HY Market Weekly Minutes: Credit Defies the Equity Selloff...But Will It Last? (April 21, 2025)

A Brief Recap of Last Week's High Yield Market Performance

🚨 Connect with me on Twitter / Threads / Instagram / Bluesky | Estimated Read Time: 5 Minutes

Something new is coming.

Built for people who actually care about credit. If you want a first look before it opens up, join the early access list — limited spots.

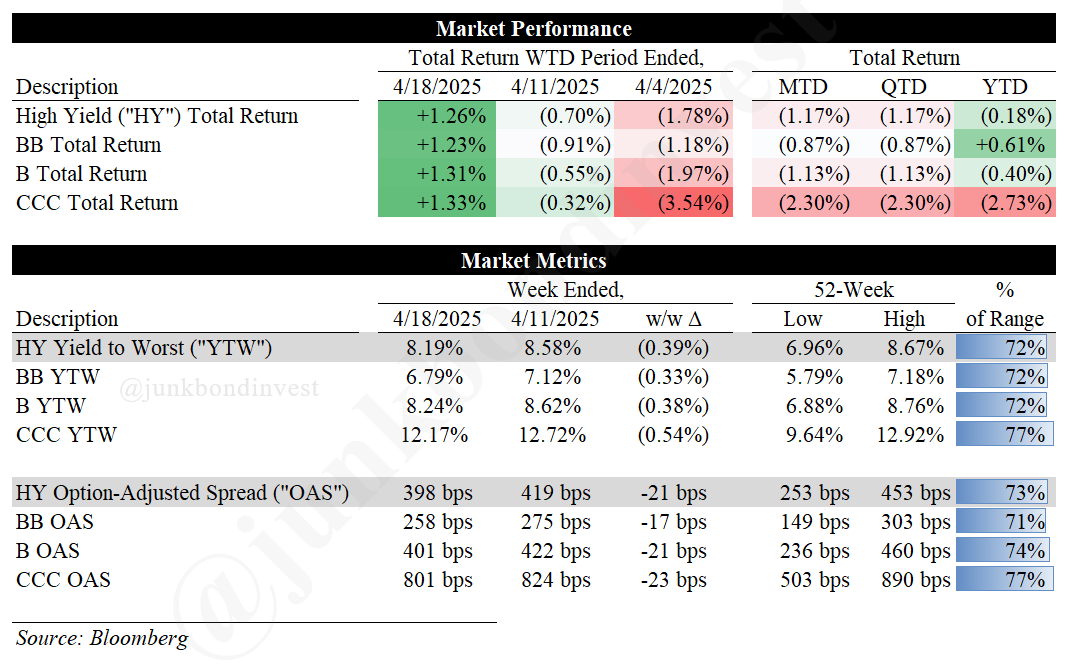

The divergence was stark. High yield outperformed last week, with the index posting a solid +1.26% return as spreads tightened 21bps to 398bps despite continued equity market weakness. Whatever the explanation—flight to yield, technical positioning, or just a natural rebound—junk bonds staged their biggest weekly rally in months even as Trump’s confrontation with Powell intensified.

The spread tightening was particularly striking considering recent market turmoil. High yield has now partially recovered from its April selloff, though still trading significantly wider than Q1 levels. With dealer positioning lean and minimal primary market activity, the supply-demand dynamic couldn’t be more favorable. Short-dated paper, which faced the heaviest selling during the tariff panic, has found renewed interest from opportunistic buyers.

Rate stability provided the foundation. Index yields fell 39bps to 8.19% as investors gravitated to credit, with CCCs gaining 1.33% and their yields dropping 54bps to 12.17%. The compression across quality segments was notable—BB spreads tightened 17bps to 258bps while CCC spreads narrowed 23bps to 801bps, showing investors’ increased comfort moving down the quality spectrum on oversold credits.

