HY Market Weekly Minutes: Spreads Rally to Fresh Tights as Trump Win and Fed Cut Fuel Risk-On Move (November 8, 2024)

A Brief Recap of Last Week's High Yield Market Performance

🚨 Connect with me on Twitter / Instagram / Threads | Estimated Read Time: 5 Minutes

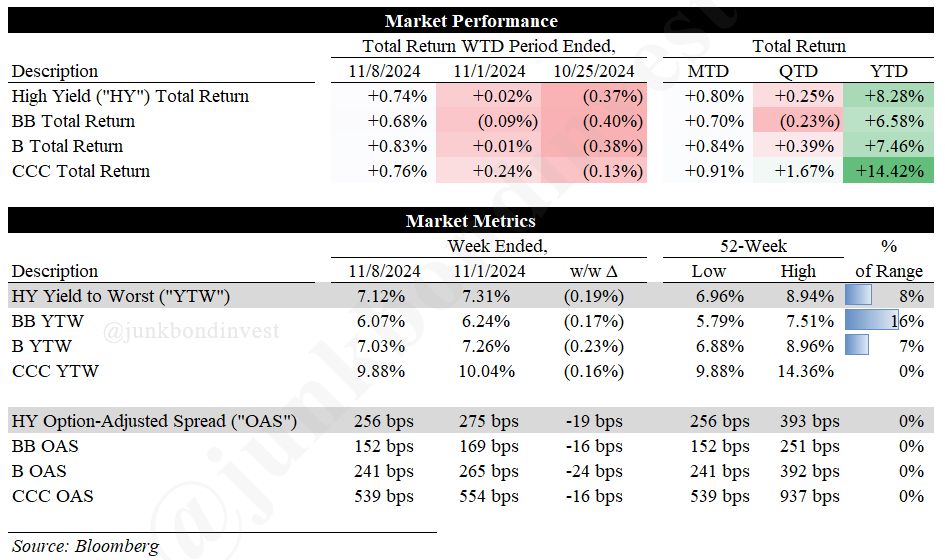

The high yield market delivered a powerful post-election rally last week, shrugging off both political uncertainty and rate volatility. Spreads compressed dramatically across the ratings spectrum, with the overall HY market tightening 19bps to 256bps—the tightest level since 2007! The technical picture proved resilient even as Treasury yields whipsawed on the combination of Trump’s victory and the Fed’s 25bps rate cut.

The market’s risk appetite was particularly evident in the performance data, with high yield delivering its strongest weekly gain since March at +0.74%. Even more telling—the rally was broad-based across the ratings spectrum with BBs gaining +0.68%, Bs up +0.83%, and CCCs maintaining their momentum at +0.76%.

Unsurprisingly, primary market activity nearly ground to a halt with just one deal—Jostens’ $500 million secured offering backing a dividend to Platinum Equity. The fact that the lone deal of the week was a dividend recap suggests the technical backdrop remains extraordinarily supportive.

Let’s dive in.

Weekly Performance Recap

For the week ended November 8th, the high yield market staged an impressive rally, with the overall index returning +0.74%. This brings MTD returns to +0.80% and extends YTD gains to +8.28%. More significantly, option-adjusted spreads (OAS) compressed a remarkable 19bps to 256bps, reaching levels not seen since before the GFC.

This strong performance came amid two major catalysts: Trump’s election victory and the Fed’s widely expected 25bps rate cut, bringing the target range to 4.50-4.75%. Chair Powell maintained a balanced tone, noting that while policy remained restrictive, the Fed would continue monitoring both sides of its dual mandate.

The market’s outperformance was particularly notable in the context of broader risk assets, with the S&P 500 delivering its best week of 2024 at +4.8%. Even more striking—high yield spreads are now through their 2007 tights for BBs, with single-Bs not far behind. CCCs have rallied dramatically from August highs of 890bps to just 539bps, delivering an impressive +8% return over the past three months. The CCC/BB ratio currently sits at 3.5x, suggesting further compression potential despite the rally.

Primary Market Activity

Primary issuance slowed to a crawl this week as markets digested the election results, with just one deal hitting the market. The sole transaction came from Platinum Equity-owned Jostens, which launched a $500 million seven-year secured note offering to fund a dividend to its sponsor. The notes traded up +2.5 following issuance.

Secondary Market Dynamics

The secondary market saw dramatic moves as investors aggressively positioned for “Trump trades” following the election. The VIX posted its second-largest one-day drop since 2021 as clarity around the election triggered a compression squeeze across risk assets. High yield spreads hit fresh tights even as the 10-year Treasury yield surged to 4.47% following stronger-than-expected services data.

The price action suggests investors are increasingly focused on policy-driven opportunities rather than traditional credit metrics, with some CCCs now trading just 100bps off their 5-year tights and nearly 300bps inside their 5-year averages. Several issuers and sectors saw dramatic moves on company-specific news and potential policy implications:

iHeartMedia bonds surged after the company announced a major balance sheet restructuring supported by approximately 80% of its creditors. The news drove significant gains across the capital structure.

Private prison operators rallied sharply on expectations of renewed federal contracts under Trump immigration policies.

E.W. Scripps bonds plunged 12 points after Q3 results disappoined investors hoping for asset sale news.

Renewable energy names underperformed, with Sunnova bonds falling on potential IRA revision concerns under a Republican administration.

Looking Ahead

All eyes turn to next week’s October CPI report as markets digest the implications of Trump’s victory and the Fed’s latest rate cut. While economists expect core CPI to accelerate slightly to 0.34% month-over-month, the broader economic backdrop remains resilient. Third quarter GDP surprised to the upside at 2.8%, powered by robust consumer spending growth of 3.7% and an impressive 11% surge in equipment investment. Even more encouraging, productivity growth continues its upward trend, with the five-year average now at 1.9%—well above pre-pandemic levels.

The market reaction to Trump’s victory has been notably bifurcated. Risk assets have surged on expectations of deregulation and growth-friendly policies, particularly in energy and financial services sectors. However, the rates market has shown more restraint—while 10-year yields briefly touched 4.5%, they’ve settled back to 4.3% as investors weigh the inflation and deficit implications of Trump’s proposed agenda.

The technical picture suggests investors are currently focusing more on the growth opportunities than the inflation risks. With spreads at post-crisis tights, equity markets delivering their best week of 2024, and the VIX posting its second-largest one-day drop since 2021, markets appear to be taking an optimistic view of the growth/inflation trade-off ahead.

The next few weeks should reveal whether this rally has staying power or if markets have gotten ahead of themselves. The combo of key economic data and early signals about policy priorities from the incoming administration will help determine if current spread levels are justified or if investors need to reprice for a more complex reality ahead.

Jobs in Credit:

💡 Have a job opening you’d like to share here? Shoot me a message.

Find the most recent JunkBondInvestor posts below

Rivian Automotive’s ($RIVN) Busted Convertible Bonds: High-Stakes Opportunity in a Crowded EV Market

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.