Is AI Going To Kill Gartner ($IT)?

The equity is down 70%. The bonds are still IG.

Is AI going to kill Gartner?

That’s the only question worth asking and management keeps answering a different one. DOGE. Tariffs. Budget pressures. Blame it on the cycle and offer a $2bn buyback program to make shareholders happy.

The equity market isn’t buying it and for good reason. Here’s Gartner’s Magic Quadrant, the product that built the brand. November 2025, generative AI model providers. IBM ahead of Anthropic. That’s all you probably need to know.

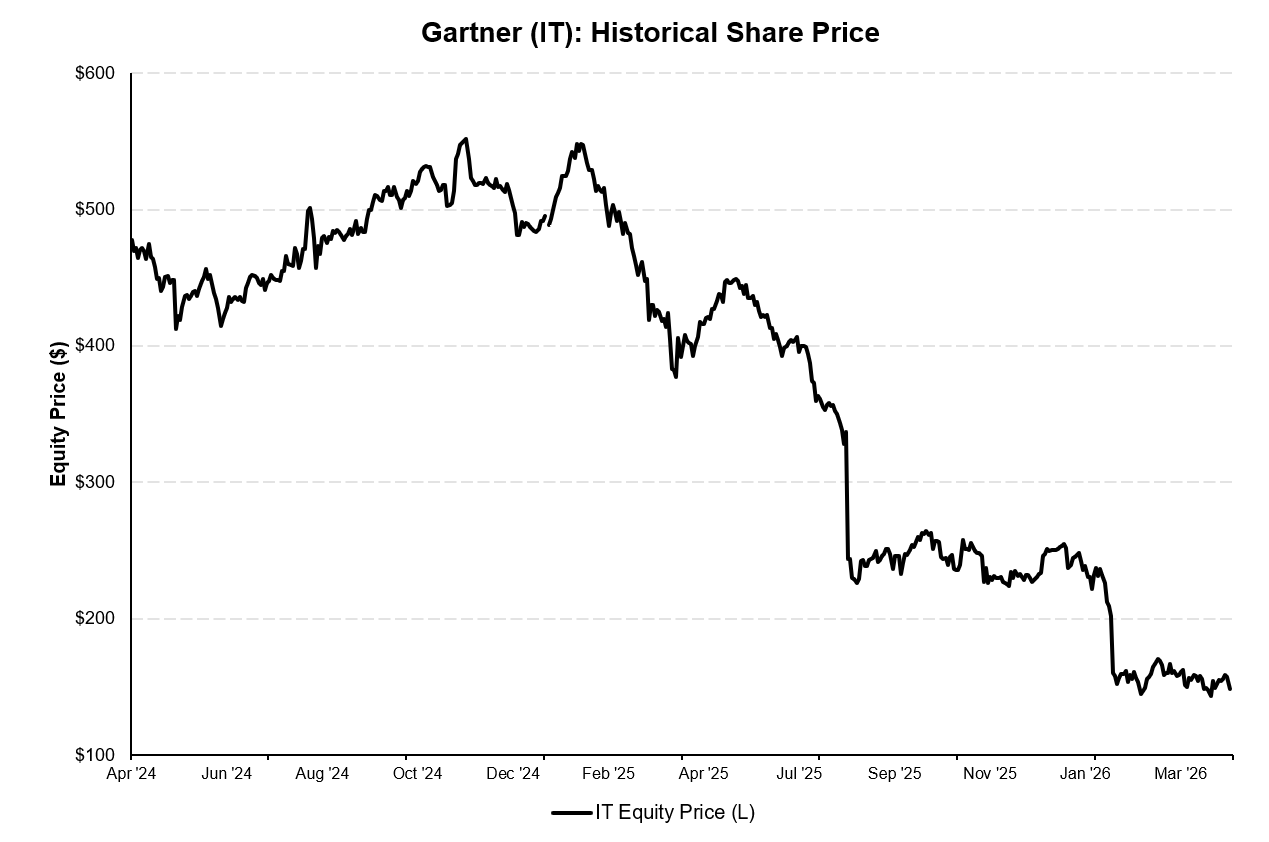

The stock is down more than 70% from its highs including 38% this year alone. Roughly $20bn of market cap vaporized. All due to multiple re-rating. Two separate single-day moves north of 20% after earnings.