But the critical question remains: is this recovery sustainable, or merely a temporary reprieve in a deteriorating macro environment? The economic data presents a puzzling contrast—solid retail sales and manufacturing figures vs. plummeting confidence measures. Add in Trump’s unprecedented criticism of Fed independence, and the uncertainty couldn’t be higher.

Unfortunately, this week is already suggesting last week’s rally may have been premature. Credit markets have reversed course with synthetics already widening 20bps to 445bps amid renewed concerns about Fed independence and global trade tensions. The Monday selloff serves as a stark reminder that we’re not out of the woods yet.

Weekly Performance Recap

Last week’s performance was impressively strong across all quality segments:

High yield returned +1.26%, improving MTD returns to -1.17% and YTD to -0.18%

BBs gained +1.23%, maintaining their YTD positive territory at +0.61%

Bs outperformed slightly at +1.31%, though still negative YTD at -0.40%

CCCs matched the rally at +1.33%, but remain deeply underwater YTD at -2.73%

The technical picture showed significant improvement:

Overall index yields dropped 39bps to 8.19%, now at 72% of their 52-week range

Spreads tightened 21bps to 398bps, breaking back below the psychologically important 400bps level

CCC yields fell 54bps to 12.17%, still relatively elevated at 77% of their 52-week range

The compression across ratings categories suggests investors were actively embracing risk again after several weeks of defensive positioning. However, with Monday’s significant widening, much of this improvement is already being erased.

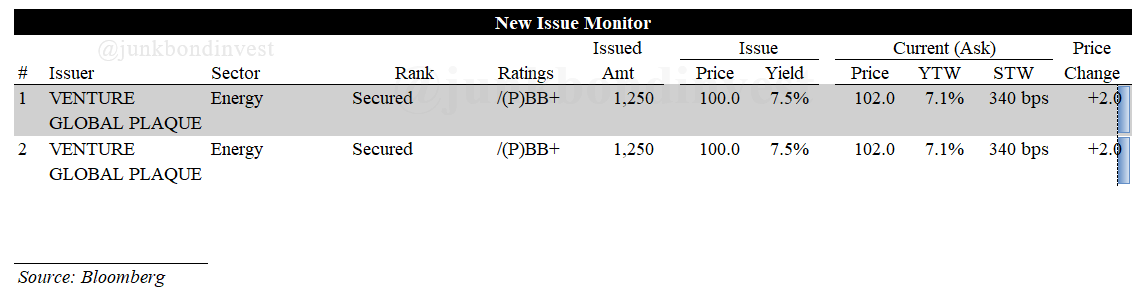

Primary Market Activity

The primary market showed the first signs of reopening, breaking its multi-week hibernation with a single $2.5 billion high yield bond transaction. The two-tranche offering was split between 8-year and 10-year maturities, yielding 7.5% and 7.75% respectively, and performed well in secondary trading.

This lone deal provided a tentative signal that primary markets are beginning to thaw following the April volatility. The strong secondary performance helped recently issued bonds recover some of their recent price declines, suggesting investors remain receptive to new supply despite the challenging environment.

The limited calendar continues to reinforce the technical backdrop. With ongoing uncertainty surrounding trade policy and corporate guidance, many potential issuers remain on the sidelines, creating an imbalance that has temporarily benefited bondholders. The pipeline is expected to gradually rebuild, but likely at a measured pace given the volatile backdrop.

