The Farfetch Enigma: From Digital Dominance to Distressed Debt Dilemma

A Deep Dive into Farfetch's Distressed Convertible Bonds: Challenges, Prospects, and Implications for Investors

Situation Overview:

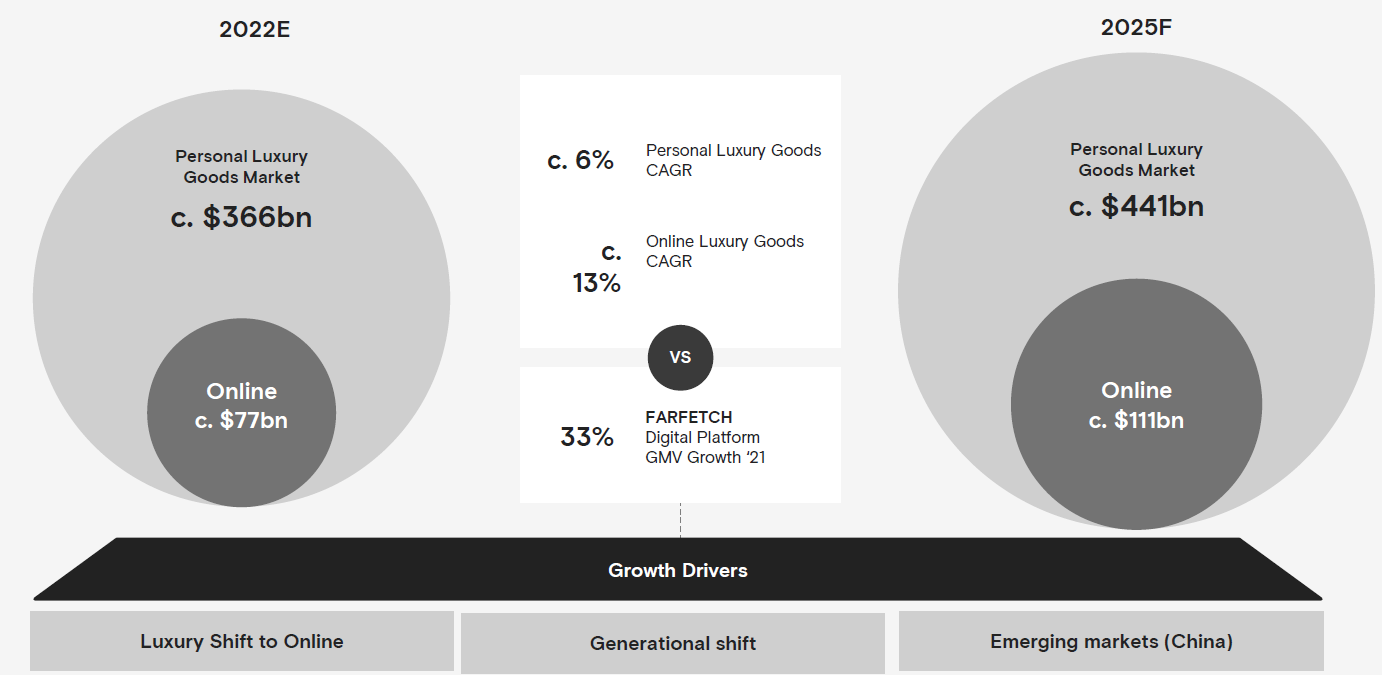

Founded in 2007, Farfetch Limited (“Farfetch” or “FTCH”) is a digital marketplace for luxury goods serving consumers in 190+ countries. Through Farfetch’s digital platform, shoppers have access to 3,500+ brands sourced from 1,400+ luxury vendors. As an e-commerce platform, Farfetch capitalized on the shift to online shopping during the COVID pandemic, evidenced by its impressive revenue CAGR of 49% between 2019 and 2021. From an industry standpoint, the $77 billion online luxury market lags behind other retail sectors with e-commerce making up just 20% of sales. As a market leader, Farfetch was well positioned to benefit from the growing shift of luxury good sales to online.

