KORE Group Holdings, Inc. ($KORE): When Leverage Meets IoT Disruption

A Multi-Layered Debt Stack Threatens This Connected Device Leader's Future

🚀 We’re expanding! Interested in full-time or internship opportunities (Summer 2025)? Get in touch!

A few weeks ago, I asked on Twitter for interesting situations to dig into over the holidays. KORE caught my eye—a PE-backed roll-up turned public company via SPAC (classic) with a familiar cast of characters in the cap stack. Whitehorse holds the term loan, Fortress owns the notes, and Searchlight sits in the preferred equity, while Abry Partners and Koch stayed on as the largest shareholders post-SPAC.

The business itself operates in an attractive space—helping companies manage their connected devices across cellular networks. But KORE’s got problems. Years of PE-backed acquisitions left them with integration headaches and a heavy debt load just as new technology threatens their business model. Management’s trying to right the ship, but with meaningful interest payments and preferred dividends accruing at 13%, they’re running out of time to execute. Let’s dig into what’s really going on here.

I. Situation Overview

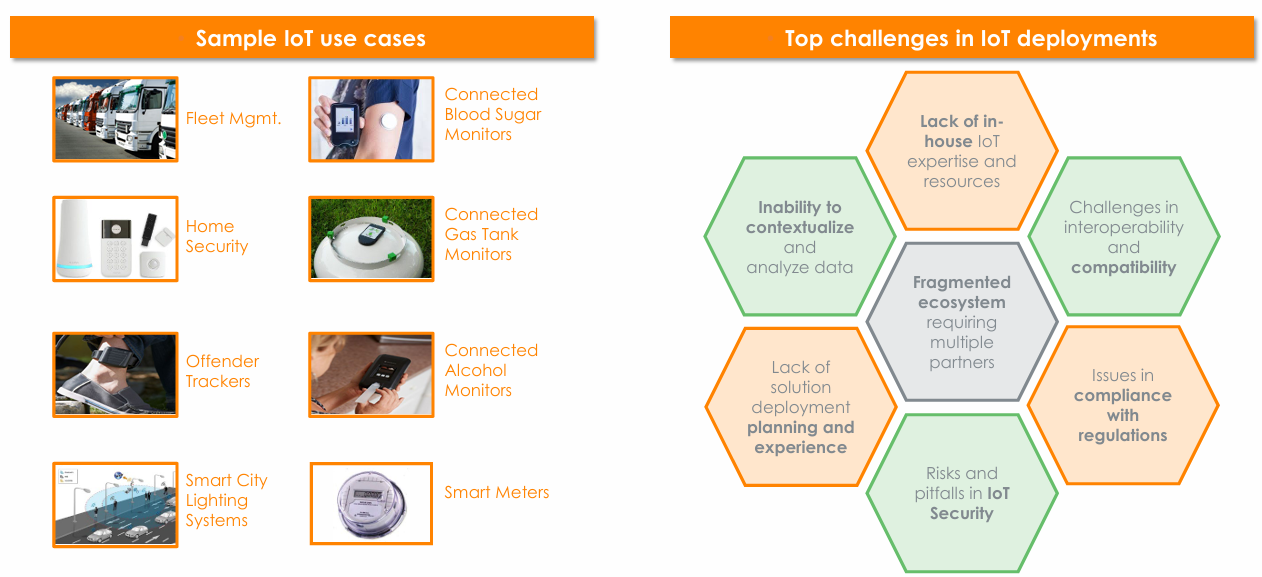

Founded in 2002, KORE Group Holdings (“KORE”), sits at the intersection of IoT and connectivity. Their pitch is straightforward: when companies need to keep thousands of connected devices online—from heart monitors to delivery truck trackers—KORE provides the cellular connectivity through a single platform, rather than forcing customers to juggle relationships with multiple wireless carriers (e.g., Verizon, AT&T).

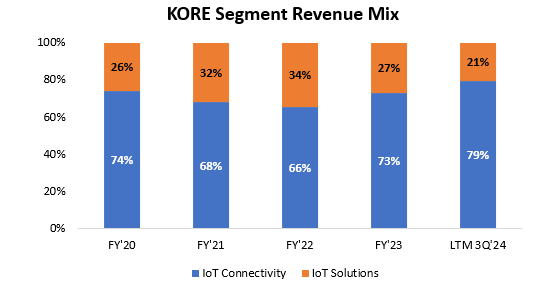

It’s a model that’s found its market. Today, KORE manages 18.8 million connected devices for 3,600 customers across healthcare, asset tracking, and fleet management. The business breaks down into two segments: Connectivity (79% of revenue), providing cellular access across carrier networks, and IoT Solutions (21%), handling device management and analytics.