Secondary Market Dynamics

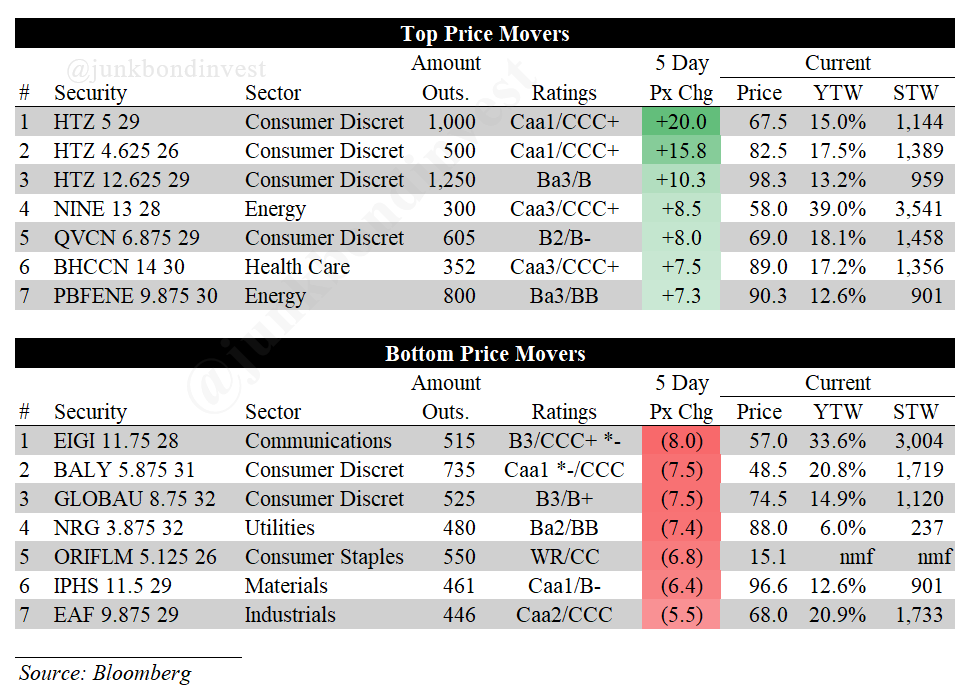

The secondary market showed broad improvement last week, with cash closing significantly higher and halting the previous losing streak. Trading patterns revealed changing investor sentiment beneath the surface, with investors emerging for both higher-quality names and higher-yielding credits.

The week’s standout performer—Hertz—saw its bonds surge 15+ points after Ackman disclosed a substantial equity stake, significantly improving the company’s near-term liquidity profile. Meanwhile, Wednesday’s session perfectly illustrated high yield’s resilience—hawkish comments from Powell drove equities down sharply, yet credit remained remarkably stable.

Looking Ahead

The market faces a pivotal week as we enter the heart of earnings season. With Trump’s remarkable attack on Powell introducing unprecedented uncertainty, investors must navigate both political and economic challenges simultaneously.

Three key developments will shape this week’s narrative:

Housing data (Wednesday/Thursday): New and existing home sales are expected to soften as affordability remains challenging despite modest declines in mortgage rates. Builder sentiment data already shows growing concerns about future sales prospects.

Durable Goods (Thursday): Expected to show modest growth in March, this report will reveal whether capital investment plans are being curtailed amid trade uncertainty. Business capital spending intentions remain subdued as companies await clearer policy direction.

Political developments: The extraordinary criticism of the Fed Chair’s independence has roiled markets, with demands for immediate rate cuts while questioning Powell’s job security. Any escalation could trigger additional volatility across all asset classes.

The contradiction in current economic conditions couldn’t be more pronounced—strong retail activity and industrial production vs. deteriorating confidence measures and expectations. This disconnect between current data and forward-looking indicators creates a particularly challenging environment for corporate planning.

The direction from here likely hinges on whether the administration continues its confrontational approach or pivots toward more market-friendly messaging. For now, credit investors must contend with this morning’s significant spread widening, serving as a sobering reminder that last week’s rally may have been more technical than fundamental.

Find the most recent JunkBondInvestor posts below

Disclosure: The information provided is based on publicly available information and is for informational purposes only. While every effort has been made to ensure the accuracy of the information, the author cannot guarantee its completeness or reliability. This content should not be considered investment advice. Any investment decisions made based on the information provided are at your own risk. It is essential to conduct your own research and consult a qualified financial advisor before making any investment decisions. Investing involves risks, and past performance is not indicative of future results. By using this information, you acknowledge that you are responsible for your own decisions and release the author from any liability. Always seek professional advice tailored to your financial situation and objectives.