The Most Interesting Trade in the $55 Billion $EA LBO

How a forgotten bond went from 65 to 87 overnight...and why the final price depends on contract language, not credit

🚨 Connect: Twitter | Threads | Instagram | Reddit | YouTube

Something new is coming.

Built for people who actually care about credit. If you want a first look before it opens up, join the early access list (limited spots).

Electronic Arts is being taken private for $55 billion.

The largest leveraged buyout since the financial crisis. $36 billion equity check. $20 billion debt from JPMorgan. Wall Street is running the usual analysis on deal size and leverage multiples.

The equity story is straightforward. Shareholders get $210 per share, a 25% premium. Done.

But EA’s debt has something odd going on. There’s $750 million of 2051 bonds with a change-of-control provision that lets bondholders put them back at 101. Standard protection for an LBO.

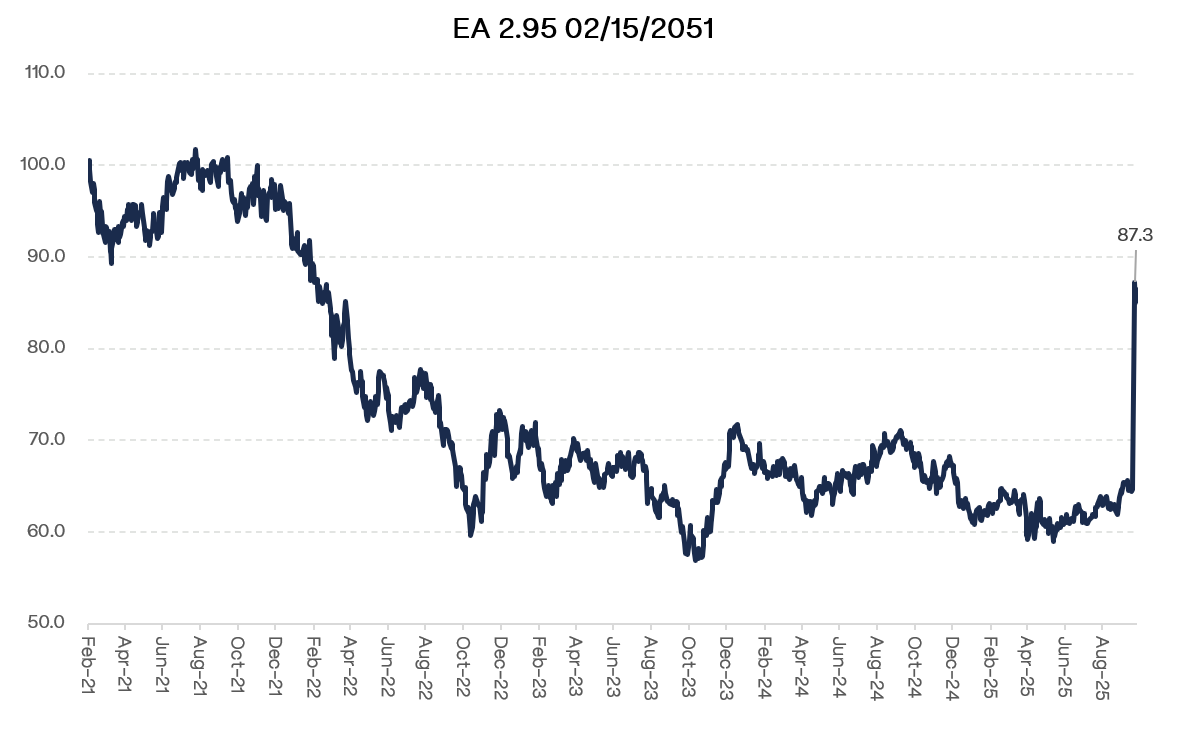

Yet the bonds are trading at 87. That’s a 14-point gap. Deal break risk alone doesn’t explain that kind of discount. Something else is going on.

The Forgotten Bond

EA’s 2.95% notes due 2051 weren’t supposed to matter. Pre-announcement, they traded in the mid-60s: orphaned, deeply discounted, the kind of long-dated paper that sleepy IG investors file away and forget about.

