Organon ($OGN): Dividend Axed. Narrative Dead. Credit Holds the Bag.

The dividend’s gone, VTAMA’s unproven, and Nexplanon is racing the patent clock. That’s the whole story.

❗Connect with me on Twitter / Instagram / Threads / Bluesky / Reddit (*new*)

🚨 Something new is coming. Join the early access list — limited spots.

They cut the dividend by over 90%. And no one clapped.

That’s where Organon is right now. Not dead. But hurting. The stock is down 60% since September. The market panicked. Investors fled.

Management says this cut was “from a position of strength.”

That’s like saying you’re getting a divorce to save the marriage.

Here’s what’s really going on:

Organon has too much debt. Net leverage is ~4.5x. Cutting the dividend frees up $265 million by year-end to get that under 4x. That’s the goal. De-lever first. Figure out growth later.

But growth is the real problem.

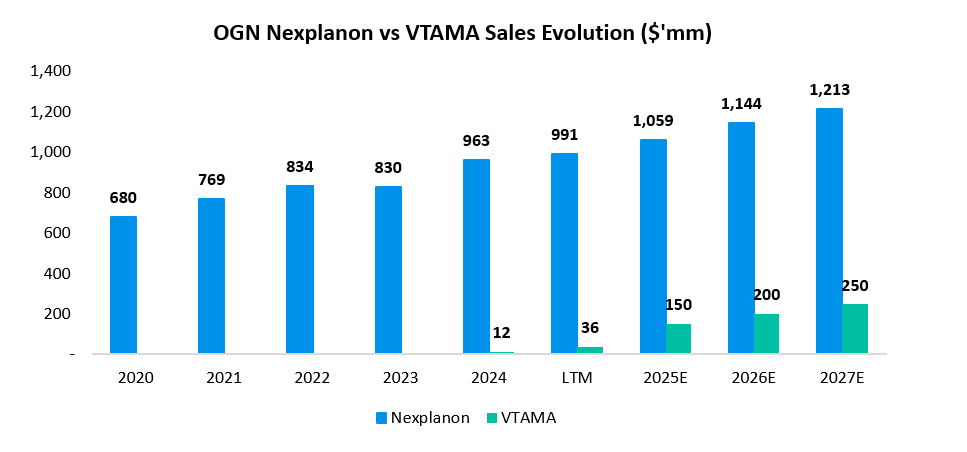

Nexplanon is their best asset. It’s expected to hit $1 billion in sales this year. But the patent expires in 2030. The clock is ticking.

Meanwhile, VTAMA was supposed to be the next growth engine. But sales are slow. Coupon use is high. The $150 million 2025 target looks aggressive.

Everything else?

Established brands are declining.

Biosimilars are getting squeezed.

R&D is being cut to meet FCF.

This isn’t a strategic pivot. It’s survival mode.

Business development? On hold.

Catalysts? Mostly cost-cutting.

This used to be a yield story.

Now it’s just a story about buying time.

The question is: what do they do with it?

I. Situation Overview:

Organon wasn’t supposed to be exciting. That was the appeal.

When Merck spun it off in 2021, the pitch was clear: a low-drama cash machine built on mature drugs, dependable revenue, and a fat dividend. A pharma company for income investors. Safe. Predictable. Boring, in a good way.

And for a while, it was.

Organon sells prescription drugs in three main buckets:

Women’s health, led by Nexplanon, a long-acting birth control implant

Biosimilars, like Hadlima (a Humira copycat)

A large base of off-patent legacy drugs (think cholesterol meds, hormone therapy, allergy pills)

The business model is simple: squeeze steady cash flow out of aging products, pay a big dividend, and maybe tack on a few tuck-in deals for growth. The company paid $1.12 per share in annual dividends, yielding more than 7% at spin.

Nexplanon carried the story. Sales hit $963 million in 2024 and are on pace to exceed $1 billion in 2025. But the applicator patent expires in 2030. Once that falls, so does the moat. Nexplanon accounts for 15% of total revenue, and the clock is ticking.

The rest of the portfolio? Not doing much heavy lifting.

Established brands declined 11% y/y in 1Q’25

Biosimilars fell 17%, hit by price compression and maturing markets

In 2024, Organon tried to change the story. It acquired VTAMA, a topical treatment for psoriasis and atopic dermatitis. It was their first real move toward growth. But VTAMA’s launch has been slow. Sales were just $24 million in 1Q, and while the company still guides to $150 million for 2025, that target is looking shaky.