The prospect of a huge underpenetrated TAM captured investor’s imagination and sadly, also fueled their greed. After hitting lows in March 2020, Farfetch’s stock price saw a tenfold increase over the subsequent twelve months, pushing its market capitalization to a whopping $28 billion in February 2021

The company used this success to rapidly expand into additional verticals and bolster its partnerships. Between 2020 and 2023, Farfetch made 4 acquisitions: LUXCLUSIF, Palm Angels, Violet Grey, and Wannaby. These acquisitions were part of Farfetch’s strategy to expand its offerings and reach new customers, such as the luxury resale market, the luxury streetwear market, the luxury beauty market, and social commerce.

In April 2022, the company made a notable $200mm equity investment in Neiman Marcus Group (“NMG”), a recently-restructured luxury department store operator. In return, NMG would utilize Farfetch Platform Solutions (FPS) to re-platform its Bergdorf Goodman website and mobile application.

In August 2022, Farfetch and Richemont, a luxury-goods group, announced a deal in which Farfetch would acquire a 47.5% stake in YOOX Net-A-Porter (“YNAP”), Richemont’s online fashion retailer, for over $2.7 billion. Farfetch agreed to also re-platform most of Richemont’s Maisons under FPS. In return, Farfetch would gain access to YNAP’s large customer base and extensive selection of luxury brands, while Richemont would benefit from Farfetch’s technology and expertise in e-commerce, as well as its global reach. The deal remains pending regulatory approval and is subject to specific deal conditions.

The company’s newly-founded success was short-lived as Farfetch began to face several headwinds beginning in 2022 including unforeseen geopolitics, macroeconomic pressures affecting luxury spending, and operational complexities from rapid expansion. In 2022, Farfetch halted operations in Russia following the Ukraine conflict. This market had previously seen rapid growth and became the company’s third-largest, contributing 6% to the GMV in 2021. Additionally, rolling lockdowns in China and supply-chain challenges continued to negatively impact performance. On top of this, inflation began to impact Farfetch’s operating costs which rose due to increased labor expenses and brand marketing investments.

Operationally, the company was also facing several challenges. For starters, Farfetch saw intense competition from brands developing their own direct-to-consumer platforms with a diminishing price advantage over direct brand websites. Furthemore, newer business ventures like New Guards Group (“NGG”) did not meet expectations and the company’s recent partnership with Reebok received tepid response.

In its most recent quarter, Farfetch not only missed estimates but also revised its full-year outlook substantially lower. This compounded the prevailing negative sentiment causing the stock to plunge 43% the following day. The company now expects GMV for FY 2023 to be $4.4 billion (+3% y-o-y), a substantial decrease from the $4.9 billion projected earlier in the year.

Despite market skepticism, management continues to guide to positive EBITDA and FCF for 2023. Management also reiterated its 2025 forecast although realizing these goals seems increasingly challenging. As a much-needed cost-cutting action, the company reduced 800 positions in June/July of this year which is expected to reduce expenses by $150mm.

While the company is taking steps to address these challenges, it is too early to say whether they will be successful. In February 2023, the CFO stepped down after more than eight years in the role causing further investor angst. Market sentiment remains extremely bearish with the stock sitting at just under $2/share, representing an impressive 98% decline from its peak.