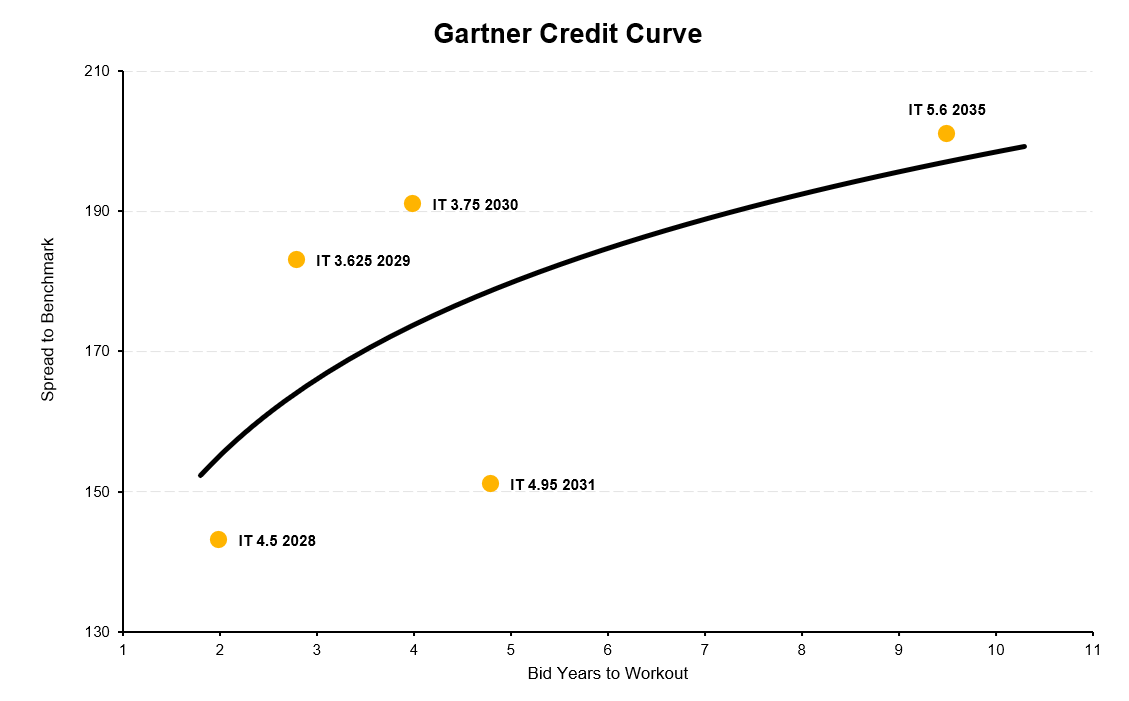

Meanwhile, the bonds have barely budged. The 2028s at 140 over, the 2031s at 150, the 2035s at 195 bps. Held by sleepy long-only IG investors running a screen that still shows sub-1x net leverage, 70%+ FCF conversion, and an IG rating. A healthy business on the spreadsheet.

But is it really?

The Business Model

Gartner (NYSE: IT) is a ~$6.5bn revenue enterprise technology research and advisory firm, headquartered in Stamford, CT, with ~21,000 employees globally.

The business model works like this: pay an annual fee per seat, somewhere between $20,000 for basic research access and $80,000-plus for senior advisory, and whoever holds that seat can read Gartner reports, call a Gartner analyst, tap into peer networks, and attend Gartner conferences.

You know the magic quadrants every company references? That’s them.

The product is basically credentialed human expertise on technology decisions, originally aimed at IT leaders and, since the 2017 CEB acquisition, extended into HR, finance, legal, procurement, marketing, and supply chain.