The discount had little to do with credit risk. EA was essentially unleveraged, generating $2.4 billion in EBITDA with barely any net debt. The bonds were cheap purely because of duration. Issued in February 2021 when rates were near zero, a 2.95% coupon now looks anemic compared to the 30-year yielding 4.7%. Too far out to matter for total return, too low-coupon to generate income, not distressed enough to be interesting.

The LBO announcement changed everything. Buried in the indenture is a change-of-control provision (triggered only if accompanied by a ratings downgrade to below IG) giving bondholders the right to put the notes back to the company at 101% of par. A bond trading at 65 suddenly has a contractual claim to 101. That’s a potential 55% return overnight.

Compare that to the equity. EA shareholders are getting $210 per share, a 25% premium to the pre-announcement price of roughly $170. Equity holders are celebrating a solid takeout. But bondholders who bought at 65 are looking at returns more than twice as large, with a fraction of the structural risk. The 2051s went from an afterthought to the best risk-adjusted trade in the capital structure.

At least, that’s how it looks on the surface.

*Updated for make-whole language correction (10/4/25)*Today’s Capital Structure

Before we get into the crux of the issue, let’s review the current capital structure.

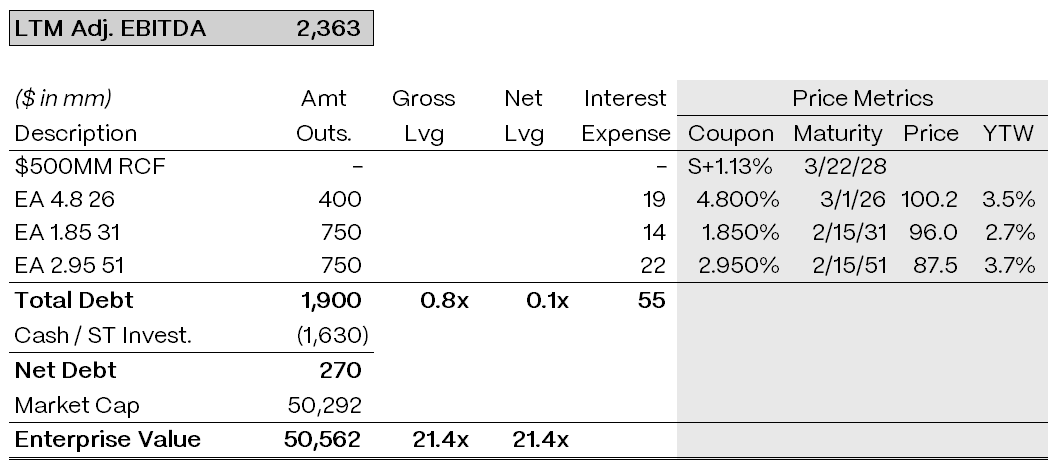

EA enters this transaction with one of the cleanest balance sheets in gaming. Total gross debt sits at $1.9 billion across three bond series:

Against this $1.9 billion debt load, EA holds $1.6 billion in cash and short-term investments. Net debt is just $270 million. With $2.4 billion in EBITDA, the company is running at roughly 0.1x net leverage, essentially unleveraged.

In the context of JPMorgan’s $20 billion financing package (levering the company up ten times to ~8x EBITDA), $1.9 billion of existing bonds is a rounding error. The real issue is the cost of that debt. The 2031s and 2051s were issued at incredibly cheap rates during the 2021 zero-rate era, carrying a blended 2.4% coupon across $1.5 billion of paper.

If the sponsors refinance this $1.5 billion at a hypothetical cost of 7%, the annual interest expense jumps from $36 million to $105 million. That’s a $69 million delta. Relative to $2.4 billion of EBITDA, you could argue this doesn’t matter much. But PV that $69 million annual cost over a five-year hold period and you’re looking at roughly $275 million. If you could avoid paying that, why wouldn’t you?

In a typical LBO, all existing public debt gets refinanced. Sponsors want a clean capital structure with no legacy covenants, no change-of-control provisions hanging over the deal, and no cross-default risks. JPMorgan’s $20 billion financing package will be sized to cover the equity purchase plus fees and expenses, and to take out all $1.9 billion of existing bonds.

The question is at what price.