Private Equity Transformation

The trajectory changed in 2014 when Abry Partners acquired control for $116 million. What followed was strategic expansion: RACO Wireless (2014), Wyless Group (2016), and ASPIDER-NGI (2018). These acquisitions broadened KORE’s capabilities but significantly increased the debt burden.

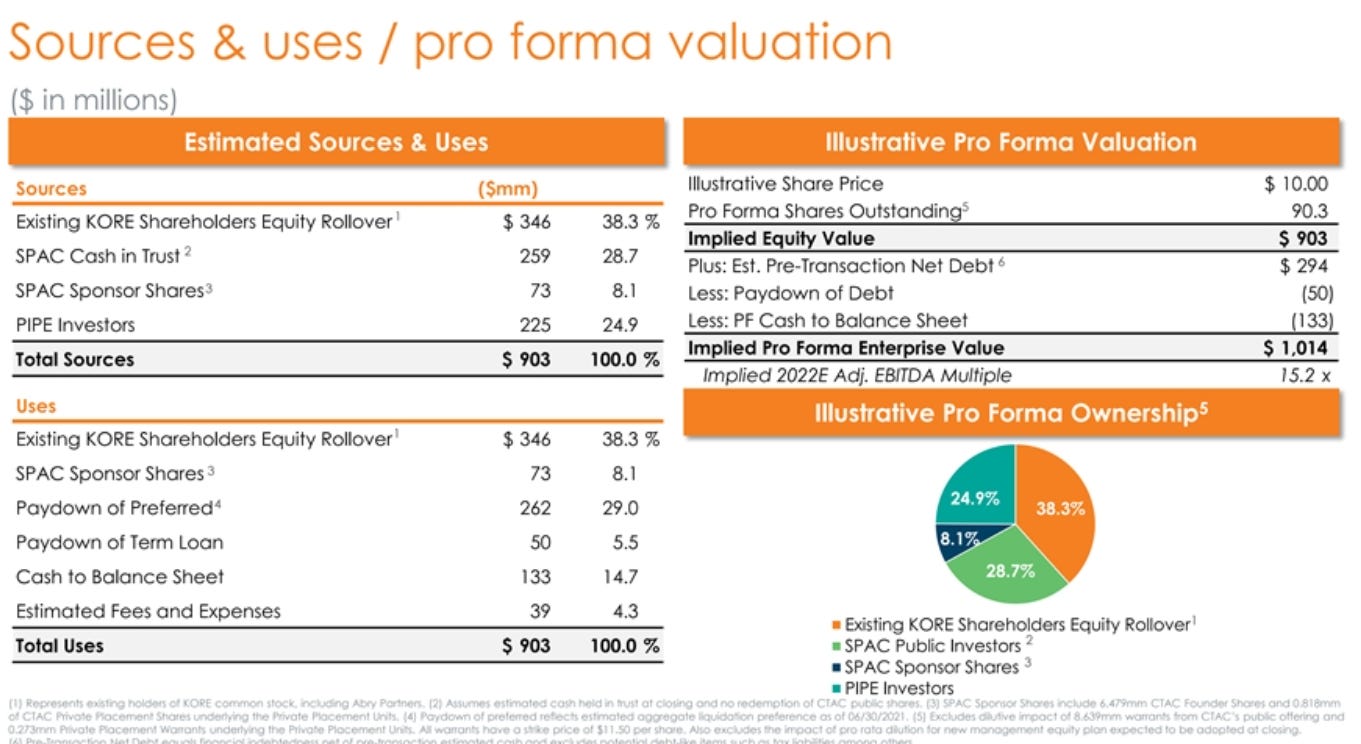

This expansion culminated in October 2021 with a SPAC merger through Cerberus Telecom Acquisition Corp, valuing KORE at $1 billion (15.2x FY’22E EBITDA). Koch Industries and BlackRock-managed funds led a $225 million PIPE investment, while Abry maintained a 38% stake.

Integration Challenges

The integration of these acquisitions has proven more challenging than anticipated. KORE continues to face fundamental platform issues—the fragmented system architecture means moving customers between platforms requires treating them as entirely new customers. While the recent Twilio IoT brought valuable technological capabilities that could prove crucial for future growth, it also added another layer of complexity that has historically burdened the company.