Can GameStop ($GME) Actually Buy eBay ($EBAY)?

The financing structure, the dilution math, and what it means for eBay's existing bonds

You saw the interview. Everybody saw the interview.

Sorkin asked the question three times. How does the math work? Eleven billion market cap, nine billion of cash, twenty billion highly confident letter from TD.

The deal is fifty-five.

Cohen’s answer: “I don’t understand your question.”

He understood the question. The deck answers the question. Sorkin walked through the math himself on air before he asked it the second time. Cohen still wouldn’t say it.

But while the financial press argues about how and whether the deal closes, they aren’t asking the question that decides everything else. Will the leveraged finance market clear this paper? At what yield? With what structure? Not whether Cohen wants to do the deal. Whether credit investors will absorb the deal he’s proposing.

And perhaps the more important question: is it enough?

The Proposal

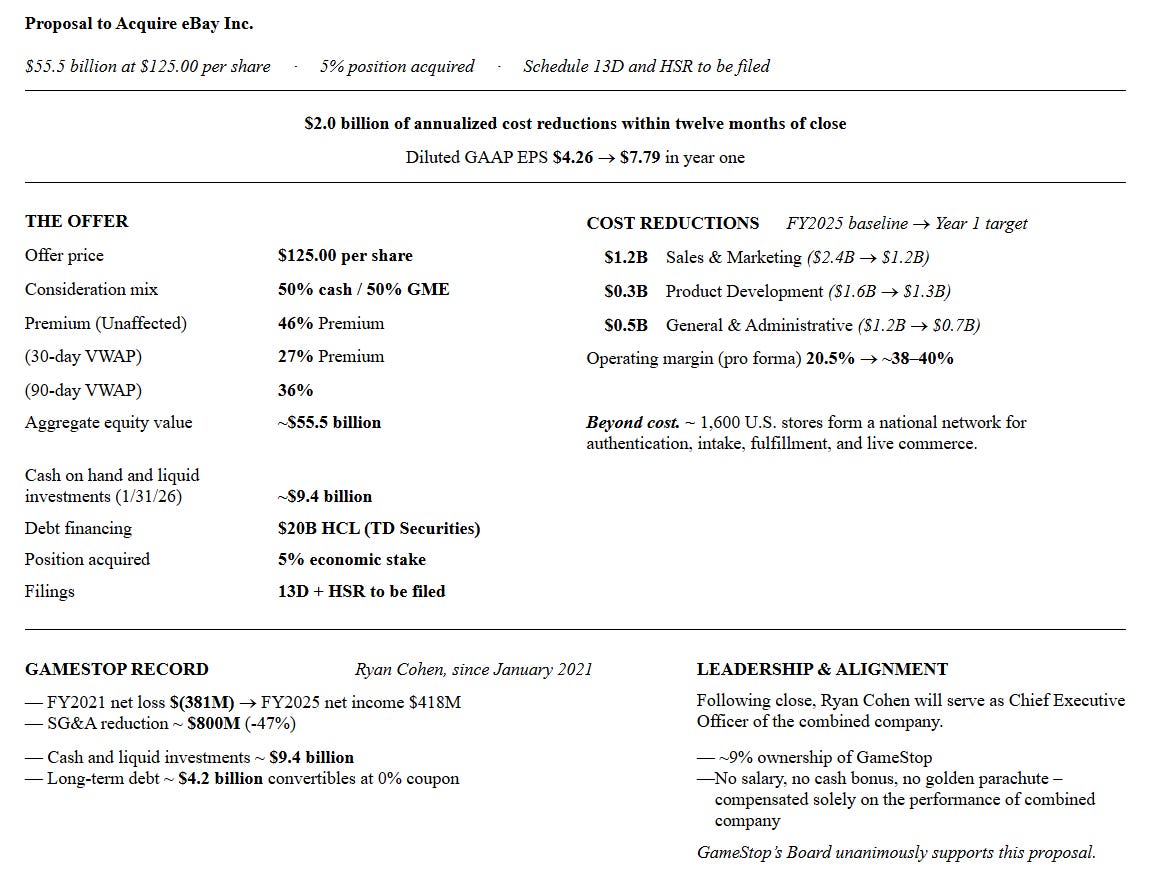

Start with what’s actually on the table. GameStop’s offer values eBay at $125.00 per share, structured as 50% cash and 50% GameStop common stock with full election rights and pro-rata allocation. At eBay’s share count, that works out to a ~$55.5 billion equity purchase price. It’s literally laid out in his 1-page memo:

