Credit Weekly: The Reckoning That Isn’t (Yet)

The market survived the week. That’s not the same as being fine.

🚨 Connect: Twitter | Instagram | Reddit | Job Board

Miami was fine.

The panels were polished. The networking was productive. The wifi barely worked. The elevators never came so you took the stairs. You did your 1x1s, worked the evening events, ate your boxed lunch in the overflow room as Jamie Dimon gave his fireside chat. Same as every year.

Except the mood wasn’t.

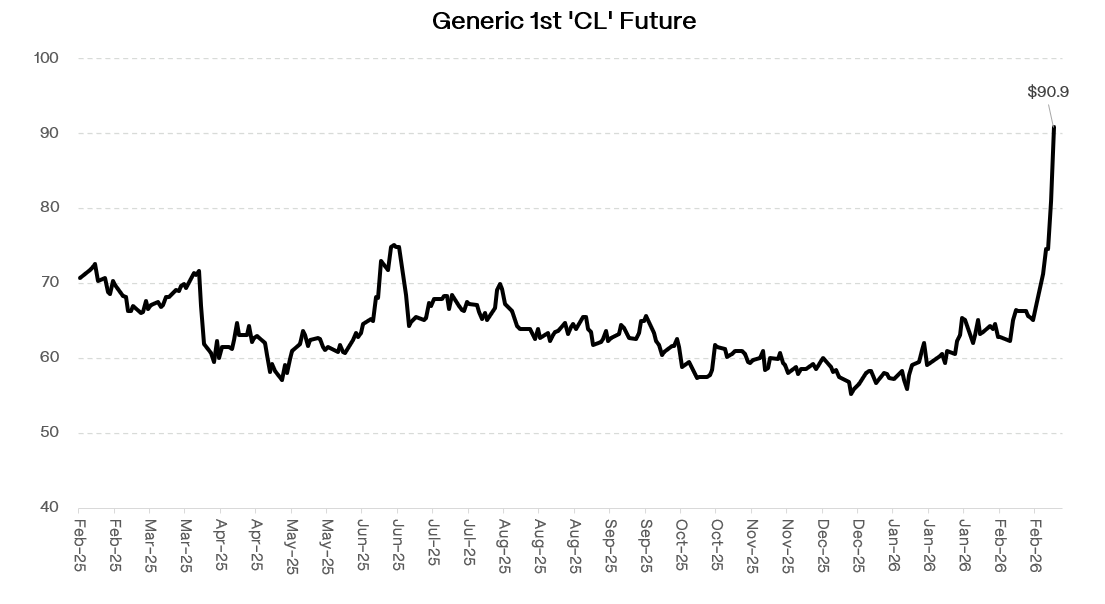

Software disruption dominated every conversation. Analysts cornering management teams about AI risk. The loan market coming off its worst monthly return since 2022. Iran hit over the weekend and suddenly you were managing two crises at once.

You showed up to talk about AI disruption. You left talking about oil and inflation. The dark joke nobody said out loud is that those two narratives run in direct opposition. AI is deflationary. Energy shocks are inflationary. You can’t hold both frameworks simultaneously and come out with a clean trade.

Then you checked your screens.

Oil up 30%. Payrolls -92,000. Private credit redemptions hitting records at multiple major managers while HY spreads stayed flat.

Something in that picture doesn’t add up. Several things, actually.

Here’s what didn’t make the agenda.

The Software Question Everyone Is Asking Wrong

The debate has hardened into two camps and both are missing the point.

Camp One: software credit is uninvestable until the terminal value question gets resolved. The tech loan bid at ~88 cents, AI disruption accelerating, the 2027/2028 maturity wall approaching. Stay away and wait for clarity.

Camp Two: the market is indiscriminately selling. “Mission-critical” platforms with embedded enterprise workflows, high switching costs, and proprietary data are not going to be replaced by a chatbot.

Both camps are right. Both camps are missing something that neither wants to say out loud:

The AI disruption trade is self-fulfilling in a way that changes the math entirely.

Spread widening at the sector level starves software companies of the capital they need to invest in AI. The companies most likely to successfully navigate the transition are precisely the ones that need continued capital access to build the defensive moat: new product development, engineering headcount, customer success investment, etc. By collapsing capital access indiscriminately across the entire sector, the market is selecting against the survivors. It is selecting for the impairment it is trying to price.