The 101 Put: What Bondholders Think They Own

A change-of-control provision is bondholder insurance against exactly this type of transaction. When you buy a corporate bond, you’re making a bet on the credit quality of that specific company at that specific leverage level. If the company gets taken private in an LBO, everything changes. Management priorities shift from conservative balance sheet management to maximizing sponsor returns. Leverage spikes. Your bond goes from investment-grade paper backed by a cash-rich gaming giant to a junior claim in a highly levered capital structure.

The change-of-control covenant protects against this bait-and-switch. It gives bondholders the right to put their bonds back to the company at a premium (typically 101% of par) if control of the company changes hands. You get to exit on your terms rather than being forced to hold paper in a completely different credit.

These provisions are standard in credit docs but the language varies, and the conditions matter enormously. For EA’s 2051s, the change-of-control provision has two trigger requirements:

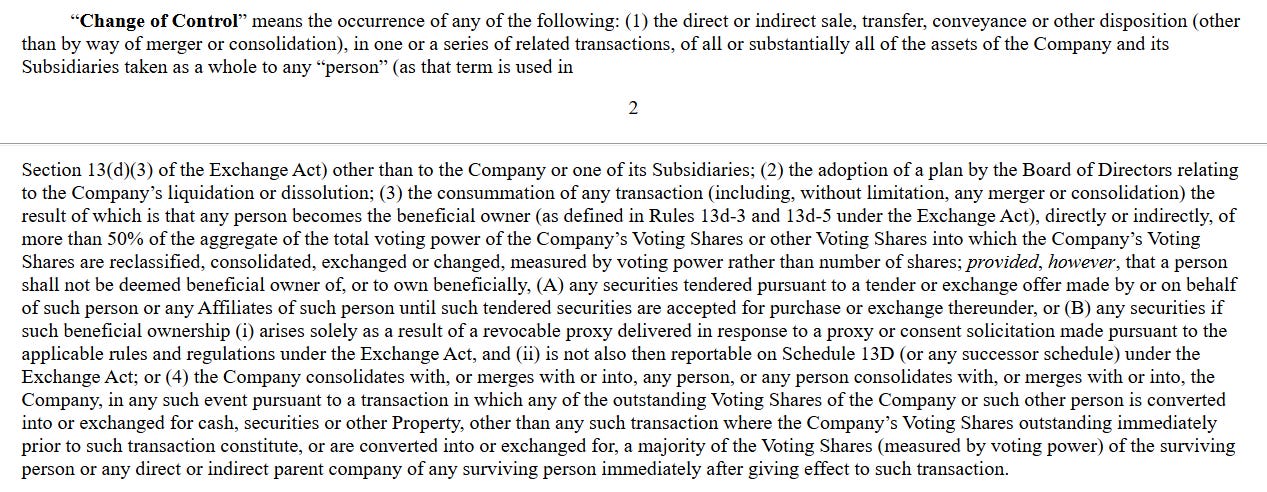

A change of control must occur. The indenture defines this as any person or group acquiring more than 50% of voting stock, or a sale of all or substantially all assets, or certain merger transactions. Silver Lake’s LBO clearly qualifies.

A ratings downgrade must occur. Within 60 days of the change of control, the bonds must be downgraded below investment grade (below BBB- by S&P or Baa3 by Moody’s) by both rating agencies.

Both conditions must be met. The LBO alone doesn’t trigger the put. The rating agencies also need to cut the bonds to junk.

Will they? Almost certainly. EA is moving from essentially zero net leverage to 7-8x gross leverage overnight. The rating agencies have been clear about their frameworks: high single-digit leverage in a cyclical industry like gaming doesn’t support an investment-grade rating. The downgrade to high-yield is a formality.

Once both conditions are satisfied, EA must make an offer to repurchase the bonds at 101% of par plus accrued interest within 30 days. Bondholders have 60 days to decide whether to tender.

Simple, right? Not quite. The same indenture that grants bondholders a put at 101 also contains provisions that could allow EA to avoid paying it entirely.

Disclaimer: I am not an attorney and this does not constitute legal advice. This analysis reflects my personal interpretation of the provided indenture documents, which may contain errors or omissions. It should not be used as a substitute for professional legal counsel. This is opinion and not investment advice; based solely on public information.