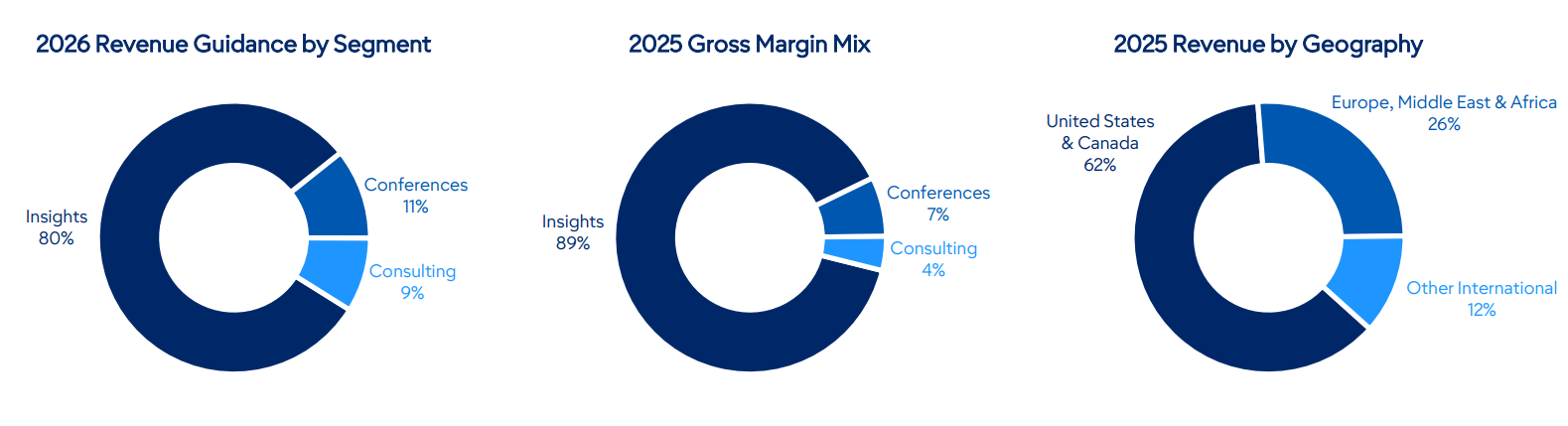

The company operates under three segments, each with different economics.

Insights: the subscription research engine. ~77% gross margins, ~90% of gross profit. ~14,000 enterprise clients across GTS (tech vendors) and GBS (functional leaders outside IT).

Conferences: ~50 events a year, anchored by Symposium/Xpo. Blended ~45% gross margins. Revenue from attendee tickets plus sponsor fees from vendors paying to reach the audience.

Consulting: small, project-based, contracting. ~27% gross margins. Contract optimization, sourcing, and benchmarking work sold into existing Insights accounts.