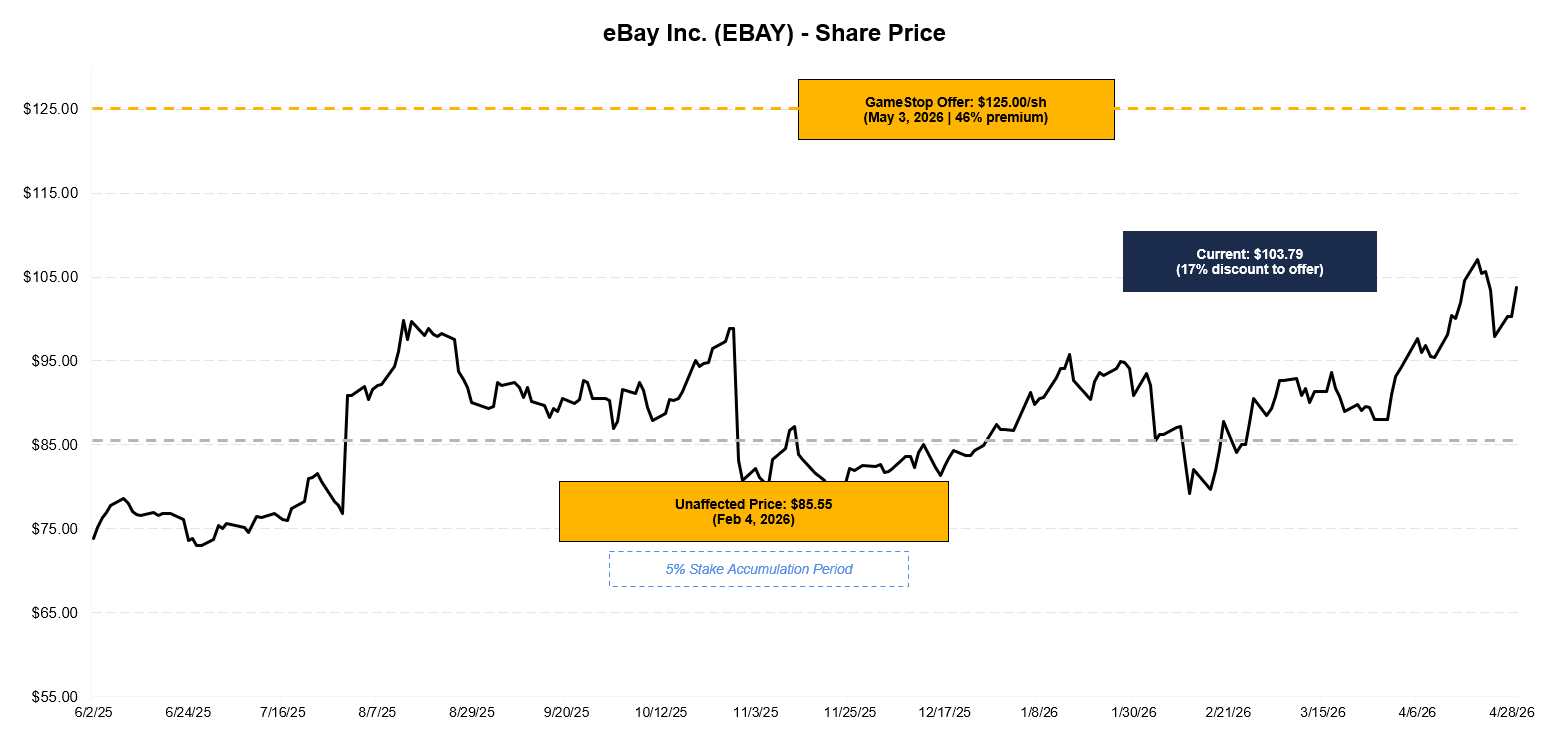

The offer represents a 27% premium to the 30-day VWAP and a 46% premium to the unaffected closing price on February 4, 2026, the day GameStop began accumulating its position. That position now stands at ~5% of eBay’s economic ownership, built through a combination of common stock and derivatives.

The cash half of the consideration, around $27.8 billion, would be funded from $9.4 billion of GameStop cash and the $20 billion TD highly confident letter. A highly confident letter is not a commitment, which we’ll return to.

Ryan Cohen would serve as CEO of the combined company following close. His compensation structure carries no salary, no cash bonus, and no golden parachute. He owns ~9% of GameStop and would be compensated solely on the performance of the combined entity. GameStop’s board has unanimously supported the proposal. eBay’s board acknowledged receipt and is reviewing.

GameStop has signaled willingness to pursue a proxy contest if the board is unreceptive. That is the offer.

GameStop’s Capital Structure

GameStop’s balance sheet is the constraint here, not the strategic logic.

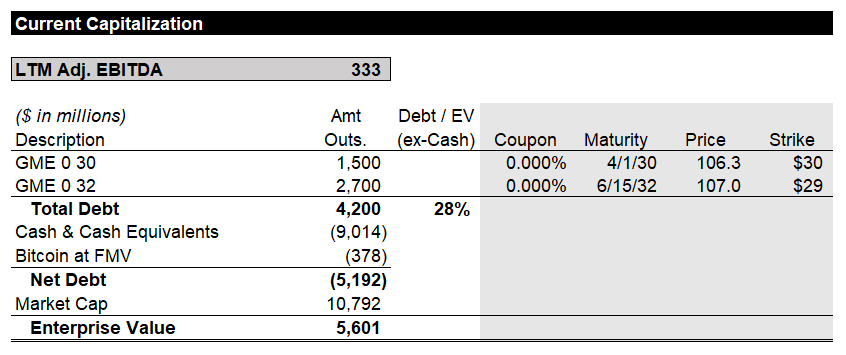

The company has ~$9.4 billion of cash and marketable securities as of January 31, 2026. That cash got there in fiscal 2025 through a combination of ATM equity raises and $4.2 billion of zero-coupon convertible notes across two tranches: $1.5 billion due 2030 with a $29.85 conversion price, and $2.25 billion due 2032 with a $28.91 conversion price.