The software company that would have refinanced at par six months ago and used the proceeds to build AI-native product features is now facing a 200 bps new issue concession, a lender group demanding covenant resets, and a sponsor increasingly reluctant to inject equity into a narrative-impaired asset. The business that might have adapted is now less likely to adapt. The spread widening made the disruption thesis more true.

This is not a normal credit cycle dynamic. In a normal cycle, spread widening reflects deterioration that has already happened. Here, spread widening is causing deterioration that has not happened yet. The credit market is not observing the outcome. It is partially creating it.

Camp One is right that you cannot underwrite a mediocre software refinancing at par when the terminal value question is unresolved. The A&E math does not give you par. It gives you coupon plus a fee, which is 8-10% on an instrument you are underwriting as a 12-15% YTM. The pull-to-par is not coming.

But the self-fulfilling dynamic eventually creates a clearing event. The companies that survive the capital starvation phase will have demonstrated something the credit market cannot currently price: genuine AI resilience under stress. When the narrative breaks, the recovery in those names will be fast, violent, and concentrated.

The Fed Is Trapped and the Market Hasn’t Priced It

The self-fulfilling dynamic would eventually resolve itself if the macro environment were cooperating. It is not.

Before Iran, the Fed’s path was already narrowing. Core inflation stuck above target, break-evens drifting higher, a labor market that was softening but not breaking.

Then oil moved ~30% in a week and the conversation changed entirely. The forward curve is still pricing meaningful cuts by year-end. Payrolls at -92,000 would normally be the green light. With $90 oil and rising break-evens it is not. Cutting into that environment risks unanchoring expectations in a way that makes the problem structurally worse.

But staying on hold creates a different problem. Every LBO model underwritten assuming significantly lower SOFR by now is running a cash flow shortfall that compounds quarterly. The borrowers who need relief are precisely the ones the Fed cannot help without making the inflation problem worse.

The honest framing: the Fed has one rate for two economies.

Economy One is AI infrastructure, hyperscaler capex, and defense. Completely insensitive to rates. Spending hundreds of billions this year regardless of what Powell does.

Economy Two is everyone in leveraged finance who borrowed at 6-8x leverage assuming rates would normalize. Being slowly impaired by the same rates that are irrelevant to Economy One.

The “Fed put” that has underpinned credit markets since 2008 is functionally suspended. Credit spreads are still pricing it as active. That gap is where the risk is.

CLO Demand: The Invisible Systemic Risk

If the Fed cannot provide relief, the loan market is left depending on a single technical support that most investors are not watching carefully enough.

The leveraged loan market has effectively one marginal buyer right now. Not retail, which has seen billions in outflows YTD with February among the worst months in recent memory. Not hedge funds. CLOs.

Here is the mechanism that matters.

When a CLO fails its OC test because software loan prices have fallen, the instinct is to sell the problem assets. But most CLO structures calculate overcollateralization on par value, not market value. Selling a software loan at 87 cents takes a par hit that makes the OC test worse, not better. So managers do the opposite. They sell their best performing positions at or above par instead. The chemicals credit at par. The energy name above par. The industrial issuer that just reported strong earnings. The OC test gets fixed. The CLO looks clean on paper. A fundamentally sound credit in an unrelated sector is wider for no fundamental reason.

This happened in 2015-16. CLO managers sold their best non-energy assets to rebalance structures stressed by oil patch deterioration. Credits with nothing wrong widened for months. Almost nobody recognized the mechanism in real time. The investors who did cleaned up on the other side.

Software is 2016 energy. The collateral damage will show up in sectors where your credit work says nothing is wrong. That is not a reason to avoid those sectors. It is a reason to have the buy list ready when the widening arrives.