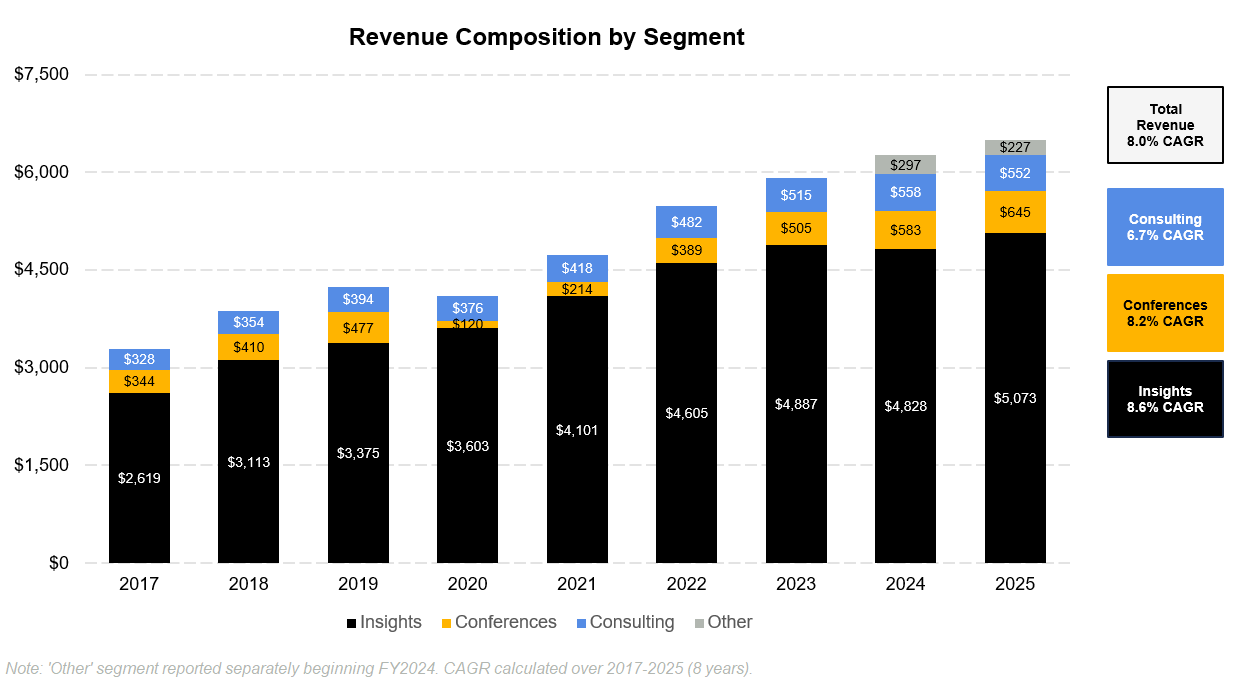

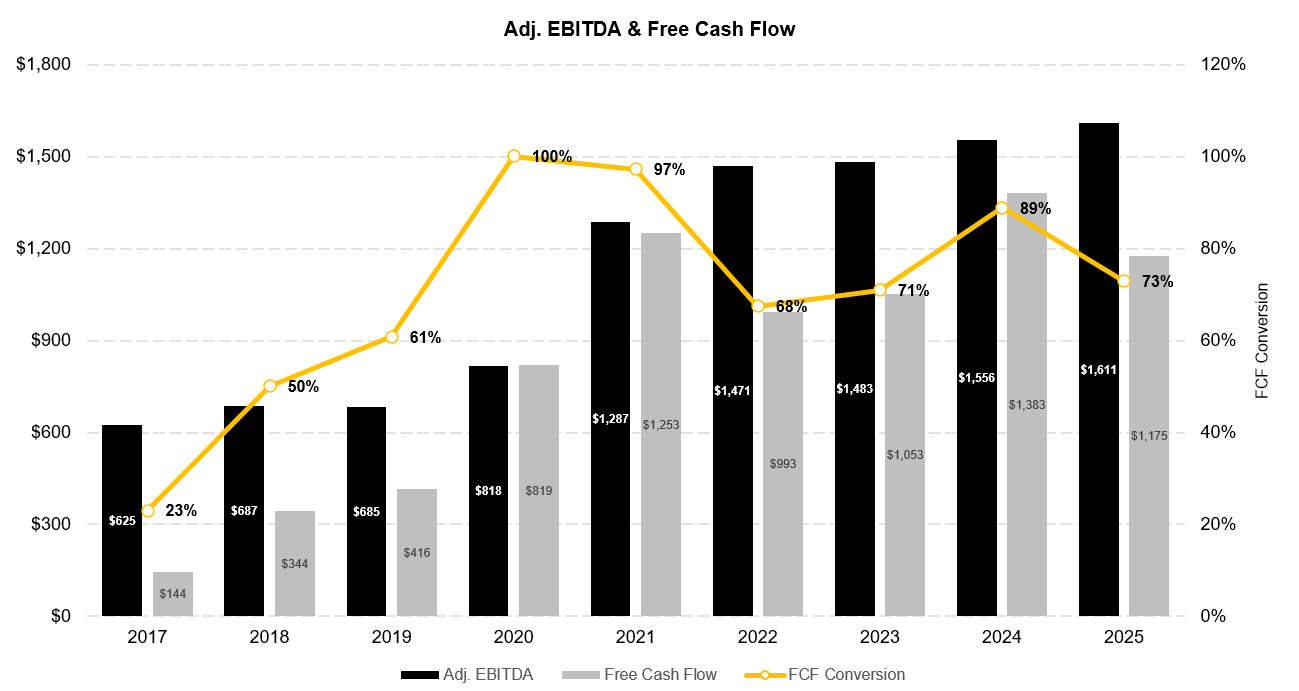

Contract Value (CV), the annualized book of active subscriptions, closed FY’25 at roughly $5.2bn. Clients pay annually and upfront, which coupled with minimal capex (<2% of sales), translates into robust FCF generation (70%+ FCF conversion).

