HY Market Weekly Minutes: Spreads Hit Post-GFC Lows Amid Economic Resilience (October 18, 2024)

A Brief Recap of Last Week's High Yield Market Performance

🚨 Connect with me on Twitter / Instagram / Threads | Estimated Read Time: 6 Minutes

Just when you thought the high yield market couldn’t get any hotter, it’s gone and surprised everyone again. Last week, spreads tightened to near post-GFC tights, fueled by a mix of robust consumer spending (retail sails more than doubled expectations) and a resilient labor market (jobless claims at the lowest level since May). It seems the “soft landing” narrative is alive and well, with investors piling into riskier assets.

The numbers also tell a compelling story: a +0.34% return for the week, pushing YTD gains to +7.86%. But it’s not just the broad strokes that are impressive—CCCs are significantly outperforming their higher-rated peers, delivering a jaw-dropping 13.44% return so far this year. Meanwhile, primary issuance has slowed to a trickle, with just $3.675 billion hitting the market last week. It’s a perfect storm for spread compression, and issuers lucky enough to tap the market are finding investors falling over themselves to get a piece of the action. Case in point: Chobani’s recent CCC-rated, HoldCo PIK Toggle note offering saw $4 billion of orders for a $650 million deal.

As we head into the heart of earnings season, all eyes are on whether this rally has legs or if we’re due for a reality check. Either way, it’s going to be an interesting ride. Let’s dive in.

Weekly Performance Recap

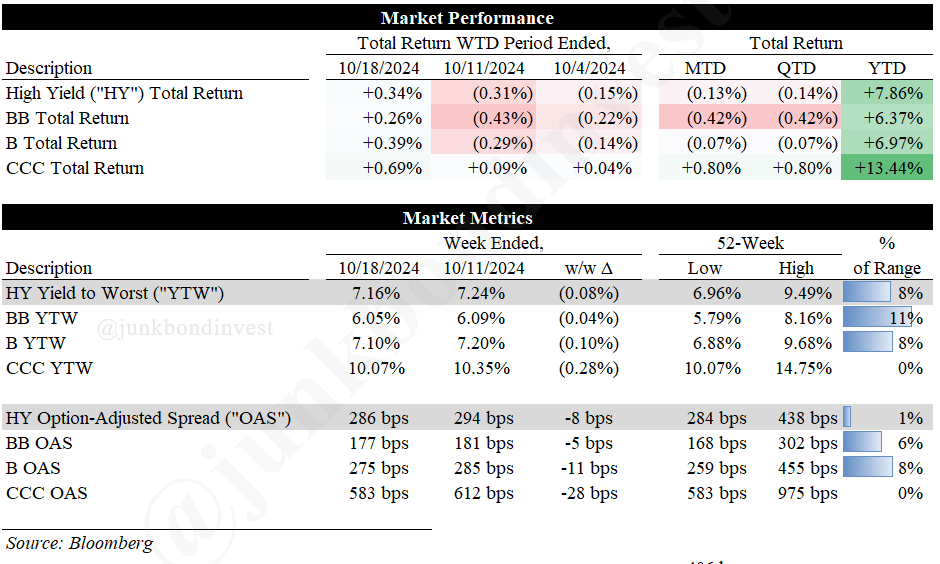

For the week ended October 18th, the high yield market rebounded strongly, with the overall index returning +0.34%. This positive performance has partially offset earlier losses in October, bringing month-to-date (MTD) returns to -0.13% and year-to-date (YTD) returns to an impressive +7.86%.

The high yield market’s strong performance has been underpinned by surprisingly resilient economic data. September’s retail sales surged 0.7% month-over-month, more than double expectations, reinvigorating the “soft landing” narrative. Labor market strength persists, with jobless claims at their lowest since May, supporting consumer spending and corporate revenues.

