Jeld-Wen ($JELD): Cost Cuts vs. the Clock

Why the 2027s matter more than the second-half savings

🚨 Connect with me on Twitter / Threads / Instagram / Bluesky / Reddit (*new*)

You know when a company says “transformation,” but what they really mean is “please don’t look too closely”?

That’s Jeld-Wen.

They’re shutting plants, installing robots, cutting heads… all in the name of a $150 million “turnaround plan” that’s supposed to fix everything by the back half of 2025.

For years, Jeld-Wen was boring. Doors, windows, zero drama. Then the growth dried up, the private equity playbook ran out, and now it’s a race between operational “savings” and capital structure fatigue. And the unsecureds are already voting with their feet.

Q1 EBITDA margins cratered to 2.8 percent. Cash flow? Still negative. The 2032s are drifting. The 2027s aren’t far behind. And management keeps recycling the same lines: it’s the macro, it’s temporary, just wait.

Sure. Because “wait and see” worked so well in 2023. And 2024.

This isn’t a misunderstood cyclical. It’s a company with a mid-century cost base trying to survive in a 21st century margin environment. And they’re patching it up with consultants, PowerPoints, and wishful thinking.

Jeld-Wen used to be a sleepy industrial. Now it’s running out of cash flow, out of credibility, and out of quarters to deliver.

Management calls it a “transformation.”

But if you’ve seen this movie before, you know exactly how it ends. And who’s left holding the bag when the lights come on.

I. Situation Overview

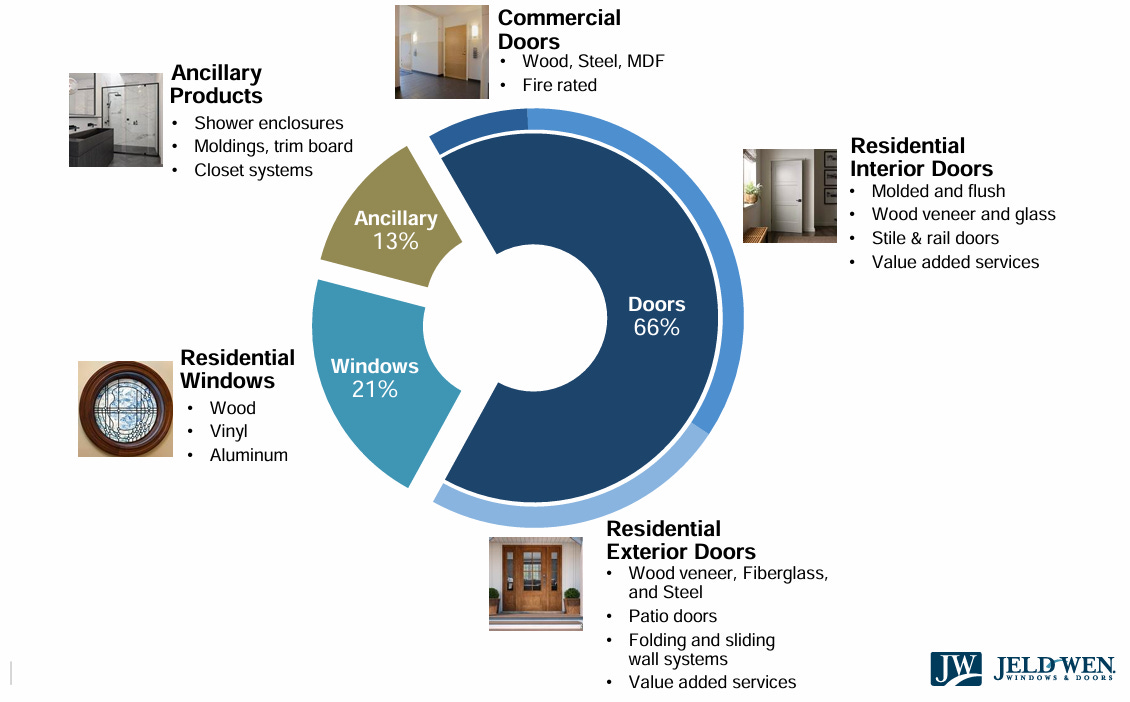

Jeld-Wen (“JELD”) makes doors and windows for a housing market that isn’t moving. The company builds everything from molded interior slabs to vinyl windows and sells into new construction and R&R channels through a mix of retailers, distributors, and pro dealers.

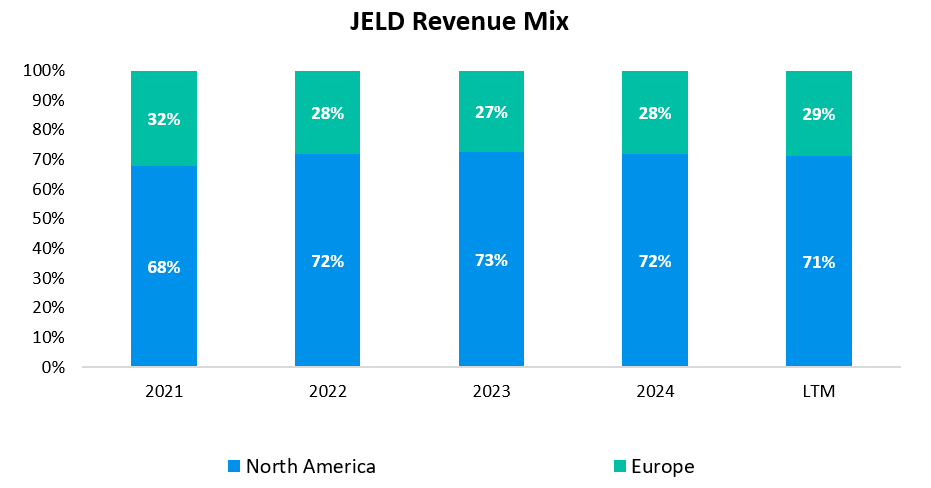

About 70% of revenue comes from North America. The rest comes from Europe. It’s a capital-heavy business with modest margins, where fixed costs only make sense when volumes are flowing. Right now, they aren’t.

This was a classic private equity play. Onex bought JELD in 2011, levered it up, and IPO’d it in 2017. Since then, it’s been four CEOs, two failed turnaround plans, and a long list of excuses. The company never integrated its footprint. Capex was consistently short. The pandemic boom gave management cover, but instead of reinvesting in plants or systems, they took price and lost share. Now the housing cycle has rolled, and the structural problems are all back on display.

Volumes are collapsing because the housing market is frozen. Existing home sales are stuck near multi-decade lows. New construction has slowed. R&R spending has softened. Consumers are trading down or deferring projects.