What's Been Happening

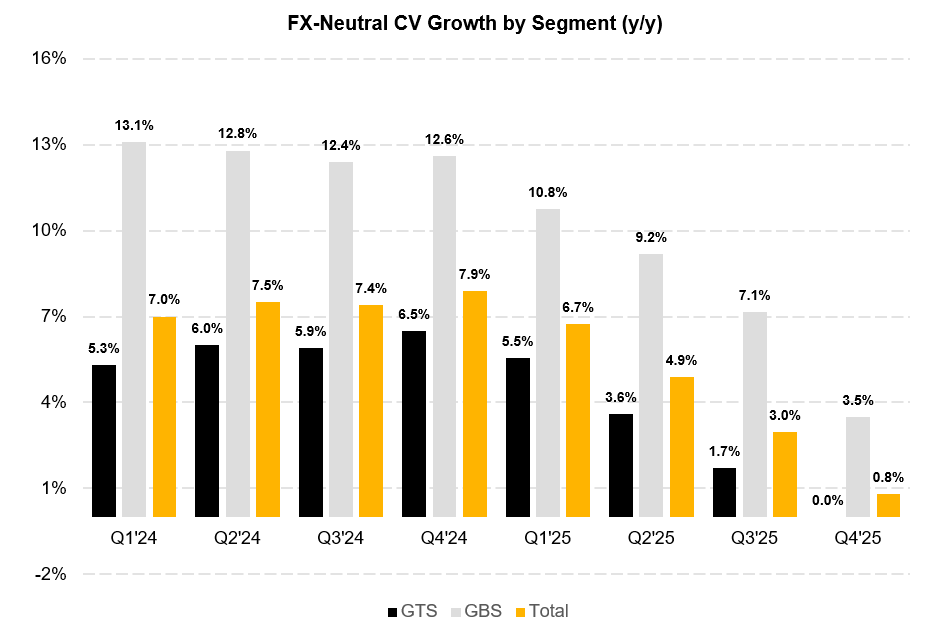

The last 18 months at Gartner have been rough. CV growth, the metric the whole business ladders up to, has decelerated every quarter for four straight quarters. FY’24 exited at 8%. Q1’25 printed 5%. Q2 came in at 3%. Q4 at 1%, well below what consensus had modeled. Four consecutive misses against a progressively lower bar.

The equity has repriced accordingly. IT is down more than 70% from its FY’24 high of ~$584, with most of the damage concentrated in two single-day drops of 20%-plus following Q2’25 and Q4’25 earnings.

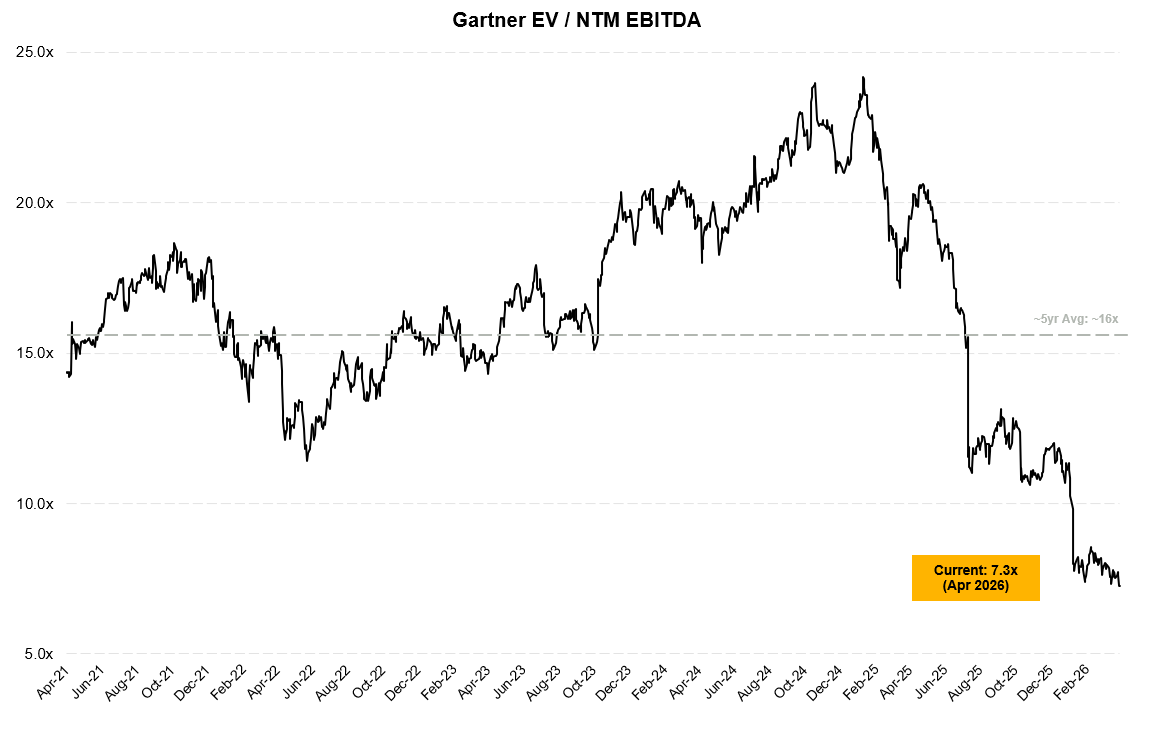

The multiple expansion that drove the stock through 2022-2024 has fully unwound and now hovers around ~7x NTM EBITDA.

