Credit Weekly: The Repeat Game

Sponsors know lenders can't run companies. They're playing that.

🚨 Connect: Twitter | Instagram | Reddit | Job Board

The capital structure says you win. The relationship says otherwise.

Not in every deal. But in enough of them that the current conversation is incomplete in ways that matter.

The logic is intuitive. Private credit sits senior in the stack. Equity is first loss. If the business deteriorates far enough, the sponsor gets wiped and the lender takes the keys with value to spare. That is the theory.

It is also incomplete. Senior secured does not mean unimpaired. It means you get paid before the equity. In a real workout, that gap between theory and recovery can swallow a lot of NAV.

And the math ignores the room.

Lenders don’t run companies. The deal team that got comfortable after five GLG expert calls, a sponsor-provided McKinsey report, and a 20% haircut to the sponsor model is not suddenly equipped to manage a 500-person global manufacturing business through a workout. That is not a knock. It is just reality. Underwriting a business and operating one are different skills. The credit community has exactly zero of the latter.

Sure, management runs the business and the incentive plan gets reset. But management ran the day to day. The sponsor ran the strategy. A reset MIP does not replace that. The best people in the building figure that out first. They are also the ones with the most options.

So what actually happens when a deal goes sideways?

Take the keys, or negotiate. Almost every time, they negotiate. Blackstone knows this. KKR knows this. Apollo knows this. The threat of taking the keys is not a threat to the sponsor. It is a threat to the lender’s time on every other position in the fund.

Here is the hypothetical conversation happening in workout rooms that nobody is writing about.

Blackstone sits across from a direct lender on a bad vintage deal. Nobody saw the tariff exposure, or the AI disruption, or whatever the problem turned out to be. Blackstone says: we can hand you the keys today. Or we can extend the maturity, restructure the debt, roll some equity into a new structure, give you upside participation on the recovery. We stay, we operate it, we try to get you out whole.

And then comes the part that does not appear in any textbook:

We have significant upcoming deal flow. The kind you have been trying to get allocation on for two years. This was a bad vintage. We are prepared to treat it as one. But if you play hardball here, we will remember that when the post-dislocation cycle opens up. Maybe your competitor gets that allocation instead.

Tell me that conversation does not happen and the lender does not blink.

Direct lending is a repeat game with a very small number of counterparties. A lender who torches a relationship over one bad deal is making a locally optimal, globally irrational decision. The sponsors know the math. They are playing it.

This is not a universal law. It is a practical reality that shapes how a meaningful number of these situations actually resolve. And it depends entirely on the sponsor.

There are a lot of zombie PE firms out there right now. Funds that are not raising another flagship. Funds where the deal flow argument carries no weight because there is no deal flow. When the sponsor has no future leverage the negotiating dynamic collapses. And that actually makes the point sharper. The strategic value of a top-tier sponsor relationship becomes more important precisely because it is scarce. Lenders know who is going to be in business in five years. That calculus is in every conversation whether anyone says it out loud or not.

The lenders underwrote the business. The sponsors know how to run it. Those are two very different things. And in a stressed credit, only one of them matters.

That dynamic is playing out against a backdrop that makes the workout math harder across the entire credit complex. Not just in private credit.

The Workout Is the Easy Part

The dominant narrative is AI disruption layered on an Iran oil shock. Both real. Both getting all the analytical resources. Both obscuring something building in completely different parts of the credit universe.

Old-fashioned credit stress is broadening. Nothing to do with software or the Strait of Hormuz.

Start with non-prime consumer lending. Non-prime borrowers have the least buffer and crack first. When non-prime lenders are in covenant discussions with their own securitization lenders the question is not whether consumer stress exists. The question is how far up the income ladder it has already traveled. Further than the headlines suggest.

Building products is running a parallel script. Margin compression with no macro catalyst attached to it. Soft housing. No policy support. PE-backed structures leveraged for a rate environment that never materialized. Pure cyclical deterioration in a sector that has nothing to do with AI or geopolitical risk. Nobody is writing about it because there is no narrative hook. The stress is just there, quietly compounding.

Airlines are the same story with a more visible mechanism. Unhedged fuel exposure, no pricing power, and an oil shock doing what oil shocks do. This one does not get better while crude stays at $100.

Three sectors deteriorating simultaneously for completely different reasons. The market is calling this a sector rotation. It isn’t.

One more thing on Iran that is not getting airtime. The focus has been entirely on the oil price. Almost nobody is modeling what a sustained Hormuz disruption does to trade finance. Letters of credit. Shipping insurance. Working capital facilities for companies with Asian supply chains. These reprice quietly when underwriters decide a major global chokepoint is under active military threat.

The oil price move is visible and already in spreads. The trade finance tightening is not. If this disruption runs another 60 to 90 days the second-order effects start showing up in working capital lines and covenant calculations at companies where your credit model currently says nothing is wrong. By the time it is legible in the data it will already be in the price.

All of this matters for the workout dynamic described above. Every incremental deterioration in the macro backdrop narrows the sponsor’s negotiating options and widens the gap between what the lender can recover in theory and what they can recover in practice. The repeat game gets more expensive to lose every week.

