Broadband Battles: WideOpenWest's Struggle For Relevance in a Cutthroat Market

A Tactical Review of a Highly-Levered, Equity Stub

Situation Overview:

WideOpenWest (“WOW”) is a top-10 US cable/internet provider operating in 15 states, primarily in the Southeast. The company is an “overbuilder” meaning it builds/operates in areas where there already is another cable provider. Nearly 3 years ago, I wrote about the company and the investment opportunity there—see below.

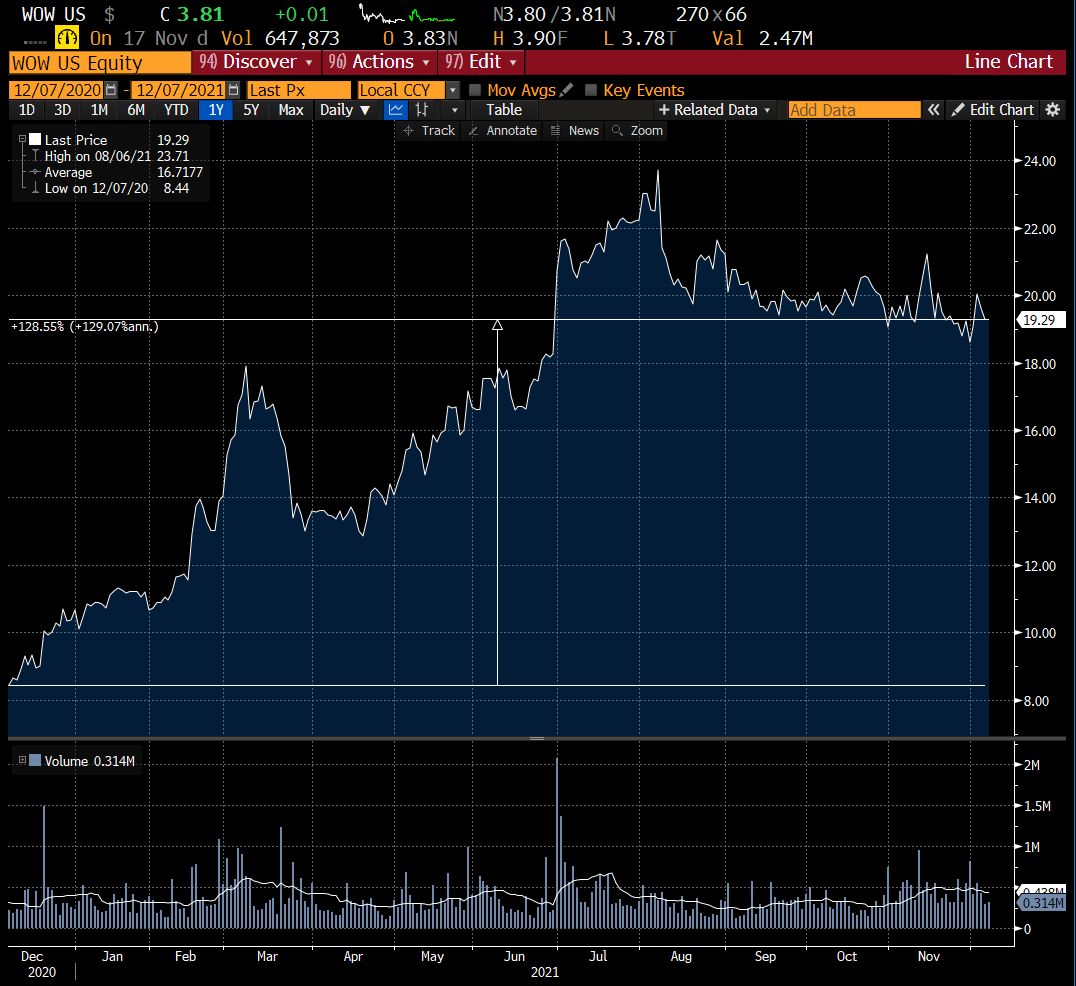

In June 2021, the company announced the sale of its Ohio assets to Atlantic Broadband for $1.125bn and its Chicago/Indiana/Maryland assets to Astound Broadband for $661mm, implying a collective purchase multiple of ~11x EBITDA— a notable 3-turn premium to WOW’s valuation at that time. The sale proceeds were used to de-lever the balance sheet, reducing leverage from 5.0x to 2.5x (at close), and to better position WOW for accretive edge-out/greenfield buildout strategies. The asset sales alongside improving sentiment in the sector helped drive the stock to a peak price of ~$24/share in August 2021, just shy of a 3-bagger from my initial write-up.

Since then, the entire US cable industry has seen a significant contraction in trading multiples on the backs of higher interest rates, elevated CapEx spend, and increased competition from fixed-wireless access (“FWA”) & fiber overbuilders. Industry multiples currently sit at their 10-year lows due to the confluence of these factors.

As a cable overbuilder with an even more competitive market environment, WOW has always traded at a discount to its cable incumbent peers such as Charter Communications. While WOW’s multiple has moved lock-step with the rest of the industry, in absolute terms, WOW currently trades at the lowest multiple in its history.

To date, the low multiple ascribed by the market has proven right. On November 8, 2023, WideOpenWest reported 3Q’23 results which not only missed street estimates on almost all accounts but also provided concerning forward-looking guidance.

Importantly, WOW reported accelerated subscriber losses in the company’s high-margin, high speed data (“HSD”) subscriber base. Management now believes HSD sub losses will be “significantly worse” in 4Q’23 with consensus estimates calling for the company to lose another 11,400 subscribers in the coming quarter (vs. 4,400 HSD subscriber losses in 3Q’23). The company also withdrew its financial guidance for the entire year (subscribers, revenues, and adj. EBITDA). In absolute terms, the subscriber loss may seem small; however, on a base of only 503,000 HSD subscribers, the order of magnitude is quite high. As this rate, it would be like Charter losing 852,000 subscribers in one quarter. Unsurprisingly, the market reaction was quite negative with the stock declining over 50% the next trading day.

Management attributed these poor results to several factors including widespread economic challenges, increased competition, and higher customer turnover in its lower-speed tiers following a price hike in July. Here’s the explanation from management in their own words:

The macro environment continues to be very challenging, which compounds the situation. Over the course of the year, we introduced rate increases, which led to higher-than-anticipated churn predominantly for those subscribers who subscribe to lower-tier speeds. During the third quarter, a large number of high-speed data customers also came off of promotions, which is resulting in higher expected churn, especially once again at the lower speed tiers.

Another factor contributing to the lower third quarter figure and reduced expectations for the fourth quarter has been with the pace of construction in our greenfield market. Although expansion is going well and we believe we are likely to hit 50,000 new homes passed by the end of this year, the pace of construction in these new markets is below our internal forecast, which is significantly reducing the number of gross connects we expected.

And lastly, we are seeing fixed wireless begin to more aggressively compete for our customers at the lower speed tiers across several of our legacy markets. However, we are absolutely confident in our good value, high quality and reliable service, especially as significantly more of our customers are buying 500 meg and above. We also believe that many of these customers who left will return to WOW! due to the reliability and value of our high-speed data service.

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.