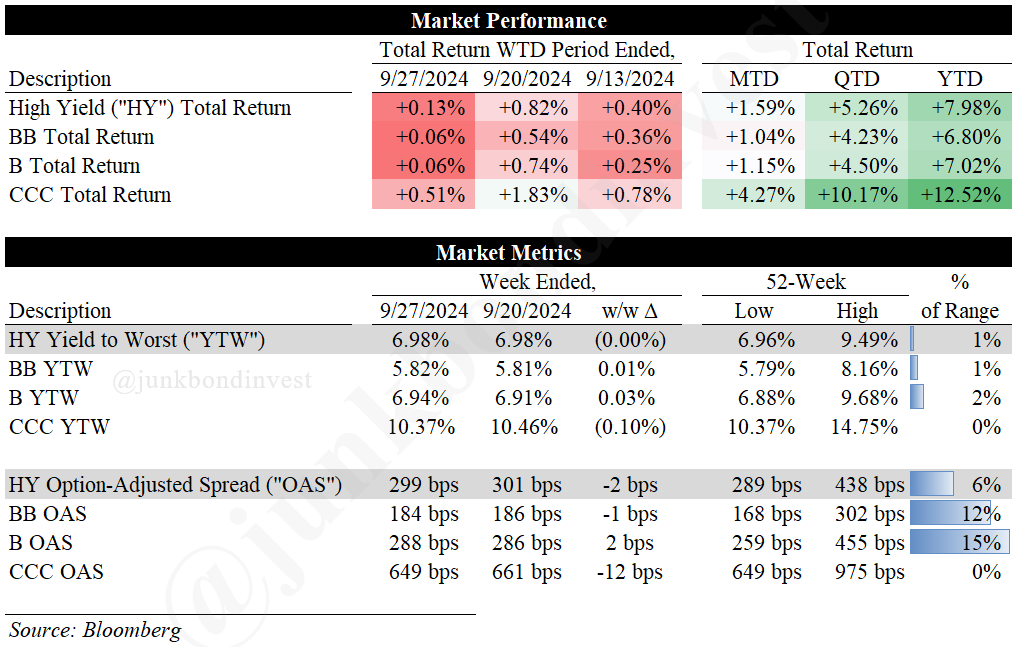

For the week ended September 27th, the high yield market showed modest gains, with the overall index returning +0.13%. This brings month-to-date returns to +1.59% and year-to-date returns to a solid +7.98%. With another quarter left in the year, it’s not out of the question to see full-year returns exceed double digits!

Breaking down performance by rating category:

BBs returned +0.06%, bringing YTD returns to +6.80%

Bs also returned +0.06%, with YTD returns now at +7.02%

CCCs continued to outperform, returning +0.51% for the week and pushing YTD returns to an impressive +12.52%

The persistent outperformance of CCCs is particularly noteworthy, as they continue to widen the gap against their higher-rated counterparts.

Noteworthy Market Metrics:

The overall YTW for the HY market held steady at 6.98%, unchanged from the previous week.

Option-adjusted spreads (OAS) tightened slightly by 2bps to 299bps, now sitting just 6% above their 52-week low.

The percentage of bonds trading above par increased to 36%, up from 29% a month ago.

The telecom sector led monthly returns with a +3.4% gain, while cable/satellite topped the list at +4.0%.

CCC spreads have tightened by 124bps in September, compared to 7bps and 4bps widening for BB and B spreads, respectively.

Year-to-date issuance now stands at $232.78 billion, a staggering 73% increase from the same period last year.

Primary Market Activity

Last week’s primary market activity was dominated by refinancing efforts, with 10 out of 16 tranches proposed as secured debt (the most since February). The surge in issuance reflects issuers’ eagerness to lock in favorable rates following the Fed’s recent 50bps cut. Notably, six of the 16 issues were drive-bys, highlighting the opportunistic nature of current market conditions.

Standout Transactions:

Cable & Wireless’ $1 billion offering of eight-year senior secured notes, upsized from $500 million, priced at par to yield 7.125%. This BB-/Ba3/BB- rated deal will refinance existing debt, including a full redemption of 2027 notes.

Multi-Color Corporation’s $950 million offering of seven-year senior secured notes priced at par to yield 8.625%. This B3/B- rated deal will redeem existing 2026 notes and partially repay ABL borrowings.

Windstream Holdings’ $800 million offering of seven-year first lien notes priced at par to yield 8.25%. Proceeds from this B3/B- rated deal will repay term loans.

Wayfair’s $800 million offering, upsized from $700 million, of five-year senior secured notes priced at par to yield 7.25%. This B1/BB+ rated deal aims to refinance a portion of the company’s outstanding convertible notes.

Post Holdings’ $600 million offering of ten-year senior unsecured notes, upsized from $500 million, priced at par to yield 6.25%. This B2/B+ rated deal marks the first 10-year bond issuance since May, signaling investor appetite for longer-dated paper.

Secondary Market Dynamics

The secondary market showed mixed activity this week as investors processed the recent rate cut and new economic data. Cash bond prices drifted and stocks retreated from record highs, while Treasury yields and high-yield spreads fluctuated in response to economic indicators.

Key economic data influencing the market included:

Weekly jobless claims fell to 218,000, below expectations and marking the lowest level since May.

Consumer confidence dropped to its lowest point in over three years, raising concerns about future consumer spending.

Looking Ahead

As we approach the end of the quarter, market participants remain focused on upcoming economic data and potential Fed moves. The strong issuance volumes suggest continued appetite for high yield debt, but investors should stay alert to potential volatility as we near the U.S. presidential election.

Key factors to watch include:

Upcoming jobs reports, which could influence the Fed’s November decision. Current market pricing implies a 40% probability of another 50bp cut in November.

Any signs of economic slowdown that might impact corporate earnings.

Geopolitical developments that could affect market sentiment.

With September issuance reaching a three-year high and the market demonstrating resilience, the high yield space appears to be firing on all cylinders. However, the sustainability of this momentum will depend on a delicate balance of economic factors and policy decisions in the coming months.

Find the most recent JunkBondInvestor posts below

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.