The Market Is Solving for the Wrong Variable

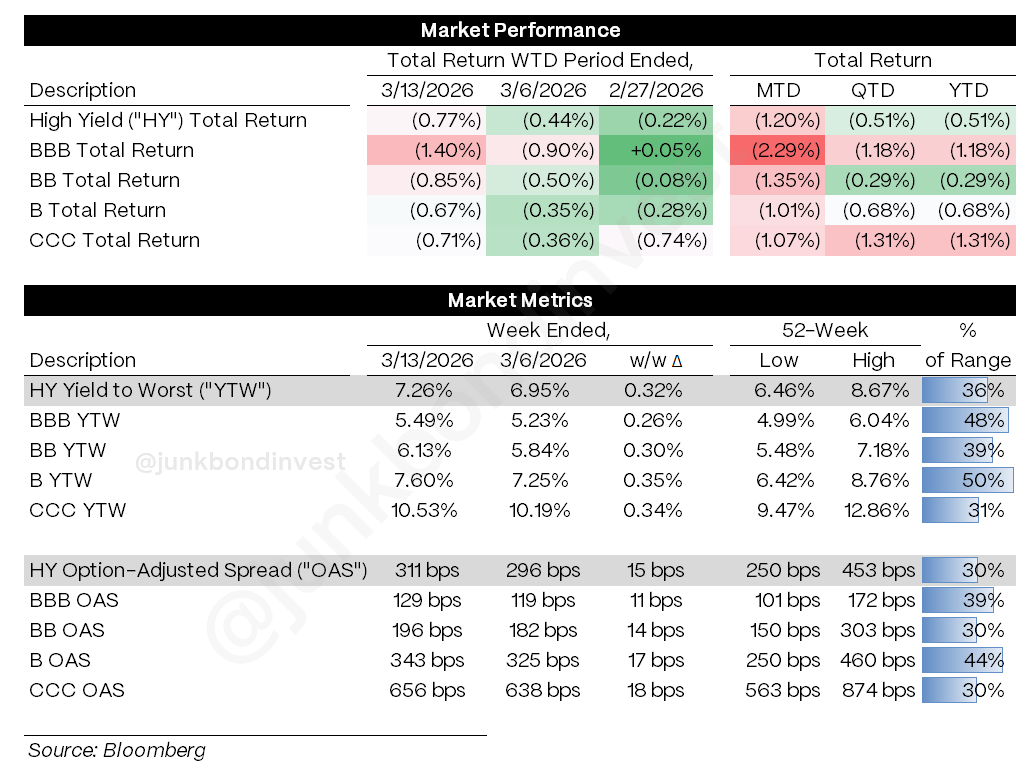

HY BBs are down 1.35% month to date. CCCs are down 1.07%. In every risk-off episode in recent memory quality outperforms. Everyone learned that playbook. Everyone is currently executing it.

It is the wrong playbook.

BBs are the worst performing ratings bucket in high yield right now and the reason has nothing to do with credit quality. The 10-year moved ~25bps wider this month. BBs carry the most duration in high yield. The accounts that historically stabilize the BB tier in a risk-off move, crossover IG buyers, insurance companies, total return funds, are themselves forced sellers when rates spike this fast. The natural shock absorber for BBs in a risk-off environment becomes a source of supply in a rates-driven one.