Management’s explanation has been consistent and cyclical:

DOGE: federal contract cancellations running at dollar retention near 50%, with the bulk of the renewal cohort concentrated in FY’25.

Tariffs: 35-40% of the client base sits in tariff-exposed industries where capex cycles have stalled.

Macro: cost-cutting across the enterprise base has stretched sales cycles and pushed existing accounts to trim seats at renewal.

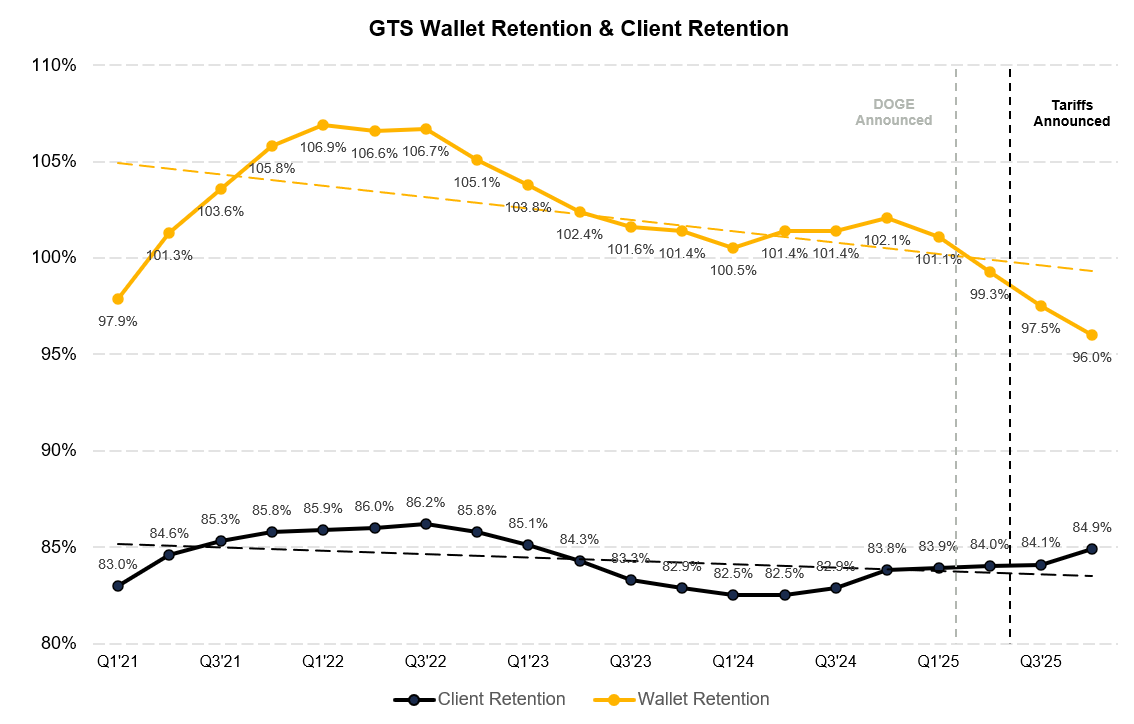

The numbers beneath the CV headline are worse than the headline. GTS wallet retention, which measures how much existing clients spend at renewal versus the prior year, has fallen from 108.8% in FY’21 to 97.5% in FY’25. A book that used to quietly expand inside every account is now, in aggregate, shrinking inside them.

Inside that number, the small tech vendor cohort is the single largest drag. Gartner has called out small tech vendors as the primary driver of client count decline for multiple quarters in a row, with retention in that cohort running in the low-to-mid 70s.The deterioration started in FY’22 and has been uninterrupted since. DOGE and tariffs are FY’25 problems.