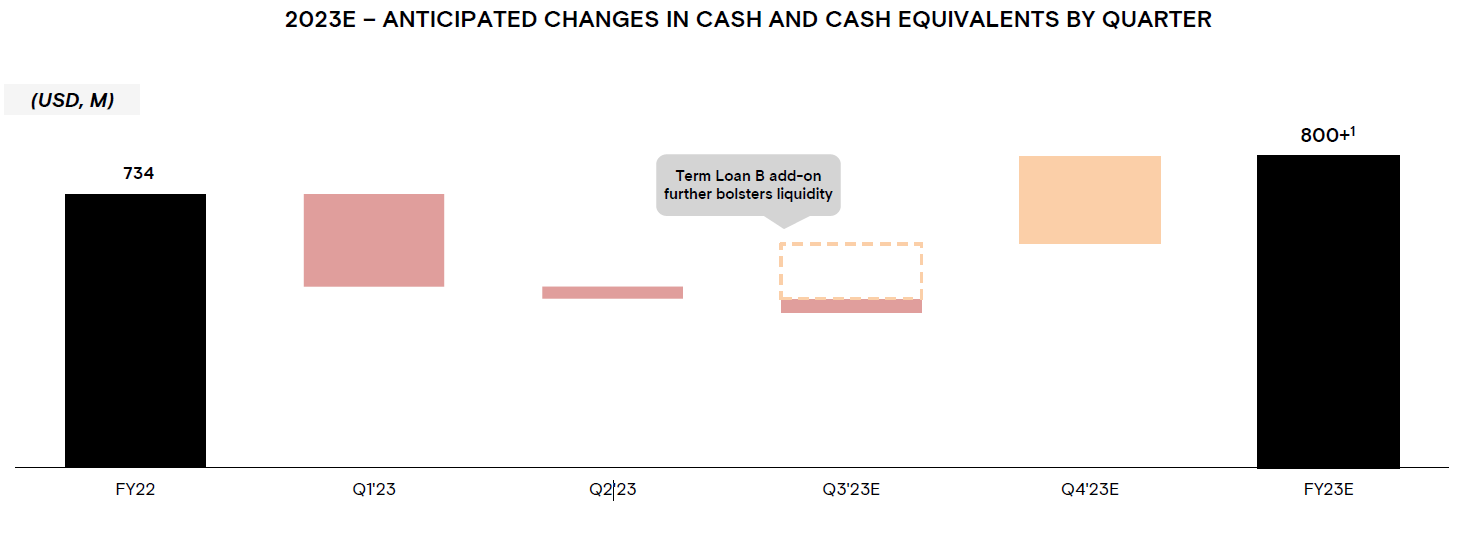

With rising rates, recent investor attention has been focused on the company’s rate of FCF burn. Despite the rapid growth in topline, the company has not had a year in which they generated positive FCF. In fact, FCF burn has appeared to get progressively worse, questioning the viability of the entire business model. In the last twelve months, the company burned over $600mm of cash. This paints a bleak picture relative to its 6/30 cash balance of ~$450mm. To bolster liquidity, Farfetch completed a $200mm TL-B add-on in August 2023. As a reminder, the company issued a $400 million 5-yr cov-lite TL-B in September 2022 at a price of SOFR+625 at 93.5.

The company also expects to receive cash from a $200mm VAT-related receivable, which it plans to reduce by half by year’s end. They’ve successfully collected amounts from several countries, but larger balances in Italy and France are still under review. Farfetch also has $435mm of inventory, which management expects to decline to $300mm by year end. Management believes that the combination of these will allow it to end the year with $800mm+ of liquidity.

Beneath the company’s ~$600mm of secured debt sits a $400mm unsecured convertible bond. The convertible bond matures in 2027 and is currently completely out of the money (~$16/share conversion price). Farfetch has historically tapped the convertible bond market to fund FCF burn but given the decline in its stock price as well as higher interest rates, the convert market remains largely inaccessible. Given the priming nature of the new debt issuance, coupled with limited business visibility into sustainable profits or FCF generation, Farfetch’s convertible bonds have similarly plunged in price. Currently, these bonds are trading at an all-time low of 51 cents on the dollar, implying a yield to maturity of ~23%. This is a stark contrast vs. the 450 price (yes that’s 450 cents on the dollar) they commanded just 36 months prior.

While Farfetch today occupies a prominent position in the luxury digital marketplace, its near-term outlook is overshadowed by operational and market difficulties. This uncertainty is compounded by a track record of missed forecasts and unmet expectations. Despite these overhangs, the company maintains a commitment to profitability and reaching its long-term goals.

In the following section, I review the company’s financials and capital structure and provide some key considerations as it relates to Farfetch’s convertible bonds due 2027. At today’s price of 51, FTCH’s convertible bonds have a yield to maturity of 25%. Whether they survive until 2027 is another story.

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.