Base Indenture: Link

Supplemental Indenture: LinkThe Defeasance Debate

Defeasance is an obscure mechanism buried in most bond indentures that almost never gets used. Recent chatter among bondholders suggests EA might try to invoke it.

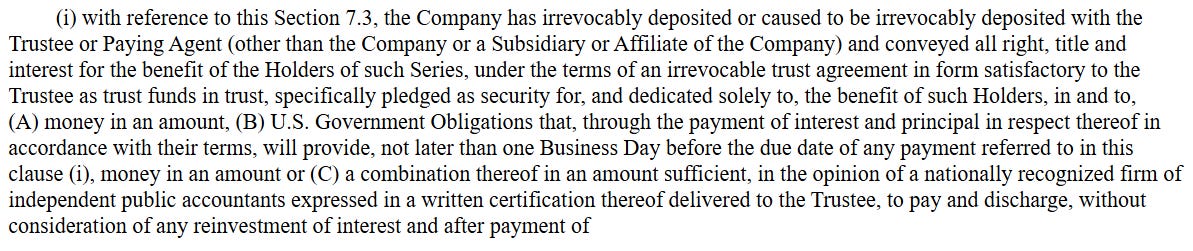

EA’s Base Indenture sets out the process in Section 7.3, “Defeasance and Discharge of Indenture.” In simple terms, EA would need to irrevocably deposit with the trustee enough U.S. Treasuries or cash to cover every future coupon and the final principal repayment on the 2051s. That deposit becomes a dedicated trust for the benefit of bondholders.

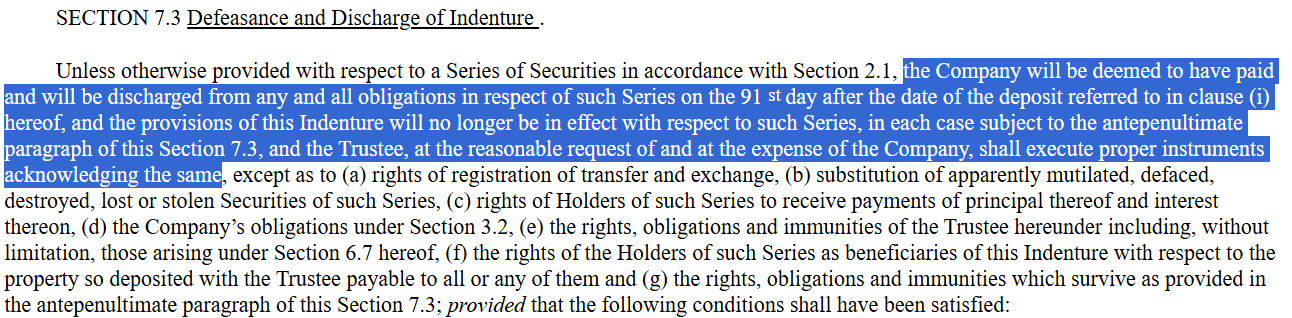

Once the deposit is made, EA must also deliver tax and legal opinions, confirm that no default exists, and wait out a 91-day period. At the end of that process, the indenture states the company “will be deemed to have paid and will be discharged from any and all obligations in respect of such Series” other than a short list of administrative items.

The Change of Control repurchase covenant in the Supplemental Indenture (Section 4.02) is not on that survivor list. That means if EA were to complete defeasance under Section 7.3, it would likely no longer be required to make a 101% repurchase offer if a Change of Control Repurchase Event occurs.

At today’s long Treasury rates of about 4.7%, funding a 2.95% coupon bond requires depositing significantly less than par. The present value math works out to roughly 74 cents on the dollar. A defeased bond would likely trade like an escrowed-to-maturity Treasury proxy, not a security with a 101% exit right.

The mechanics still matter. EA would need to make the deposit in full, provide verification that the escrow is sufficient, and deliver the required tax and legal opinions. Timing is also critical: defeasance must be completed before the Change of Control put right becomes live.

If executed properly, bondholders would end up with a long-dated Treasury proxy paying 2.95% until 2051, worth in the mid-70s at today’s rates. The upside to 101% would no longer be available.

Whether bondholders would accept that outcome without challenge is another matter. Here’s why.