Electrode Economics: Avoid GrafTech's Secured Bonds

Insights into GrafTech International's Strategic Financial Planning in an Unpredictable Electrode Industry

Situation Overview:

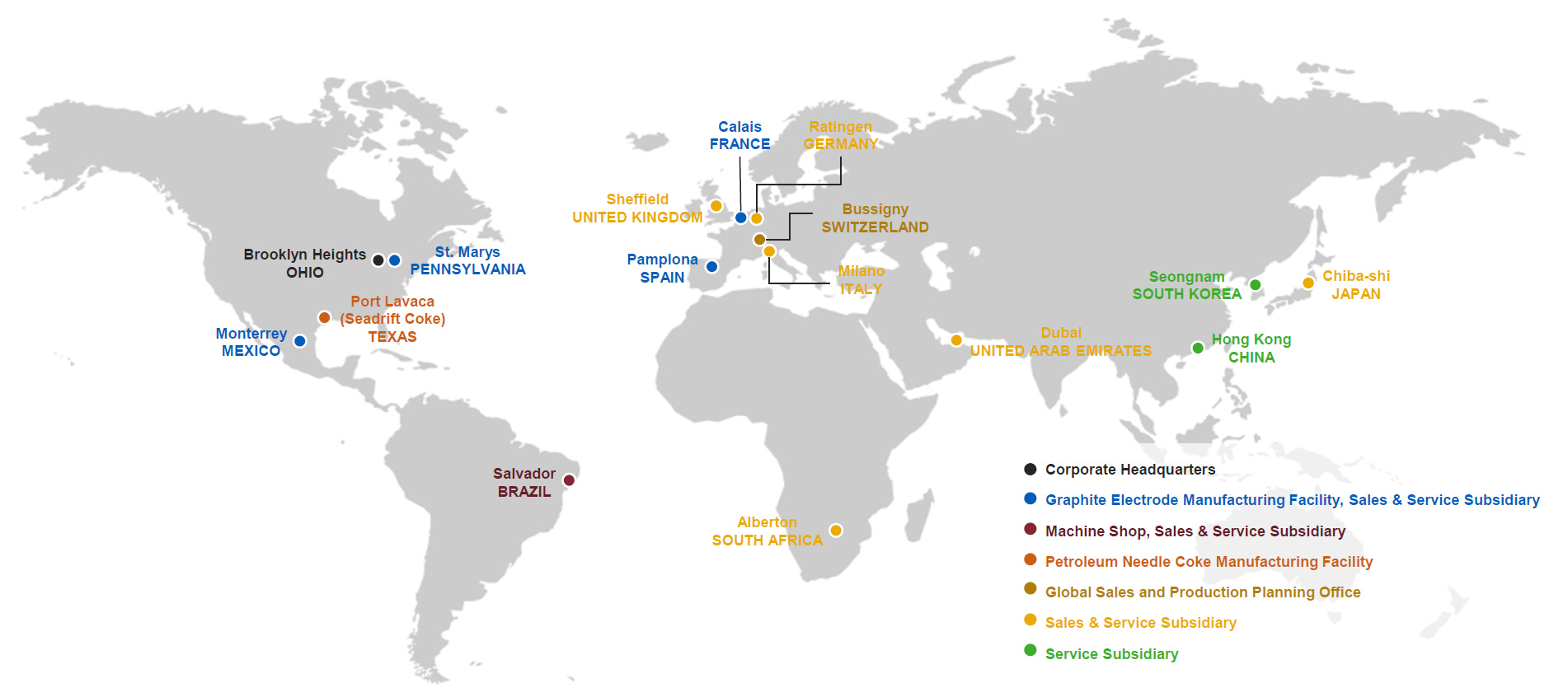

Headquartered in Brooklyn Heights, Ohio, GrafTech International Ltd. (“GrafTech” or “EAF”), is a vertically integrated manufacturer of graphite electrodes, a key component in the production of steel using electric arc furnaces (“EAF”). With operations in more than 50 countries, the company’s ultra-high power graphite electrodes are manufactured primarily at 4 facilities located in France, Spain, Mexico, and the US, with total annual production capacity of 2021 thousand metric tons.

The company is unique in that it is the only large-scale, vertically integrated producer, controlling its own supply of petroleum needle coke, a key raw material, which gives it an advantage in producing high-quality electrodes in a cost-efficient manner. GrafTech’s products are used in a variety of industries, including steel production, electronics, and energy storage. Acquired for $1.25 billion in 2015 by Brookfield, the company was taken public in 2018 and is currently listed on the NYSE under the ticker EAF.

The business is highly cyclical and experiences a high degree of fixed cost operating leverage. To alleviate the inherent volatility in electrode market prices, between 2017-2019, the company entered into 3-5 year, take-or-pay contracts (“LTA”) with customers when market prices experienced a surge. The chart below can probably explain to you the entire credit story in one picture. Now that the LTA contracts are beginning to roll-off, can you guess where spot prices are currently?

To nobody’s surprise, current graphite electrode market prices are substantially below their contracted LTA prices. As these have rolled-off, profitability and FCF have come under pressure. Recently, the company’s realized market prices were lower than its cash operating costs, resulting in -$22 million of Adj. EBITDA in 4Q’23. For the entire year, Adj. EBITDA totaled just $20 million. This compares to Adj. EBITDA of $536 million in FY’22 and $1.2bn at the peak in FY’18, all on substantially the same production capacity.

The decline in prices began when the global steel industry was negatively affected by the trade war in 2019. This was further exacerbated by an oversupply of cheaper electrodes from China as well as a demand shock during the COVID-19 pandemic. Currently, graphite electrode market prices stand at multi-year lows driven by diminished steel production, particularly in Europe where elevated energy costs and subdued industrial demand are impacting steel production. While the US market has shown some resilience, there has been a decrease in utilization rates compared to previous years. At the same time, decreased production of EAF steel in China is leading to an increase in electrode exports, exacerbating the downward pressure on graphite electrode prices. This dynamic is unlikely to change in 2024 as an ongoing steel surplus from China and India, coupled with weak worldwide demand, is likely to keep spot prices for graphite electrodes under strain throughout the year.

In response to the weak current market environment, EAF has revealed a plan to enhance FCF through various cost-saving measures. This plan includes significantly scaling back operations at its St Marys plant and cutting both overhead costs and graphite electrode manufacturing across other sites. Additionally, GrafTech has planned to reduce capex and is exploring opportunities in the lithium-ion battery market for electric vehicles, including filing a permit application for expansion at its Seadrift facility. Despite the weak market environment, management remains positive on the industry’s long-term outlook. This outlook is buoyed by expectations that the steel industry decarbonization efforts will continue to drive continued share growth for EAF method of steel production, thereby driving increased graphite electrode demand, ultimately lifting prices.

Nonetheless, at current earnings levels, the company’s capital structure is clearly unsustainable. Fortunately, debt maturities are not until 2028 which means refinancing is not a major consideration at the moment. However, negative EBITDA coupled with other fixed charges has resulted in negative FCF, putting the company’s liquidity in focus. While the company’s liquidity provides some runway, should prices drift lower, this buffer may quickly be drained and EAF may seek additional financing.

These market challenges have also been reflected in the prices of EAF’s securities. Currently, EAF’s secured bonds trade in the mid 60-70s (depending on tranche), implying a YTM of 14-17%.

In the next section, I will review the company’s capital structure, financials, and covenant considerations. If you are currently involved and looking to double-check your analysis or stress-test your thesis, I’ll also provide my opinion on the secured bonds at current trading levels.

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.