Victoria's Secret ($VSCO): A Bond Market "Show-Me" Story Yielding 9%

Assessing the Risk-Reward Trade-Off in VSCO's 2029 Notes

Situation Overview:

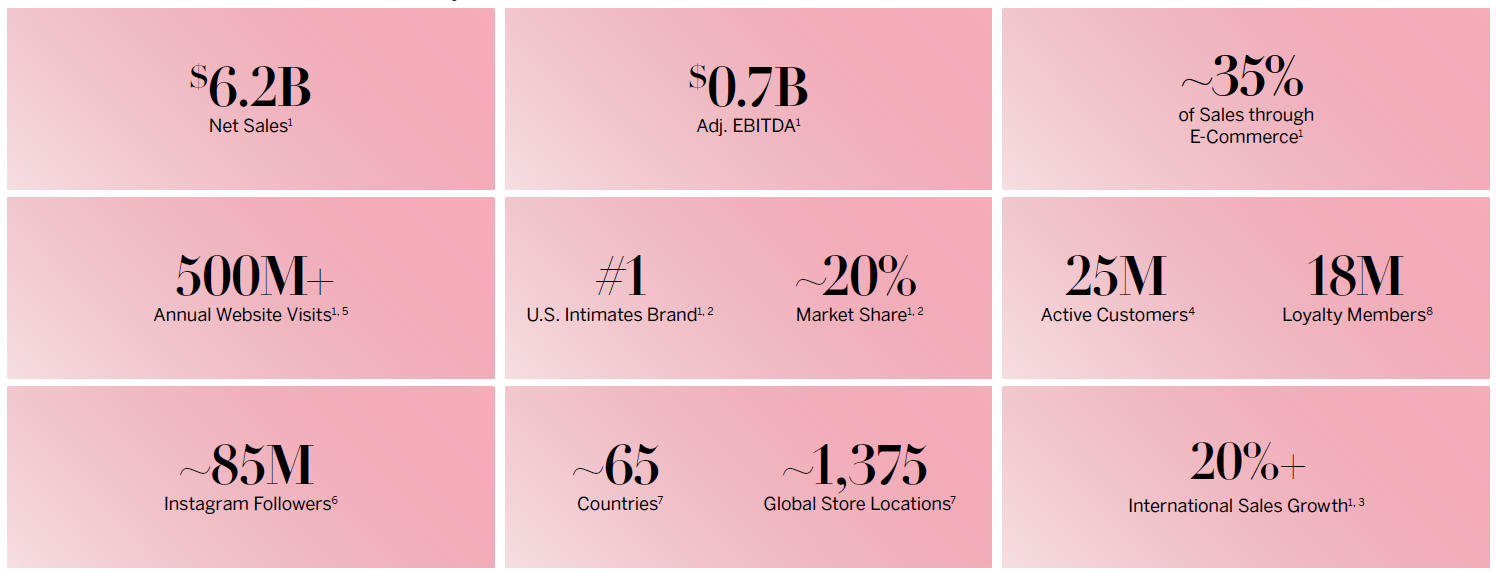

Headquartered in Ohio, Victoria’s Secret & Co (“VSCO”) is the #1 lingerie specialty retailer known for its iconic brand and broad product assortment across lingerie, beauty, and fragrances. The business operates nearly 1,400 stores globally and generated $6.2bn of sales in FY’23 (ended Jan 2024).

Following its separation from Bath & Body Works, VSCO has undertaken a major repositioning to shed its male-fantasy brand image and resonate with a broader demographic of women. Key initiatives include more inclusive marketing, modernized stores, expanded sizing, and a focus on core bra and basics. Management has also worked to optimize VSCO’s store footprint, digital capabilities, and supply chain to structurally improve profitability. However, the turnaround has been choppy with the stock down 70%+ from 2021 highs and bond spreads wider by 125bps+ as market skepticism has grown.

There are a few key factors at play:

Executional missteps and brand disconnect: Many of VSCO’s new merchandising and marketing moves have failed to gain traction. It’s shift away from “sexy” styles toward casual basics seems to have alienated its core customer without bringing in a new audience. Consumers appear confused by VSCO’s brand identity and as a result, the company has ceded share to more focused peers.

Macro pressures weighing on intimates demand. The overall intimates category in North America declined MSD% in FY’23 with pressures persisting into early FY’24. As a discretionary category, intimates spending is susceptible to pullbacks and trade-down in softer economic environments. VSCO has had to lean more into promos to drive demand.

Turnaround in a leadership transition. Just 2 years post-spin, VSCO has seen significant executive turnover with its most recent CEO (Amy Hauk) resigning just 8 months after taking the job. The lack of consistency at the top has led to stops/starts with turnaround initiatives and strained investor confidence.

Lackluster Financials

These headwinds have led to lackluster financial results for VSCO. On March 6, 2024, VSCO reported mixed 4Q’23 earnings, with sales up 3% y/y but below consensus. While topline inflected positively, this was largely due to an extra week in the quarter vs. the underlying trend which remained under pressure (4Q SSS comps -8%). Adj. gross margin expanded 240bps y/y on supply chain efficiencies but this was more than offset by 270bps of SG&A deleverage on negative comps.

More concerning was management’s subdued FY’24 guide, which came in well below consensus and implies another year of fundamental deterioration:

Sales guided to $6.0bn, -LSD% y/y on top of FY23’s -3% decline. This assumes ongoing North America intimates category pressure through at least 1H’24 and only modest 2H improvement.

Adj. Operating Income guided to $250-275mm, -10% to -19% y/y, reflecting gross margin recapture more than offset by SG&A deleverage. This implies -70bps to -110bps of margin contraction to 4.2-4.6%.

FCF guided to $175-200mm as lower EBITDA is only partially offset by $25mm reduction in CapEx to $230mm.

On the call, management attributed the soft guidance to macro pressures and “unevenness” in its turnaround rather than structural issues. However, the lack of visibility and inconsistent progress is clearly weighing on sentiment, as evidenced by the stock’s -25% negative reaction and senior notes’ ~5 point drop.

VSCO currently finds itself in a precarious position as its highly anticipated turnaround shows signs of stalling out. Despite initial optimism, the company’s latest earnings report paints a worrisome picture—with FY’23 sales -18% below 2019 levels, operating margins compressing 570bps vs. pre-COVID averages, and FY’24 guidance coming in well below expectations (LSD% sales decline and $250-275 million in EBIT vs. pre-earnings consensus of $351 million).

Management appears to be walking back prior investor day targets, core North America store sales are tracking over 30% below pre-pandemic levels, and the consumer landscape is shifting away from the company’s historical competitive advantages in structured bras and retail footprint. While the company’s bonds/stock screen cheap and there is theoretical recapture opportunity, visibility is extremely limited and management’s credibility has taken a hit. The market has moved decidedly into “show me” mode with VSCO, and rightfully so.

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.