Breaking down performance by rating category:

BBs returned +0.26%, bringing YTD returns to +6.37%

Bs returned +0.39%, with YTD returns now at +6.97%

CCCs continued their outperformance, returning +0.69% for the week and pushing YTD returns to +13.44%

The persistent outperformance of CCCs, which have now delivered a 13.44% YTD return, highlights the market’s continued appetite for risk, even as spreads reach historically tight levels. This trend is particularly noteworthy given the >700bps outperformance of CCCs over BBs YTD.

Noteworthy Market Metrics:

OAS tightened by 8bps to 286bps, reaching near post-GFC lows. This represents a 154bps tightening YTD.

The overall YTW for the HY market decreased by 8bps to 7.16%, reflecting both spread tightening and a slight decline in Treasury yields.

High yield primary issuance volumes decreased to $3.675 billion across just three deals, marking the lightest issuance week since August and a 21% decrease from the previous week’s $4.66 billion.

YTD issuance now stands at an impressive $255.1 billion, of which $59.3 billion is non-refinancing related. This significantly outpaces the $136.5 billion seen in the same period last year, representing an 87% y/y increase.

The telecom sector led October performance with a +1.00% return, while utilities lagged at -0.48%.

Primary Market Activity

The primary market saw a significant slowdown this week, with volumes reaching only $3.675 billion across three deals. This brings the October total to $15.4 billion, of which $6.1 billion is non-refinancing related, compared to the monthly average of $31.6 billion gross and $5.9 billion net for the first nine months of the year. The decrease in issuance can be attributed to the Columbus Day holiday and the ramp-up of the Q3 earnings season.

Standout Transactions:

Jane Street’s $1.15 billion offering of eight-year senior secured notes, upsized from $1 billion, priced at par to yield 6.125%.

NRG Energy’s $1.875 billion dual-tranche offering, upsized from $1.5 billion, consisting of 8.25-year and 10-year senior unsecured notes priced at par to yield 6% and 6.25% respectively. The Ba2/BB rated deal will be used to refinance existing debt.

Chobani’s $650 million offering of five-year PIK toggle notes, upsized from $500 million, priced at 99 OID to yield 9%. The Caa1/CCC+ rated deal saw an impressive $4 billion of demand.

These transactions underscore the continued appetite for high yield debt, with all deals being upsized and pricing at or below the tight end of guidance.

Secondary Market Dynamics

As the November Fed meeting approaches, rate cut expectations have moderated. The market now prices just a 40% probability of another 50bps cut this year, down from earlier projections. This recalibration is driving investors towards riskier assets, evident in CCC outperformance. The secondary market showed strong performance last week as investors processed robust economic data and positive corporate earnings.

Looking Ahead

As we head into the heart of earnings season, the high yield market is walking a tightrope. With spreads at levels that would make pre-GFC investors blush, the million-dollar question is: how long can this party last?

The next few weeks could be a rollercoaster ride, with corporate earnings at the forefront. Strong numbers could send spreads even tighter, while any significant misses might finally cause spreads to widen. And let’s not forget our friends at the Fed—any unexpected hawkish turns could throw a wrench in the works. 10-year Treasury yields have already climbed over 40bps in the past month, reaching 4.08%. This uptick is pressuring all-in yields, even as spreads compress. Meanwhile, geopolitical tensions are simmering in the background, ready to boil over and threaten the energy sector, which comprises about 14% of the high yield index.

Lastly, over $100 billion of high yield bonds are now flirting with their call prices, setting the stage for a potential refinancing bonanza. This could flood the primary market with new issues, testing just how deep investor pockets really are. Hold onto your hats—the next few weeks promise to be anything but dull.

Jobs in Credit:

💡 Have a job opening? I’m open to having you publish— drop me a message!

One of my long-time followers is hiring a credit associate. Check it out here👇

Find the most recent JunkBondInvestor posts below

Disclosure: The information provided is for informational purposes only and should not be considered as investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release me from any liability. Seek professional advice tailored to your financial situation and objectives.