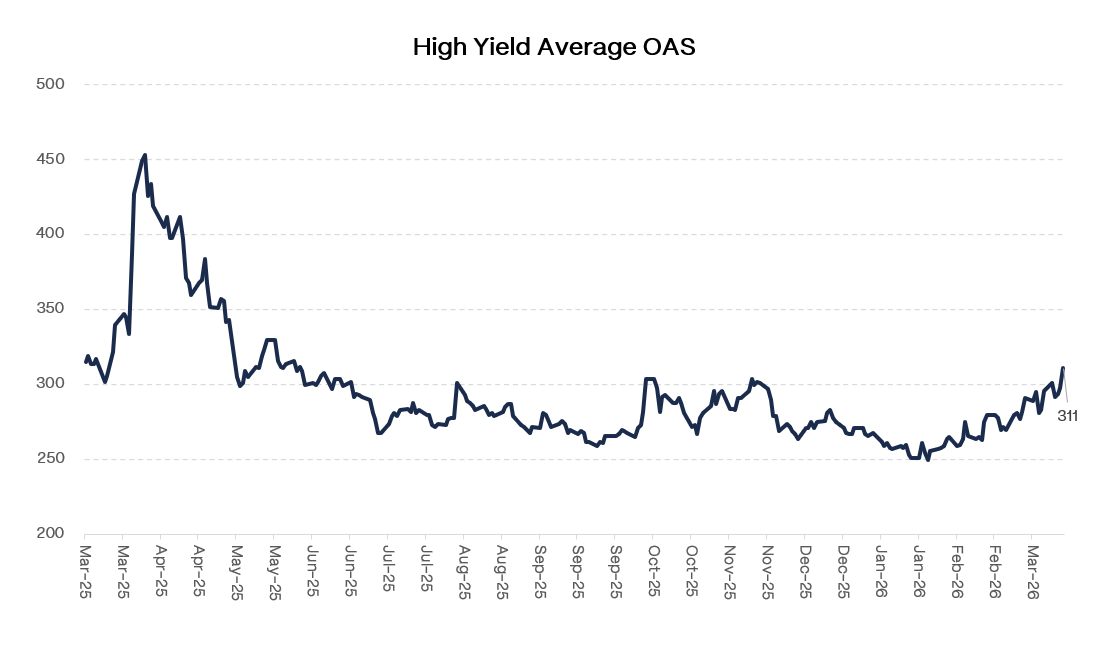

This is a rates selloff dressed as a credit event. If you are treating 311 bps as a spread problem you are looking at the wrong number.

The mechanism that would normally correct this is unavailable. The Fed cannot cut into 3% inflation with oil at $100. It cannot signal hikes without accelerating the private credit unwind already building. The Fed put that has underwritten credit market risk-taking since 2008 is not suspended. It is logically unavailable given the current configuration of data.

The forward curve is still pricing ~1 cut for the full year. That residual expectation is the last piece of the Fed put not fully removed from market pricing. Watch Wednesday’s press conference. Not for what Powell says. For what he will not commit to. The silence is the signal.

The Primary Market as the Honest Signal

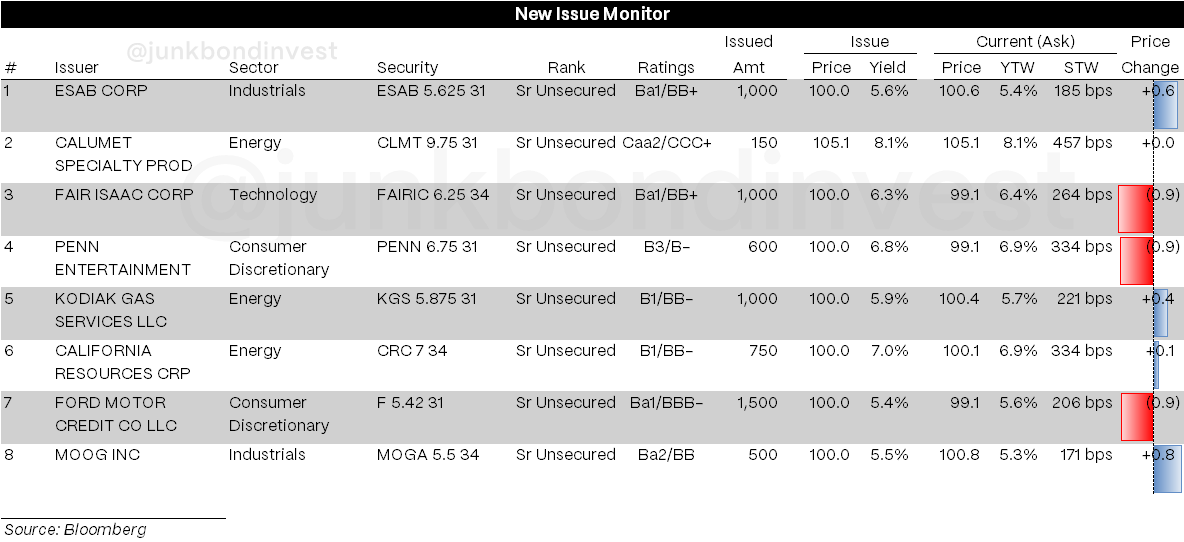

Moog priced $500 million at 5.50%. Defense and aerospace. Traded to 101 immediately. Kodiak Gas Services printed $1 billion at 5.875%. Natural gas infrastructure. Upsized. Clean.

FICO came at the midpoint of guidance and slipped to 99 on the break. Penn priced and immediately backtracked to 99. The deal cleared. The investor concern about profitability did not.

Then there is EA. The largest LBO on record is on deck for the primary market. When it launches it will be the most visible real-time test of investor appetite for large software-adjacent credits in the current environment. The primary marketing task will be convincing investors the company is not actually a software company. That sentence tells you everything about where the sector discount sits right now. Watch how it prices. Watch whether it upsizes or gets cut. The outcome will be more honest than any spread quote published this week.

EA is the exception that proves the rule. The rest of the primary market is not testing anything. It already knows the answer.

All but two deals this week were BB refis. Looks like health. The selection effect is so extreme it has inverted the signal entirely. Each month the primary market stays closed to lower-quality issuers more paper gets pushed into a narrower refinancing window at worse terms. The calm primary market is making the maturity wall problem worse by appearing to solve it.

By the time the compressed maturity wall becomes visible it will already be a negotiating problem rather than a refinancing problem. Those resolve differently. With worse outcomes for existing creditors.

While the leveraged credit primary market quietly closes its doors to lower-quality issuers the investment grade market just had one of the largest issuance weeks in its history. Those two facts are connected.