An Update to National Cinemedia's Bankruptcy Case

Three important updates since filing Chapter 11

Since my original post on (see below), several events have occurred, and I believe it would be valuable to update my valuation analysis.

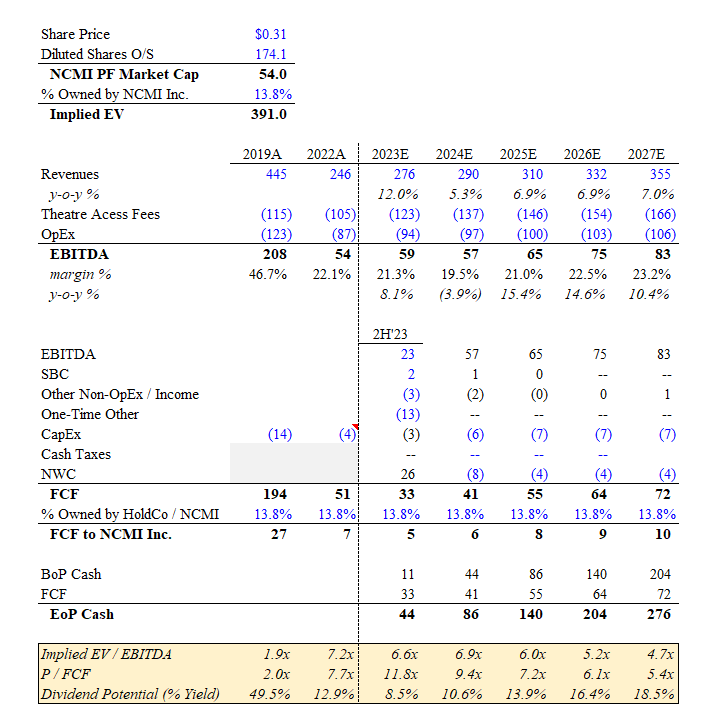

Firstly, we have an updated share count of 174 million, as per the latest 10-Q filing on May 9th. See below for details.

Secondly, NCMI has been negotiating with Regal/Cineworld over its ESA, and it appears that they have reached an agreement. The company provided cleansing materials on May 9th, reflecting the revised economics, which will be effective July 1, 2023. As you can see, theatre access fees are approximately $5 million higher than the previous financial projections.

Third, the company released an amended disclosure statement which shows a valuation analysis conducted by investment banking firm Lazard. Assuming an effective date of August 17, 2023, Lazard estimates the value of the reorg equity to be between $396 million and $521 million with a midpoint value of $461 million.

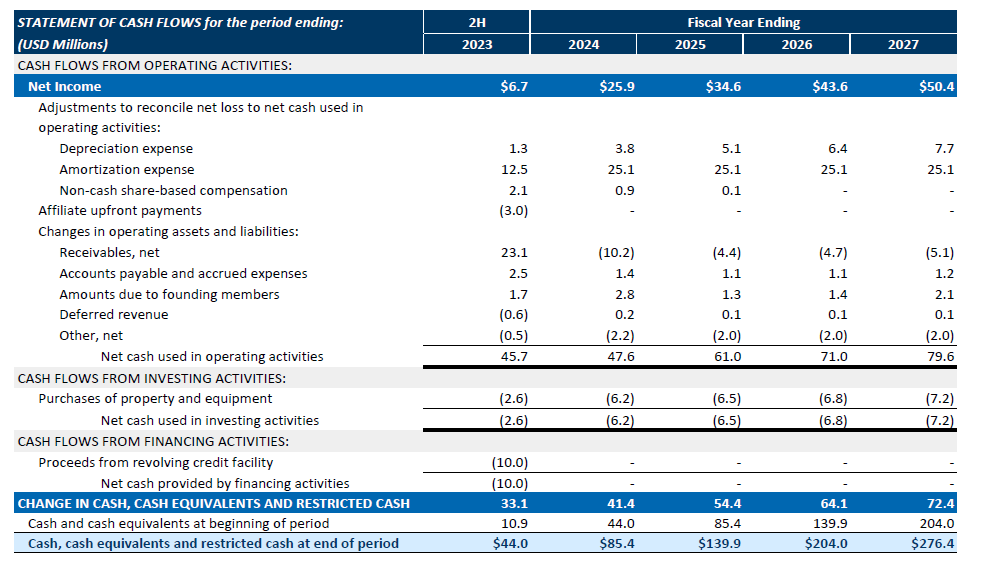

The disclosure statement also provided cash flow statement projections.

Putting all of this together, we can see that the equity is more interesting than I had previously anticipated. Not only are you creating the business at a ~15% discount to the midpoint of Lazard’s valuation analysis, but it is also lower than the low end of their range. Additionally, over the next 5 years, management expects to generate $265 million of FCF, which alone accounts for 68% of today’s implied EV. By 2025, NCMI could be generating enough cash flow to provide a 14% dividend yield. See below.

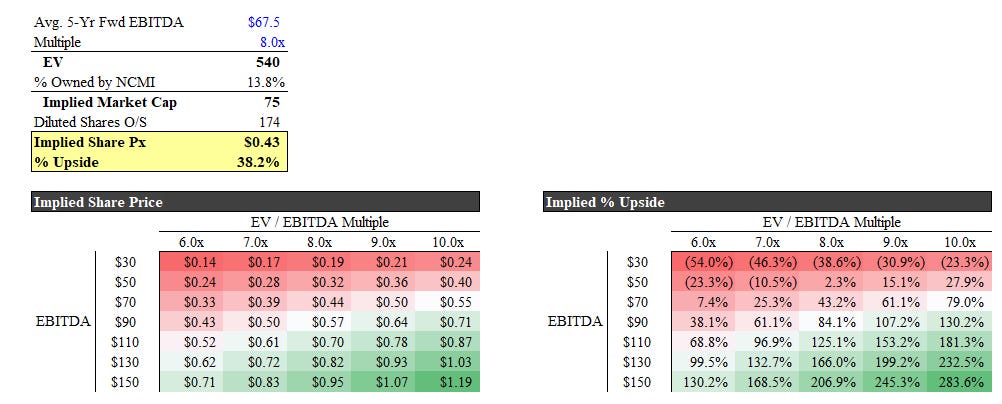

Below are the updated sensitivities, which sensitize EBITDA and EV/EBITDA multiples. It is not too difficult to envision a much higher share price than today. I will note that you can create the business at a slightly cheaper valuation (~7% discount) by buying the secured bonds instead of NCMI equity. However, most of us are not QIBs and are unable to buy 144A bonds.

Lastly, the Unsecured Creditors Committee ("UCC") has been officially formed and is putting up a fight in bankruptcy court. As it currently stands, their projected recovery is a mere 0.03%. I do not have a strong view on the legal merits of their claims, but seeing the unsecured bonds trade at 2 cents on the dollar ($5 million market value), it seems unlikely that they will recover much, if anything. I could, however, see them improving their recoveries slightly through nuisance (i.e., settlement to avoid further legal action). Either way, I do not believe that the UCC's potential recoveries will meaningfully change the economics that will accrue to NCMI equity.

Seems there was also a hearing on the 10th. That might be interesting to listen to and see if they just plan to be a nuisance and get a settlement or go full court press.

I believe the share count to use for valuation purposes is ~195.5 million. This is due to the units issued to AMC and Cinemark in early April that they are likely to convert to NCMI shares in the very near future.