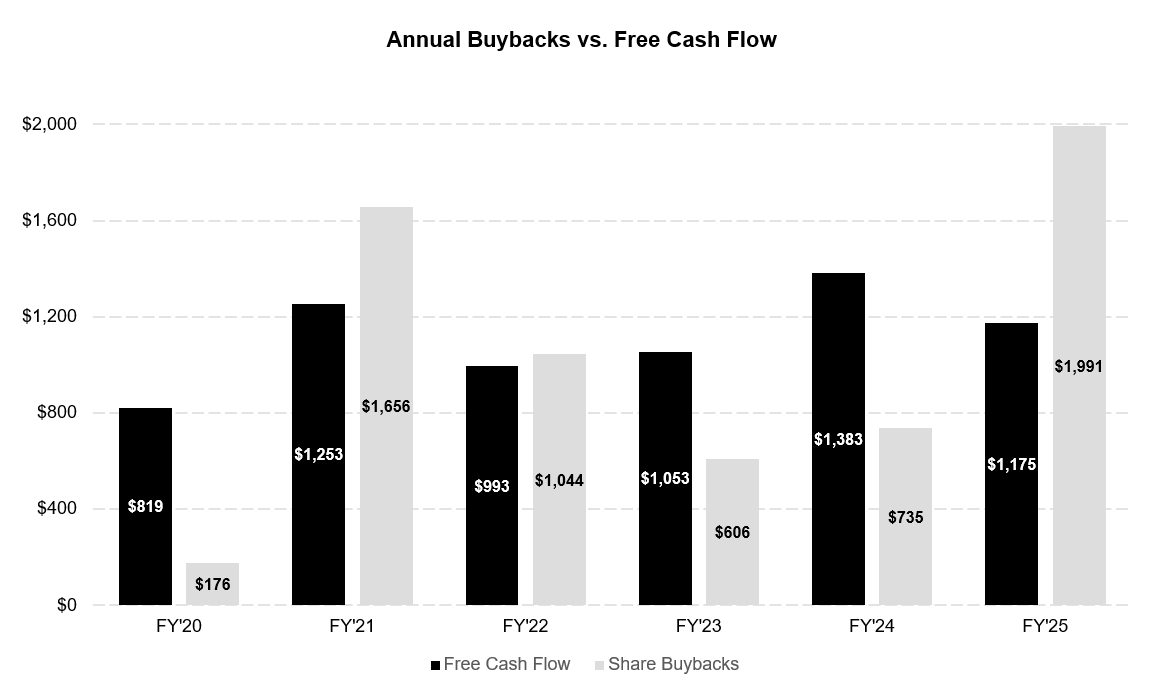

Management’s response has been to double down on capital return rather than change the business. FY’25 buybacks hit nearly $2bn against ~$1.2bn of FCF, the largest annual repurchase in company history, funded partly by drawing down cash and using incremental debt capacity. Another $1.2bn of authorization remains.

On recent calls, management has pointed to AskGartner adoption and analyst productivity gains as evidence the product transformation is working and CV will reaccelerate through FY’26-27.