GameStop trades around $24 today. Both tranches are out of the money, but volatility is high enough that both trade around 107. I wrote about the setup late last year.

The notes are senior unsecured. There are no covenants restricting additional debt. The notes include a Fundamental Change repurchase right, but the indenture’s public-stock exception means a GameStop-as-survivor structure doesn’t trigger it. The $4.2 billion stays in place.

What Will Actually Clear Credit Markets

GameStop is proposing to raise up to $20 billion of new acquisition debt against a pro forma cash flow base that depends on $2 billion of cost synergies. I’ll work through the synergies first, because they determine pro forma EBITDA, which determines leverage, which determines pricing, which determines whether the debt syndicates at all.

Synergies: What Credit Markets Will Actually Underwrite

Credit markets do not typically underwrite 100% of a sponsor’s synergy plan. They often underwrite a haircut version of it.

Cost takeouts that eliminate duplicative headcount and overhead get most of the credit, sometimes with a 12 to 18 month phase-in. Cost takeouts that reduce investment in the customer or the product get heavily discounted, because credit committees have seen too many deals where revenue follows the spending cuts down. Synergies framed as run-rate within 12 months almost always get pushed to 24 or 36 months in the underwriting case.

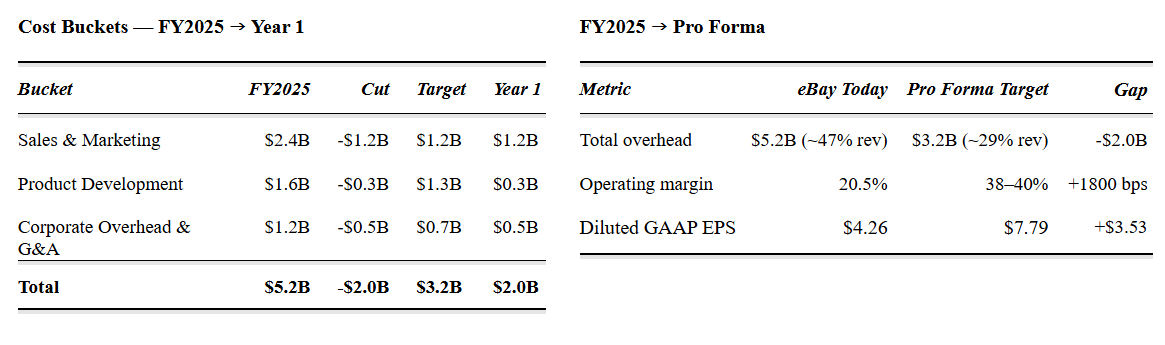

Apply that lens to the $2 billion GameStop is claiming.

G&A ($500M claimed) is the most defensible. Two public companies merging into one means duplicative finance, HR, legal, IT, real estate, and professional services. Eliminating one CFO, one general counsel, and consolidating audit and compliance is straightforward. Credit investors will probably underwrite $300-400M within 24 months; the full $500M is plausible by year three.

Product development ($300M claimed) is harder. eBay’s product development spend grew 11% in fiscal 2025 against revenue growth of 8%, which GameStop frames as overspending. The counterargument is that the AI-driven listing and search improvements driving the recent acceleration in GMV growth are exactly what that spending is buying. The new “Magical Listing” experience drove a 50% increase in new listing creation rates and double-digit increases in sold items per seller. Cutting $300M here means cutting into what is currently working. Credit underwrites maybe $100-150M, and only with a multi-year phase-in.

S&M ($1.2B claimed) is the most aggressive line. GameStop’s framing is that eBay spent $2.4B on S&M in fiscal 2025 and only added one million net active buyers. That ignores that eBay is in the middle of its strongest GMV growth in years, with US GMV up 27% year over year and focus categories up 24%. The marketing spend is correlated with the growth. Cutting it in half assumes the growth holds without it. Credit markets will not underwrite that. This amount is haircut by 2/3rds to $400M.

Under this logic, credit markets will give the deal credit for roughly half of the claimed synergies, phased over 18 to 36 months. Year-one synergies in the underwriting case are closer to $300-500M. I’m not saying this is necessarily what is achievable or will happen but this is what creditors, who are conservative by nature, will likely be willing to underwrite day 1.

That is enough to keep the financing conversation alive. But once the synergy case is haircut, the question now becomes how much leverage can this company actually carry?