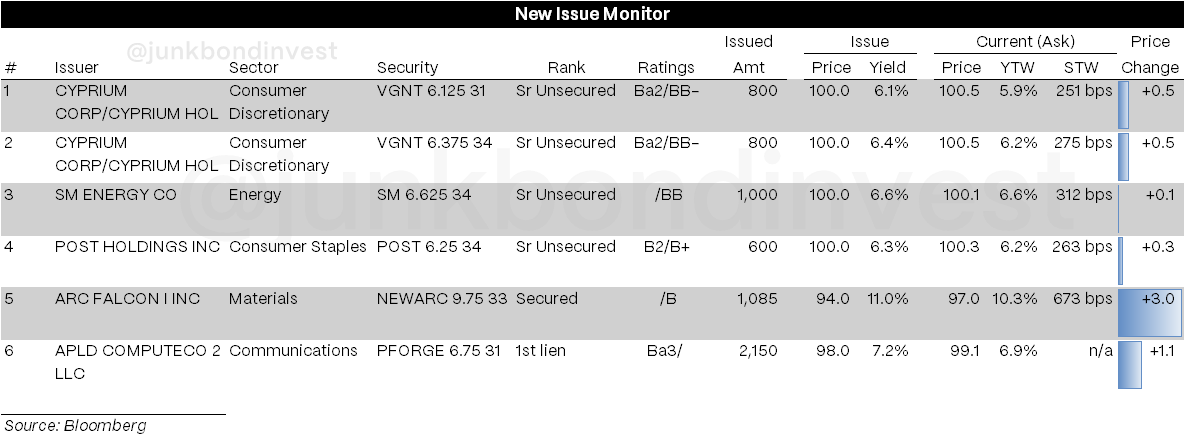

The deeper problem: the supply/demand gap in loans is being bridged almost entirely by CLO formation. Multiple tech deals have been pulled from primary since late January. As CLO managers become more selective about eligible collateral, the feedback loop from tighter CLO standards to wider primary pricing to more pulled deals becomes self-reinforcing. It does not require a crisis. It just requires the marginal CLO deal to stop making economic sense.

Primary Market as Live Confirmation

You do not need to model any of this. The primary market is showing you in real time.

Two markets are running on the same screen right now. Energy and infrastructure printing clean, upsizing, trading up. Software-adjacent situations shelved, delayed, or restructured before launch. The line between them is not rating or sector in the broad sense. It is whether your business model has a question mark attached to it that a credit investor cannot underwrite through to a confident answer at current prices.

The EA financing makes the point cleanly. The debt package for the largest LBO on record is shifting heavily toward bonds and away from loans. When banks underwriting a marquee buyout make that call, they are not making an academic observation. They are telling you directly that loan investor appetite for large software-adjacent credits is impaired at scale. Deal structure is more honest than spread quotes.

The fact that the EA pitch had to be made at all tells you where the market’s head is. Bankers have been spending their time assuring anchor investors that EA is not a software company in the disruptable sense. The IP in Madden NFL and The Sims is defensible. Which is a sentence that has never been uttered in a leveraged finance context before and yet here we are.

The pitch is reasonable and probably correct for EA specifically. But if you are running a $55B buyout and your primary marketing task is convincing investors your software company is not actually a software company, the sector discount is real and it is structural.

Private Credit: The Ratchet

The public market signals are clear. What makes this cycle harder to manage is that the stress is building simultaneously in a market where the signals are deliberately obscured.

This is not a liquidity problem. It is a trust problem. And trust problems do not respond to liquidity solutions.

When Blackstone injects firm and employee capital to avoid formally changing its tender offer terms, that is reputation management. Retail investors are not pulling money because they need liquidity. They are pulling because they do not believe the marks. Publicly traded BDC peers pricing at significant discounts to NAV suggests the institutional market agrees.

Here is what makes this structurally different from a normal credit cycle. Redemption pressure forces asset sales. Managers sell their best assets first because those are liquid and at par. The assets remaining are more concentrated in marks-at-model positions that have not been independently validated. The average NAV stays roughly stable. The actual quality of the collateral behind the NAV quietly deteriorates.

Each redemption cycle that forces par sales of the best credits leaves a portfolio incrementally more concentrated in the assets nobody wanted to buy. The ratchet does not require a crisis to operate. It just requires inflows to stay below outflows for a few more quarters.

What is actually inside those remaining portfolios is the part of this story that is not being told clearly enough. The 2020-2022 vintage MM PE playbook was built on one core assumption: labor costs are stable and manageable.