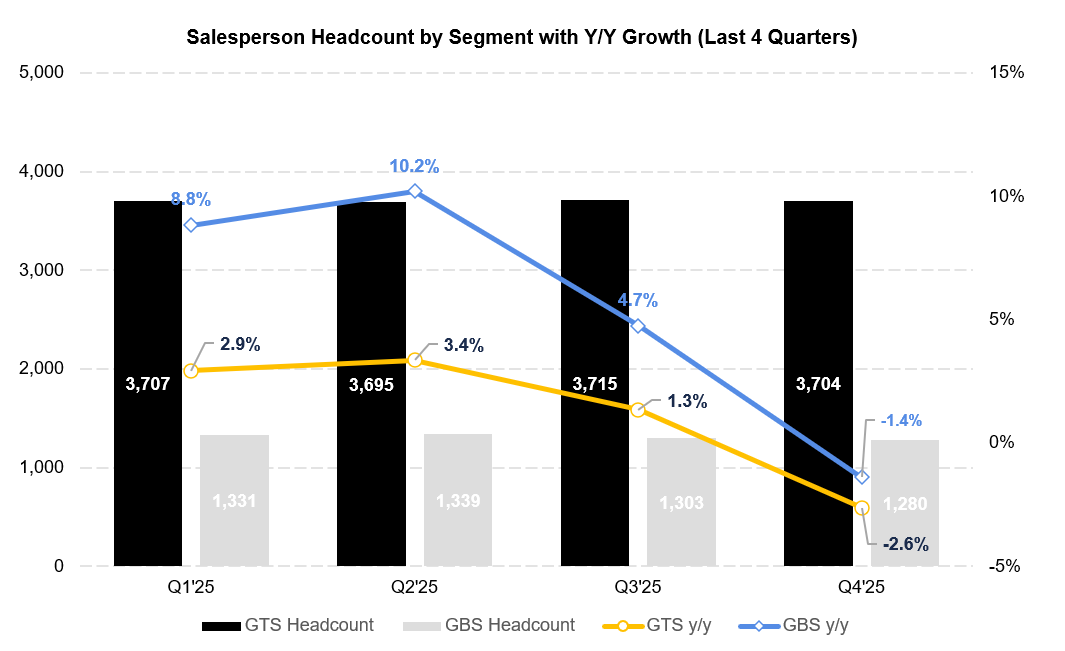

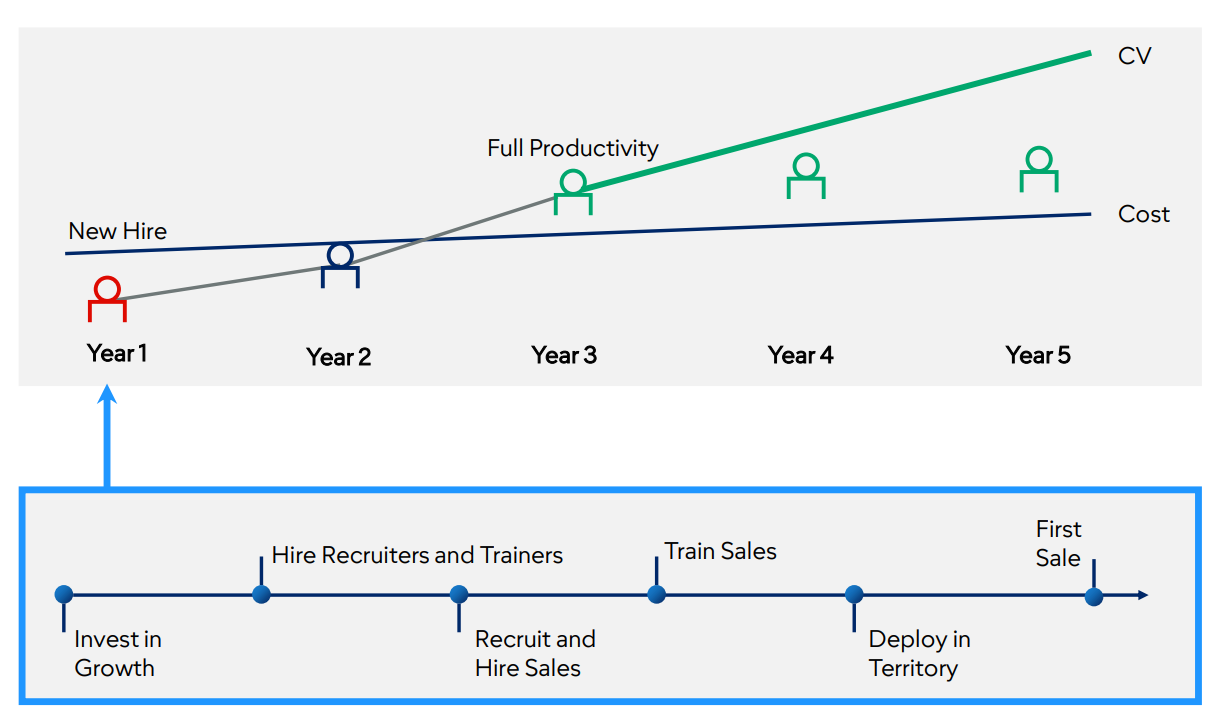

The salesforce situation makes the setup worse. Quota-bearing headcount (QBH, the seat-selling reps that carry the renewal and new-logo targets) was reduced through FY’25, which pulled down average rep tenure at the same time the book turned.

Gartner reps take three to four years to ramp. Even assuming a cyclical recovery in FY’26, the salesforce that would need to capitalize on it is less tenured than the one that navigated prior cycle troughs. Any rebound will be shallower than historical comparisons suggest. Unsurprisingly, salesperson productivity has declined in lock-step.

Here’s what the bond market is saying.