HY Market Weekly Minutes: Credit Cracks Wide Open...as Tariffs Turn the Screws & Consumer Confidence Collapses (March 17, 2025)

A Brief Recap of Last Week's High Yield Market Performance

🚨 Connect with me on Twitter / Threads / Instagram / Bluesky | Estimated Read Time: 7 Minutes

The tariff tremors are turning into full-blown market quakes. High yield just posted its second consecutive weekly loss for the first time since December, with the index down -0.67% last week and spreads widening 30ps to close at 321bps. That’s the largest weekly widening in two years, and we’re still digesting the fallout.

The technical damage is spreading. Fund flows finally cracked with an outflow, breaking a seven-week inflow streak dating back to mid-January. Meanwhile, the primary market slowed dramatically with only $4.0 billion pricing across 8 deals—half the prior week’s volume. The quality of execution tells the real story: deals that could get done were forced to pay higher new issue concessions than usual, and tariff-exposed issuers priced at the wide end of talk before trading lower.

But here’s what’s really interesting: Wednesday’s softer-than-expected CPI—which would normally spark a rally—barely registered amid the tariff noise. By Thursday, yields and spreads were at their highest since summer before a modest Friday rally provided some relief.

What’s changed? For the first time this cycle, we’re seeing clear evidence of consumer stress. Delta’s surprise guidance cut revealed demand fell off a cliff in February and March. Less-than-truckload providers reported volumes down ~7% in February. This isn’t just about tariffs anymore—it’s about demand destruction in real time.

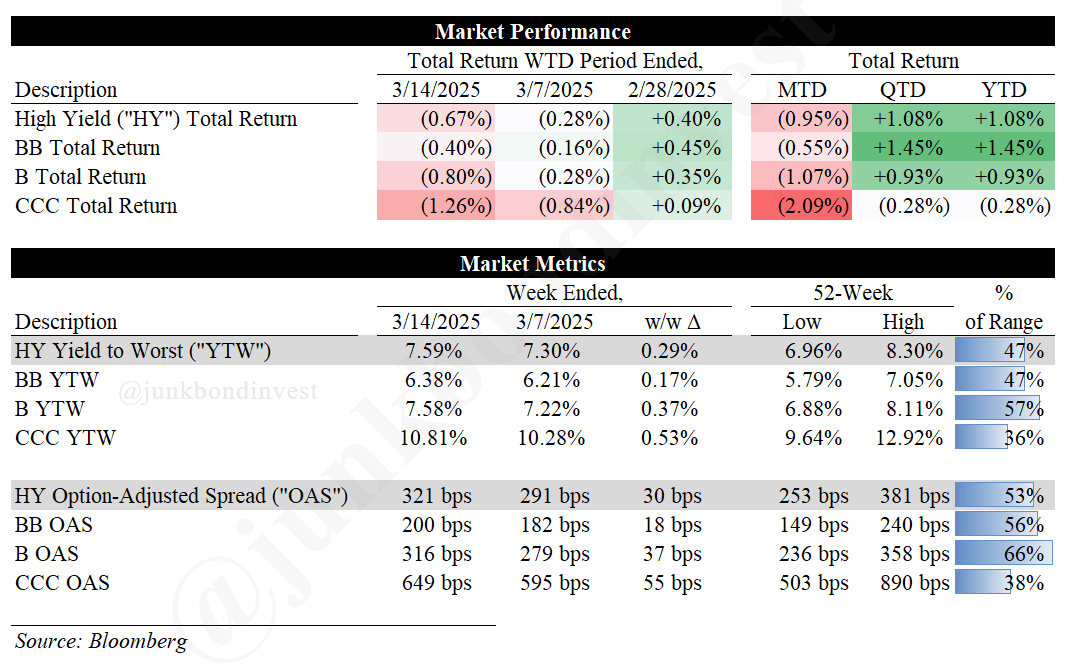

Weekly Performance Recap

The numbers reveal a market under genuine stress. Overall HY lost -0.67% for the week, with credit quality making all the difference:

BBs suffered the least at -0.40%, showcasing the continued flight to quality

Bs underperformed at -0.80%

CCCs significantly lagged at -1.26%, their worst weekly performance in months

The technical picture deteriorated markedly:

Overall index yields jumped 29bps to 7.59%, now at 47% of its 52-week range

Spreads dramatically widened 30bps to 321bps, with CCCs experiencing the largest move at +55bps to 649bps

Meanwhile, Treasury yields barely moved despite equity market turbulence, with the 10-year closing just 1bp wider at 4.31%. This disconnect highlights how credit-specific this selloff has become.